Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DOCU

Is It Time To Reconsider DocuSign (DOCU) After Recent Share Price Weakness?

Reviewed by Bailey Pemberton

- Wondering if DocuSign at around US$42.89 is priced for a comeback or still carrying too much optimism? This article walks through what the numbers actually say about its value.

- The stock has been under pressure, with returns of 11.3% over 7 days, 7.7% over 30 days, 33.9% year to date and 42.3% over 1 year. This naturally raises questions about whether the risk and reward now look different to you than they did in the past.

- Recent share price moves are occurring alongside ongoing attention on DocuSign's role in digital agreement workflows and how that fits into broader software spending. Investors are weighing where contract management and e-signature tools sit in their own priorities. News coverage has also focused on how companies are using digital agreement platforms to improve efficiency, which can influence sentiment around DocuSign even without company specific announcements.

- DocuSign currently holds a value score of 4 out of 6. The rest of this article will walk through what different valuation approaches suggest about that score, while hinting at a richer way to judge value that comes together at the end.

Find out why DocuSign's -42.3% return over the last year is lagging behind its peers.

Approach 1: DocuSign Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes projected future cash flows and then discounts them back to today using a required rate of return, to estimate what the business might be worth now.

For DocuSign, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections rather than earnings. The latest twelve month Free Cash Flow is about $1.06b. Analyst style projections and extensions put Free Cash Flow at $989.93m in 2026, $1,118.46m in 2027 and $1,367m by 2029, with further years extrapolated by Simply Wall St rather than based on direct analyst estimates.

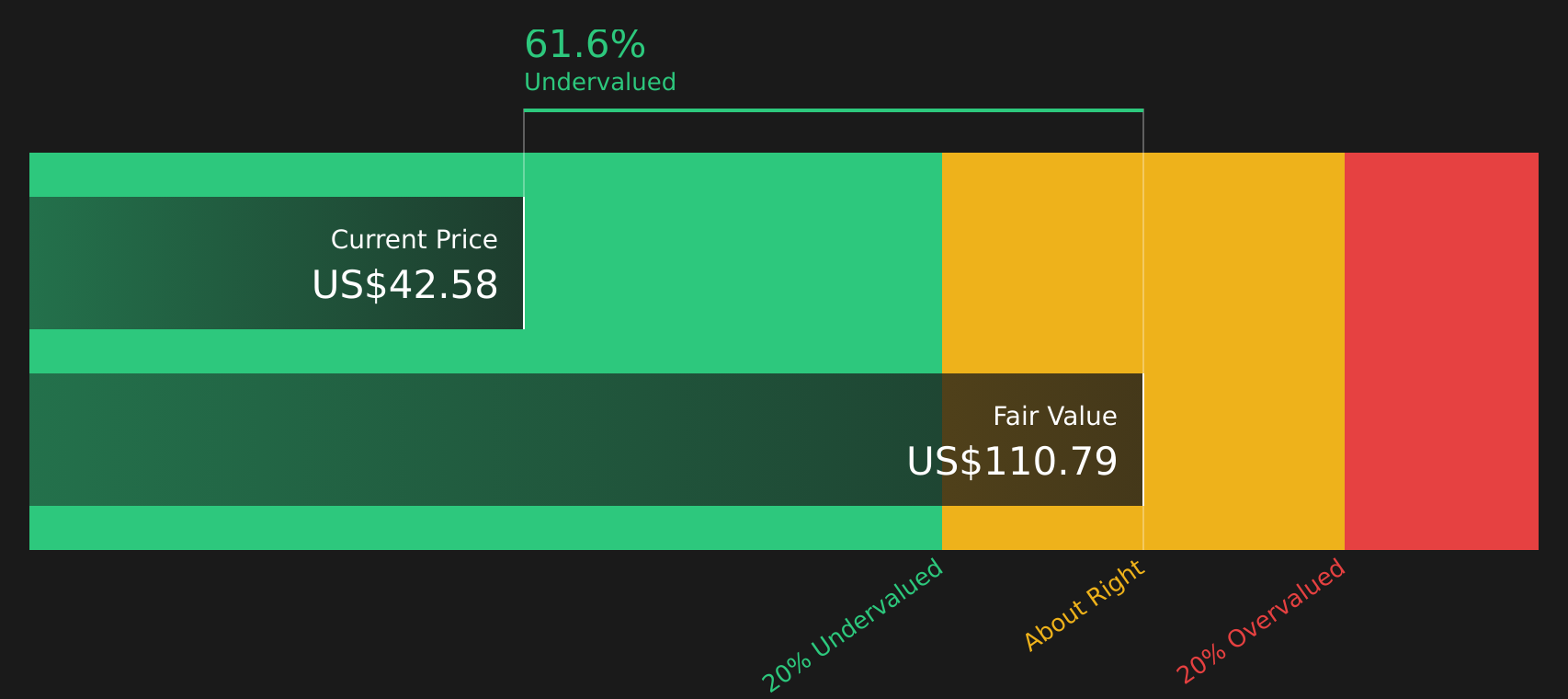

When these projected cash flows are discounted back to today and combined with a terminal value, the model arrives at an estimated intrinsic value of about $134.42 per share. Compared with a current share price around $42.89, this DCF output suggests the stock is 68.1% undervalued on these assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests DocuSign is undervalued by 68.1%. Track this in your watchlist or portfolio, or discover 58 more high quality undervalued stocks.

Approach 2: DocuSign Price vs Earnings

The P/E ratio is a common way to value profitable companies because it links what you pay for each share to the earnings that company is currently generating. It gives you a quick sense of how many dollars investors are paying for each dollar of earnings.

What counts as a “normal” P/E depends a lot on how fast earnings are expected to change and how risky those earnings look. Higher growth expectations and lower perceived risk often go with higher P/E ratios, while slower growth or higher risk tend to go with lower P/E ratios.

DocuSign currently trades on a P/E of 26.98x. That sits slightly above the Software industry average of about 26.88x and below the peer group average of 29.74x. Simply Wall St also provides a “Fair Ratio” of 28.83x, which is the P/E it would expect for DocuSign given factors such as its earnings profile, industry, profit margin, market cap and risk characteristics.

This Fair Ratio can be more tailored than a simple comparison with peers or the broad industry, because it brings those company specific factors together in one number. With DocuSign at 26.98x versus a Fair Ratio of 28.83x, the P/E based view points to the shares being undervalued on these inputs.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 18 top founder-led companies.

Upgrade Your Decision Making: Choose your DocuSign Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so this is where Narratives come in. They give you a simple story behind the numbers by tying your view on DocuSign's future revenue, earnings and margins to a financial forecast, a Fair Value, and then a clear comparison with the current share price. All of this is available within an easy to use tool on Simply Wall St's Community page that updates as new news or earnings arrive and that can reflect very different perspectives. For example, one investor may lean toward a higher Fair Value near US$94.10 based on stronger AI monetisation and margin discipline, while another may lean toward a lower Fair Value around US$53 based on more cautious assumptions about growth, competition and future P/E multiples.

Do you think there's more to the story for DocuSign? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DOCU

DocuSign

Provides electronic signature solution in the United States and internationally.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7061.6% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17036.6% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38026.3% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.8% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

Recently Updated Narratives

IM

Imthetxarbi on Betsson ·

The Market Is Paying You a 9.3% Dividend and an 18.9% FCF Yield to Wait for a Recovery That's Already Starting

Fair Value:SEK 16747.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IM

Imthetxarbi on Evolution ·

A Monopoly-Quality Business Trading at Distress Multiples — CEO Buying, €346M Buyback Active, 73% Upside to Fair Value

Fair Value:SEK 1.04k33.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IM

Imthetxarbi on SThree ·

Every Staffing Stock Is Being Sold. SThree Is the Only One That Benefits From the Thing Killing the Others

Fair Value:UK£4.966.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.7% undervalued

124 followersusers have followed this narrative

3 commentsusers have commented on this narrative

36 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9722.1% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1930.3% undervalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative