Advertisement

- United States

- /

- IT

- /

- NasdaqGS:DOX

Is Amdocs (NASDAQ:DOX) A Risky Investment?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Amdocs Limited (NASDAQ:DOX) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Amdocs

What Is Amdocs's Debt?

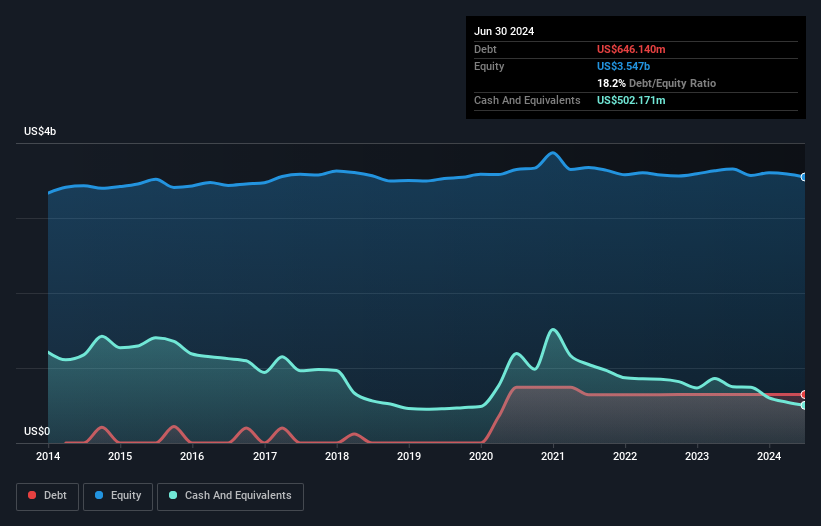

The chart below, which you can click on for greater detail, shows that Amdocs had US$646.1m in debt in June 2024; about the same as the year before. However, it does have US$502.2m in cash offsetting this, leading to net debt of about US$144.0m.

How Healthy Is Amdocs' Balance Sheet?

The latest balance sheet data shows that Amdocs had liabilities of US$1.42b due within a year, and liabilities of US$1.43b falling due after that. Offsetting this, it had US$502.2m in cash and US$1.02b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$1.33b.

Of course, Amdocs has a titanic market capitalization of US$10.1b, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. Carrying virtually no net debt, Amdocs has a very light debt load indeed.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Amdocs's net debt is only 0.15 times its EBITDA. And its EBIT covers its interest expense a whopping 20.3 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Fortunately, Amdocs grew its EBIT by 5.3% in the last year, making that debt load look even more manageable. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Amdocs's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. During the last three years, Amdocs generated free cash flow amounting to a very robust 85% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Our View

Amdocs's interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. And that's just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. Looking at the bigger picture, we think Amdocs's use of debt seems quite reasonable and we're not concerned about it. While debt does bring risk, when used wisely it can also bring a higher return on equity. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Amdocs's earnings per share history for free.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:DOX

Amdocs

Through its subsidiaries, provides software and services to communications, entertainment, media, and other service providers worldwide.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4351.3% undervalued

77 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

28 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8166.9% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

DE

DeathSmiIes on New Horizon Aircraft ·

HORIZON AIRCRAFT (HOVR)

Fair Value:US$2084.3% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

berkdnd on Yeo Teknoloji Enerji Ve Endustri Anonim Sirketi ·

Yeo Teknoloji Enerji için hedef fiyat analizi

Fair Value:₺152.726.4% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JA

Janpeo on Stellantis ·

IA Analysis

Fair Value:€1140.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.4% undervalued

113 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6119.8% undervalued

1194 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

28 likesusers have liked this narrative