Advertisement

- United States

- /

- IT

- /

- NasdaqGS:DOX

These 4 Measures Indicate That Amdocs (NASDAQ:DOX) Is Using Debt Safely

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Amdocs Limited (NASDAQ:DOX) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Amdocs

What Is Amdocs's Net Debt?

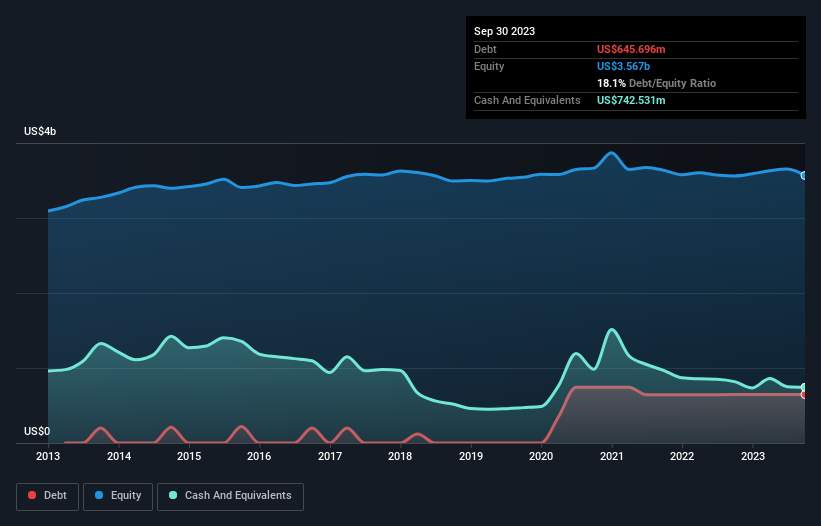

As you can see below, Amdocs had US$645.7m of debt, at September 2023, which is about the same as the year before. You can click the chart for greater detail. However, it does have US$742.5m in cash offsetting this, leading to net cash of US$96.8m.

How Healthy Is Amdocs' Balance Sheet?

We can see from the most recent balance sheet that Amdocs had liabilities of US$1.35b falling due within a year, and liabilities of US$1.51b due beyond that. Offsetting this, it had US$742.5m in cash and US$944.5m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$1.17b.

Of course, Amdocs has a market capitalization of US$9.97b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. While it does have liabilities worth noting, Amdocs also has more cash than debt, so we're pretty confident it can manage its debt safely.

The good news is that Amdocs has increased its EBIT by 8.6% over twelve months, which should ease any concerns about debt repayment. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Amdocs can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. Amdocs may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Amdocs recorded free cash flow worth a fulsome 98% of its EBIT, which is stronger than we'd usually expect. That puts it in a very strong position to pay down debt.

Summing Up

Although Amdocs's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$96.8m. And it impressed us with free cash flow of US$698m, being 98% of its EBIT. So is Amdocs's debt a risk? It doesn't seem so to us. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Amdocs's earnings per share history for free.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:DOX

Amdocs

Through its subsidiaries, provides software and services to communications, entertainment, media, and other service providers worldwide.

6 star dividend payer and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1158.7% undervalued

32 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.6% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9220.2% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$1908.3% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

JO

John_Eric on ServiceNow ·

The Company Nobody Brags About

Fair Value:US$266.0164.1% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnimalDoctorKwon on DuChemBIOLtd ·

DuChemBio absorbs Radio DNS Labs as Novartis injects 140B KRW into Korean RLT. With 100%+ OCF/EBITDA, the 6-mo lag is a de-risked steal.

Fair Value:₩10k43.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

Alice3D on ServiceNow ·

NOW is an established SAAS positioned for accelerated growth over the next 5 years.

Fair Value:US$15538.4% undervalued

23 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.1% undervalued

101 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5449.5% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual income — with every assumption published and tagged as fact or assumption. The interesting result isn't a number, it's a disagreement: the point estimates run from €20,03 (RIM) through €27,64 (DDM) to €64,91 (DCF), and the pairwise overlaps form two disjoint segments — €20,36–€21,54 and €39,60–€44,56. Between €21,54 and €39,60, no two of the three models agree. [img]https://staticm.fastcomments.com/1784197249786-1000x1000-ad-range-strip.png[/img] Most of the spread is lens properties rather than company drama. A dividend model structurally can't see the roughly half of shareholder returns Ahold pays through buybacks. The book is ~96 % goodwill from the 2016 merger, which pins the residual-income reading low. And ~83 % of the DCF's value sits beyond the explicit five years, so it leans hard on the terminal assumptions. Three honest lenses, three honest answers — the disagreement is the information. Disclosures Position disclosure: The author holds no position in Ahold Delhaize as at 9 July 2026. This valuation is a StoxEurope opinion, based on honest research. Mistakes are possible. This is not investment advice. Do your own research. This article demonstrates a valuation methodology. It is not an investment recommendation, is not personalised to any reader's circumstances, and every figure in it depends entirely on the stated assumptions

1

|0

ST

stephen_iwu3c on CK Hutchison Holdings ·

Hutchsion 3 UK has been sold to vodafone, why is there an integration costs, is the analysis outdated?

0

|0