Advertisement

- United States

- /

- IT

- /

- NasdaqGS:DOX

Is Amdocs Trading Below Fair Value After New Telecom Partnerships?

Reviewed by Bailey Pemberton

- Curious if Amdocs is really delivering value for your investment dollar? You are not alone. With the stock in the spotlight, now is the perfect time to take a deeper look.

- After trading at $84.57, Amdocs has seen a return of 4.7% over the past month, but is still trailing by -6.0% over the past year.

- Recently, Amdocs caught attention after it was included in major technology benchmarks and expanded its partnership with several telecom giants. These moves signal both growth ambitions and shifting market sentiment. Headlines have highlighted Amdocs' new contracts with top mobile operators, which may be fueling renewed interest among investors.

- The company's valuation score currently stands at 6/6, meaning it appears undervalued on every metric we check. Next, we will break down what those metrics mean. At the end of the article, we will introduce an approach that could help you see valuation from a completely new perspective.

Find out why Amdocs's -6.0% return over the last year is lagging behind its peers.

Approach 1: Amdocs Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's value by projecting its future cash flows and discounting them to today's dollars. For Amdocs, this involves examining expected free cash flows over the coming years and calculating how much those are worth now, based on typical return rates and risk factors.

Currently, Amdocs generates $613 million in Free Cash Flow (FCF). Analyst estimates put annual FCF at $728 million in 2026 and $808 million in 2027, with projections indicating steady growth through 2030, reaching $973 million according to extended forecasts. The first five years are based on analyst estimates, while cash flows beyond that are extrapolated by Simply Wall St’s model.

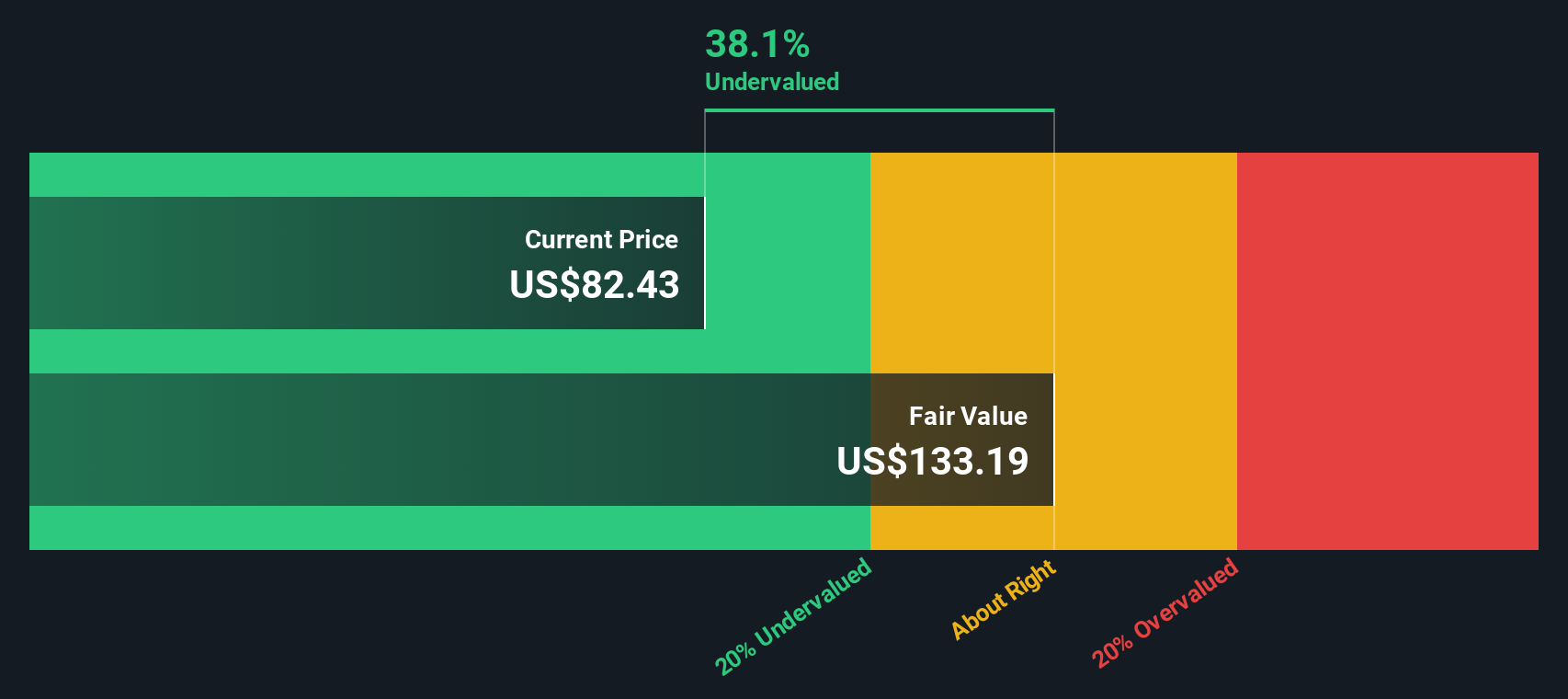

After calculating and discounting these future cash flows, the DCF valuation comes out to $133.25 per share. With shares last trading at $84.57, this suggests the stock is undervalued by 36.5 percent compared to its modeled intrinsic value.

A substantial discount between the share price and the calculated value signals a potential opportunity for investors and suggests that Amdocs is trading below what its future cash generation would justify.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Amdocs is undervalued by 36.5%. Track this in your watchlist or portfolio, or discover 875 more undervalued stocks based on cash flows.

Approach 2: Amdocs Price vs Earnings

The Price-to-Earnings (PE) ratio is a well-known valuation metric, especially useful for profitable companies like Amdocs. It compares the company’s market value to its net earnings and helps investors assess how much they are paying per dollar of profit. Since Amdocs consistently generates healthy earnings, PE is a suitable benchmark for gauging value.

What constitutes a “normal” or “fair” PE ratio depends on the company’s growth expectations and risk profile. Companies with strong anticipated growth and lower risk generally command higher PE ratios. Those with slower growth or more uncertainty tend to trade at lower valuations.

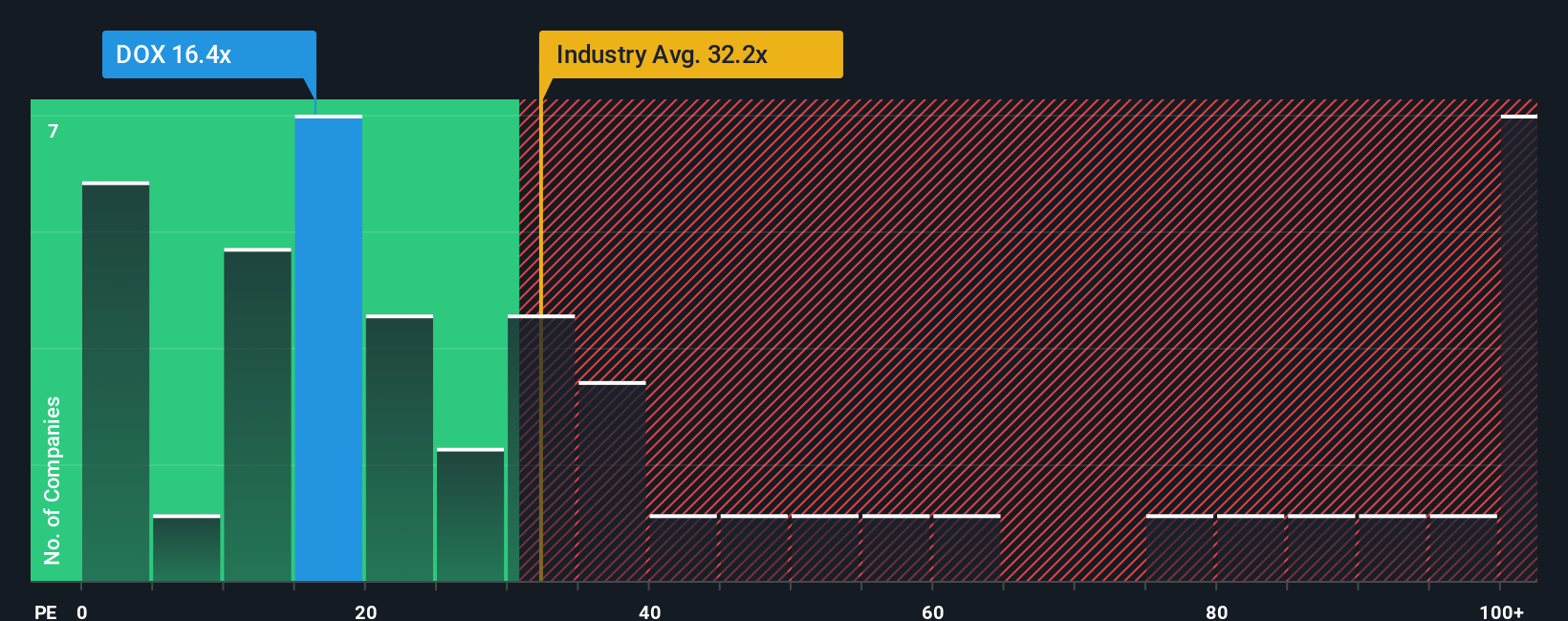

Amdocs currently trades at a PE ratio of 16.8x. This is noticeably below both the industry average for IT companies at 31.1x and the peer group benchmark at 19.0x. On its face, this might suggest a discount compared to peers and the broader sector.

However, Simply Wall St’s proprietary “Fair Ratio” provides more nuance. The Fair Ratio for Amdocs stands at 32.9x and incorporates specific factors like expected earnings growth, profitability, market cap, and risk profile. Unlike traditional peer or industry comparisons, the Fair Ratio adapts to the company’s unique circumstances, providing a multidimensional benchmark rather than a simple average.

Since the Fair Ratio of 32.9x is significantly above Amdocs’ actual PE of 16.8x, this analysis suggests the stock is undervalued based on its earnings potential and adjusted risk factors.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1404 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Amdocs Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is a simple and approachable tool that allows you to create a story, your personal perspective, that connects the numbers behind Amdocs (such as fair value, projected revenue, earnings, and margins) with the bigger picture of the business.

With Narratives, you can link your investment thesis and expectations for Amdocs’ future to a financial forecast, which then calculates your own fair value. This makes it easy to see how your view lines up with market prices. Narratives are available right now to millions of investors within the Simply Wall St Community page, offering an accessible way to move beyond just numbers and see the “why” behind your valuation.

By tracking the difference between your estimated fair value and the current share price, Narratives help you make more confident decisions about when to buy or sell. They are dynamically updated as new information comes in, for instance, after earnings releases or breaking news, so your view is always current.

As an example, one investor might believe that Amdocs’ rapid expansion into cloud and AI will justify a fair value as high as $133 per share, while another sees risks from client concentration and slower SaaS traction, arriving at a value closer to $85. Narratives make both perspectives simple to quantify and track.

Do you think there's more to the story for Amdocs? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DOX

Amdocs

Through its subsidiaries, provides software and services to communications, entertainment, media, and other service providers worldwide.

6 star dividend payer and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2535.8% undervalued

146 followersusers have followed this narrative

0 commentsusers have commented on this narrative

26 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0332.6% undervalued

31 followersusers have followed this narrative

3 commentsusers have commented on this narrative

10 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.521.1% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.726.3% undervalued

41 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Recently Updated Narratives

HU

Hunter_Z on Oriental Kopi Holdings Berhad ·

Oriental Kopi's Indonesia JV Strengthens Regional Growth Narrative

Fair Value:RM 1.533.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ST

StoxEurope on UCB ·

FV 206,24 but with a 310-154 range...to discuss

Fair Value:€206.249.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Figma ·

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value:US$22.3625.9% overvalued

62 followersusers have followed this narrative

7 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28021.7% undervalued

260 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9116.1% overvalued

128 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$202.6278.9% overvalued

139 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0

FU

FundamentalFlow on Green Tea Group ·

Great narrative! Many people focus on AI nowadays (including me), and it's refreshing to see a deep dive into the fundamentals of a business like Green Tea. I really appreciate how you cut through the market noise to focus on the unit economics and the structural risks.I also write from a fundamentals-first perspective, and I'm currently working on an analysis of Samsung Electronics. I've been trying to refine how I balance factors such as financial health, future, and valuation of a company.If you have a moment, I'd love for you to take a look at my narritives. I'd value your perspective on whether my analysis holds up to the level of rigor you set here. No pressure at all, but I'd appreciate the feedback if you're open to it!

1

|0