Advertisement

- United States

- /

- Software

- /

- NasdaqGS:IDCC

InterDigital's (NASDAQ:IDCC) Shareholders Will Receive A Bigger Dividend Than Last Year

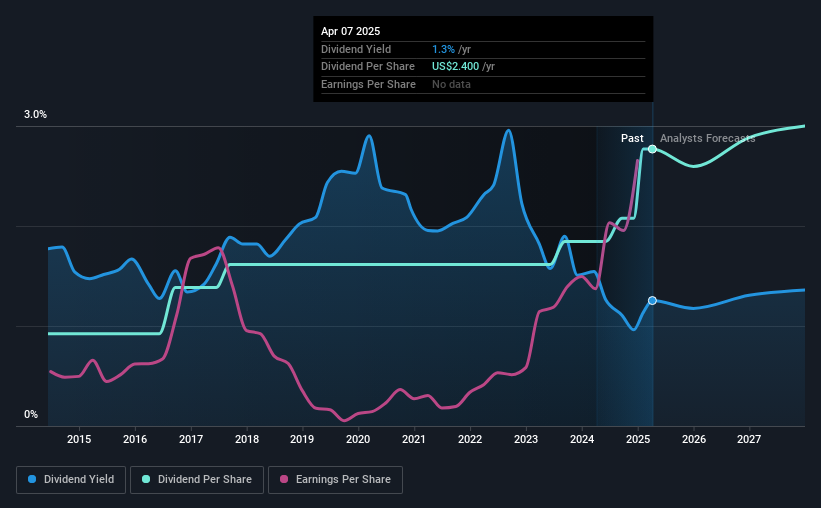

The board of InterDigital, Inc. (NASDAQ:IDCC) has announced that it will be paying its dividend of $0.60 on the 23rd of April, an increased payment from last year's comparable dividend. This makes the dividend yield 1.3%, which is above the industry average.

InterDigital's Projected Earnings Seem Likely To Cover Future Distributions

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. However, prior to this announcement, InterDigital's dividend was comfortably covered by both cash flow and earnings. This means that most of its earnings are being retained to grow the business.

Over the next year, EPS is forecast to fall by 44.0%. If the dividend continues along recent trends, we estimate the payout ratio could be 26%, which we consider to be quite comfortable, with most of the company's earnings left over to grow the business in the future.

See our latest analysis for InterDigital

InterDigital Has A Solid Track Record

The company has an extended history of paying stable dividends. The annual payment during the last 10 years was $0.80 in 2015, and the most recent fiscal year payment was $2.40. This implies that the company grew its distributions at a yearly rate of about 12% over that duration. Rapidly growing dividends for a long time is a very valuable feature for an income stock.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. It's encouraging to see that InterDigital has been growing its earnings per share at 84% a year over the past five years. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

We Really Like InterDigital's Dividend

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. The earnings easily cover the company's distributions, and the company is generating plenty of cash. If earnings do fall over the next 12 months, the dividend could be buffeted a little bit, but we don't think it should cause too much of a problem in the long term. All of these factors considered, we think this has solid potential as a dividend stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Taking the debate a bit further, we've identified 2 warning signs for InterDigital that investors need to be conscious of moving forward. Is InterDigital not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:IDCC

InterDigital

Operates as a global research and development company focuses on wireless, visual, artificial intelligence (AI), and related technologies.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0776.3% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

JA

Jades on Coca-Cola ·

Coca-Cola’s Enduring Moat in a Health-Conscious World: Steady Compounder Poised for 5-10% Annual Returns Through Emerging Market Dominance

Fair Value:US$66.221.6% overvalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

ET

Ethan_cpa on Xero ·

Xero: Growth Was Priced In — Execution Is Not

Fair Value:AU$101.5619.0% undervalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.374.1% undervalued

34 followersusers have followed this narrative

3 commentsusers have commented on this narrative

22 likesusers have liked this narrative

Recently Updated Narratives

UN

unknown on Salesforce ·

Salesforce (CRM) The Agentic Pivot: Salesforce Redefines the SaaS Era

Fair Value:US$25424.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

UN

unknown on NVIDIA ·

Nvidia (NVDA) The Sovereign of Silicon: Accelerating Beyond the $5 Trillion Horizon

Fair Value:US$248.421.3% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JA

Janpeo on Stellantis ·

IA Analysis

Fair Value:€1140.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.887.4% undervalued

65 followersusers have followed this narrative

5 commentsusers have commented on this narrative

28 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59632.8% undervalued

1297 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

TA

Talos on Tesla ·

The "Physical AI" Monopoly – A New Industrial Revolution

Fair Value:US$665.3637.3% undervalued

49 followersusers have followed this narrative

20 commentsusers have commented on this narrative

22 likesusers have liked this narrative