Advertisement

- United States

- /

- IT

- /

- NasdaqGS:FSLY

Fastly (FSLY): Exploring the Valuation Gap After Recent Share Price Weakness

Fastly (FSLY) has quietly drifted lower over the past month, even though its longer term performance looks better. That gap between sentiment and fundamentals is what makes the stock interesting now.

See our latest analysis for Fastly.

Over the last year, Fastly’s share price has swung between renewed optimism and caution. The recent 30 day share price return of negative 9.44 percent has cooled what had been stronger 90 day momentum, while the three year total shareholder return of 20.93 percent shows that patient holders have still come out ahead despite a weaker one year total shareholder return of negative 10.24 percent.

If you like Fastly’s volatility but want more names on your radar, this is a good moment to explore high growth tech and AI stocks for other potential growth stories.

With shares still far below their five year peak, but only modestly below analyst targets, the key question now is whether Fastly is quietly undervalued or if the market is already pricing in its next leg of growth.

Most Popular Narrative: 2.4% Undervalued

Fastly's most followed narrative puts fair value slightly above the last close of $10.17, framing the stock as modestly mispriced rather than deeply discounted.

The acceleration of cloud migration and edge computing, combined with Fastly's increased product velocity (especially in Compute and adaptive observability analytics at the edge), expands the company's addressable market and supports durable multi-year revenue growth.

Want to see how measured revenue growth, improving margins, and a rich future earnings multiple all connect into that small discount? The full narrative explains the specific forecasts, the timing of margin inflection, and the valuation math behind this fair value estimate.

Result: Fair Value of $10.42 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sustained CDN pricing pressure and reliance on a concentrated group of large customers could quickly challenge assumptions about margin expansion and steady growth.

Find out about the key risks to this Fastly narrative.

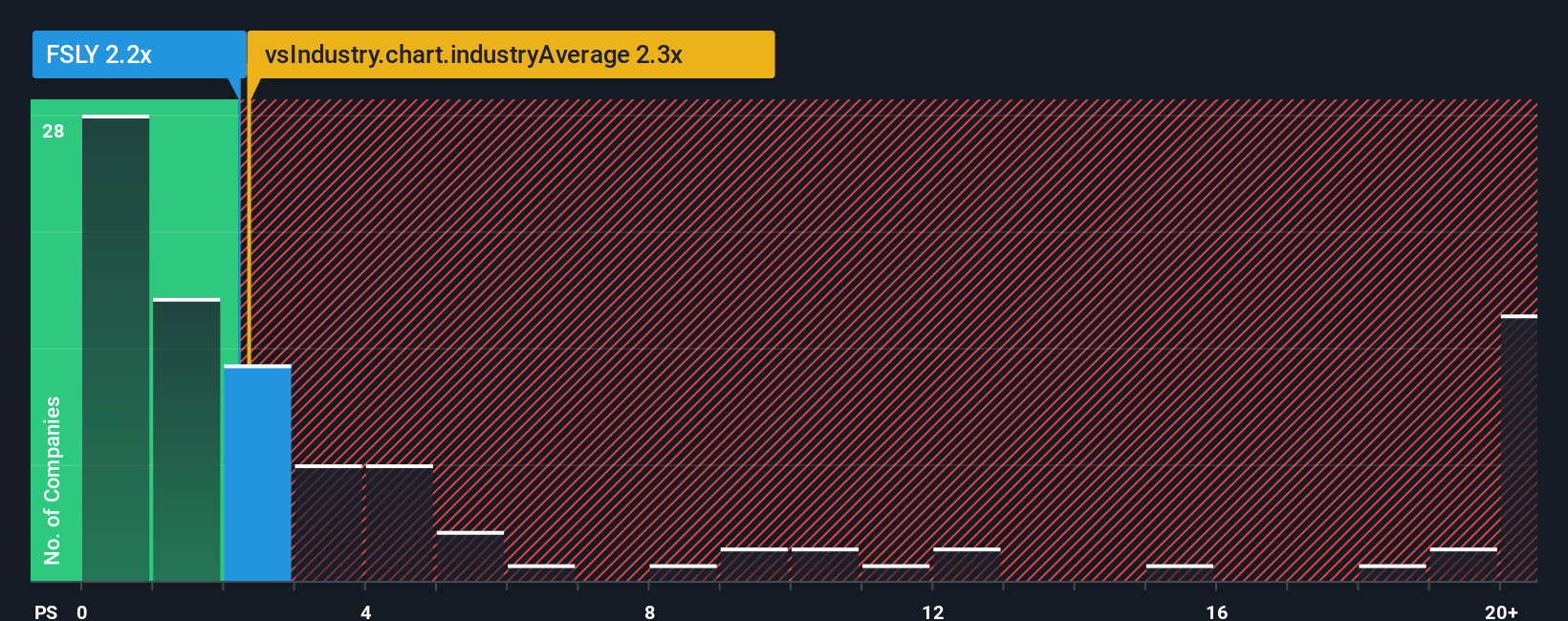

Another View: Market Ratio Signals Caution

While the narrative suggests Fastly is about 2.4 percent undervalued, its price to sales ratio near 2.6 times tells a different story. That is slightly more expensive than the US IT average of 2.5 times, and only in line with its own fair ratio of 2.6 times. This hints at a limited margin of safety if growth disappoints.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Fastly Narrative

If you see the story differently or simply want to dig into the numbers yourself, you can build a personalized view in minutes using Do it your way.

A great starting point for your Fastly research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Ready for your next investing move?

Fastly might fit your thesis today, but you will miss some of the market’s strongest setups if you ignore the opportunities waiting in our screeners.

- Capture potential mispricings by targeting quality companies trading below their estimated worth with these 909 undervalued stocks based on cash flows that highlight compelling value ideas.

- Ride powerful innovation trends by focusing on these 25 AI penny stocks that could benefit most as artificial intelligence adoption accelerates globally.

- Strengthen your income stream by hunting for reliable payers through these 13 dividend stocks with yields > 3% that offer yields above 3 percent with supporting fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:FSLY

Fastly

Operates an edge cloud platform for processing, serving, and securing its customer’s applications in the United States, the Asia Pacific, Europe, and internationally.

Excellent balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0776.3% undervalued

88 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9820.4% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1558.0% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3648.3% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on DIGITAL HEARTS HOLDINGS ·

Strategic pivot in maximizing corporate value

Fair Value:JP¥928.162.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FI

Finder109 on BARK ·

Buy-out proposal for BARK Inc., at $1.10 has be confirmed by the acquisition group

Fair Value:US$1.443.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DH

Dhruva on Paladin Energy ·

Paladin Energy: Betting on the Nuclear Renaissance

Fair Value:AU$1.87563.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.376.9% undervalued

51 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59631.9% undervalued

1306 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.0% undervalued

1103 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative