Advertisement

- United States

- /

- IT

- /

- NasdaqGM:III

Information Services Group, Inc. Just Beat Analyst Forecasts, And Analysts Have Been Updating Their Predictions

Information Services Group, Inc. (NASDAQ:III) just released its third-quarter report and things are looking bullish. It was a solid earnings report, with revenues and statutory earnings per share (EPS) both coming in strong. Revenues were 16% higher than the analysts had forecast, at US$62m, while EPS were US$0.04 beating analyst models by 433%. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

Check out our latest analysis for Information Services Group

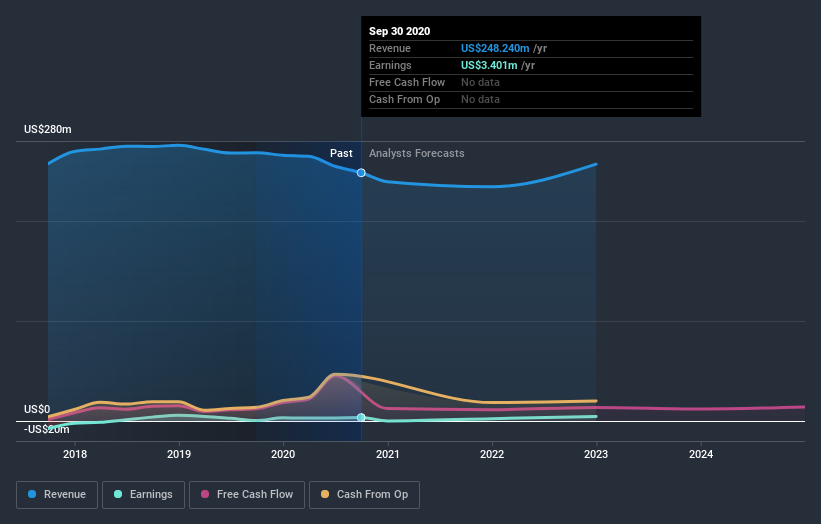

Following the recent earnings report, the consensus from four analysts covering Information Services Group is for revenues of US$234.2m in 2021, implying a small 5.7% decline in sales compared to the last 12 months. Statutory earnings per share are forecast to crater 44% to US$0.04 in the same period. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$236.8m and earnings per share (EPS) of US$0.043 in 2021. The analysts seem to have become a little more negative on the business after the latest results, given the minor downgrade to their earnings per share numbers for next year.

The average price target fell 24% to US$4.25, with reduced earnings forecasts clearly tied to a lower valuation estimate. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. There are some variant perceptions on Information Services Group, with the most bullish analyst valuing it at US$5.00 and the most bearish at US$3.50 per share. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Information Services Group's past performance and to peers in the same industry. We would highlight that sales are expected to reverse, with the forecast 5.7% revenue decline a notable change from historical growth of 5.2% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 13% next year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Information Services Group is expected to lag the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Fortunately, the analysts also reconfirmed their revenue estimates, suggesting sales are tracking in line with expectations - although our data does suggest that Information Services Group's revenues are expected to perform worse than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Information Services Group's future valuation.

With that in mind, we wouldn't be too quick to come to a conclusion on Information Services Group. Long-term earnings power is much more important than next year's profits. We have forecasts for Information Services Group going out to 2022, and you can see them free on our platform here.

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Information Services Group , and understanding this should be part of your investment process.

If you decide to trade Information Services Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NasdaqGM:III

Information Services Group

Operates as an artificial intelligence (AI) centered technology research and advisory company in the Americas, Europe, and the Asia Pacific.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor