Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DOCU

Is DocuSign (DOCU) Pricing Looked At Differently After Its Recent Share Price Rebound?

Reviewed by Bailey Pemberton

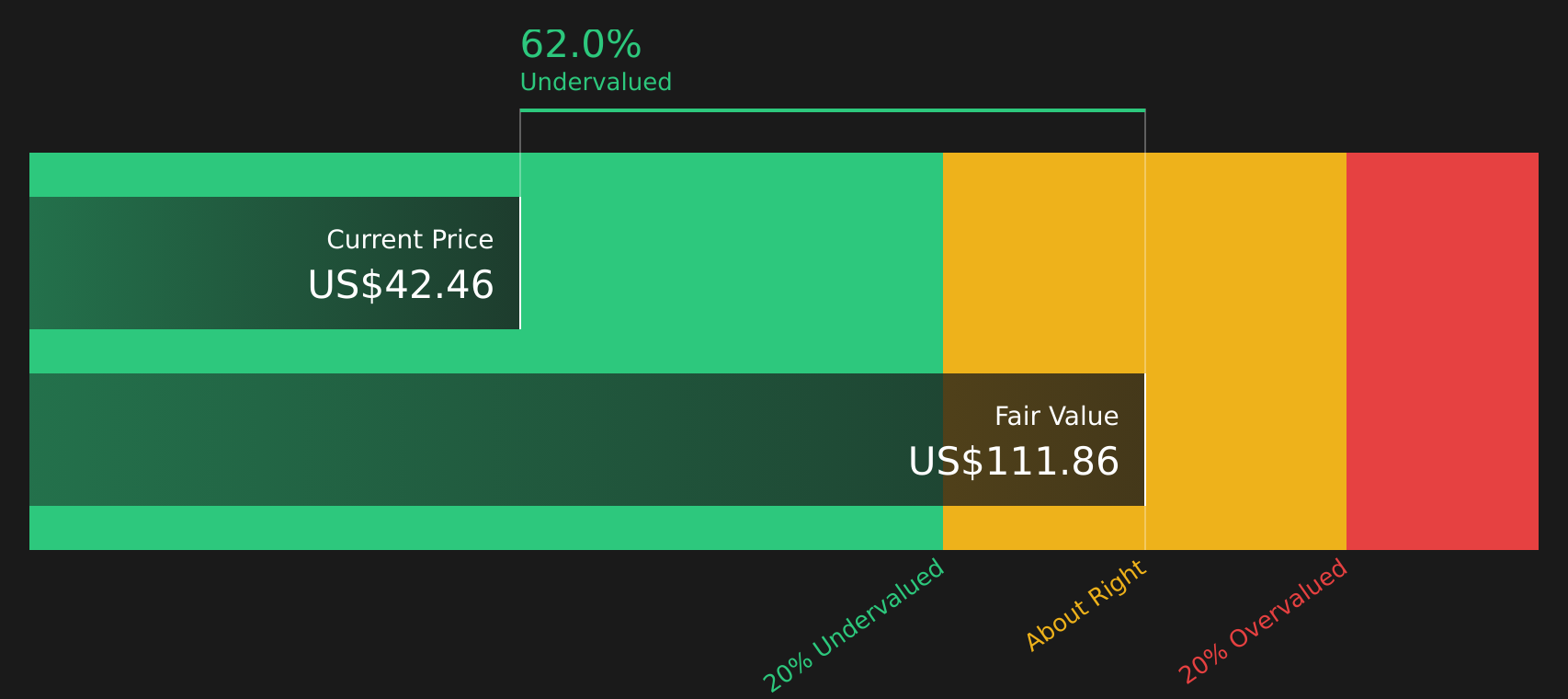

- If you are wondering whether DocuSign is a bargain or a value trap at around US$48.23, you are not alone. Many investors are trying to work out what a fair price looks like today.

- Over the past week the share price is up 5.5% and it is 4.7% higher over the last 30 days. Yet year to date the stock is down 25.6% and it has returned negative 39.5% over 1 year and negative 78.6% over 5 years.

- These mixed returns have kept DocuSign on a lot of watchlists, as some investors reassess their view of the business and its risks. Recent coverage has focused on how the stock’s longer term pullback compares with shorter term gains, which has naturally pushed valuation questions back to the forefront.

- On Simply Wall St’s 6 point valuation checklist, DocuSign currently scores a 3 out of 6. This suggests some indicators point to undervaluation while others are more cautious. Next we will walk through the different valuation approaches, then finish with a way to tie them together into a more complete view of the stock.

Find out why DocuSign's -39.5% return over the last year is lagging behind its peers.

Approach 1: DocuSign Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company could be worth today by projecting its future cash flows and discounting them back to the present using a required rate of return.

For DocuSign, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections. The latest twelve month Free Cash Flow is about $990.3 million. Analysts provide explicit forecasts for the next few years, and beyond that Simply Wall St extrapolates cash flows, including a projected Free Cash Flow of $1,258 million in 2031.

When all these projected cash flows are discounted back to today, the model arrives at an estimated intrinsic value of US$101.33 per share. Compared to the recent share price of about US$48.23, this implies the stock trades at roughly a 52.4% discount to this DCF estimate. This suggests that the market may be pricing in materially lower expectations than the model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests DocuSign is undervalued by 52.4%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: DocuSign Price vs Earnings

For a company that is generating profits, the P/E ratio is often a useful way to think about what you are paying for each dollar of earnings. It gives you a quick check on how the market is weighing those earnings against other opportunities.

What counts as a “normal” P/E depends a lot on expectations and risk. Higher expected growth or stronger perceived resilience can support a higher multiple, while more uncertainty or weaker outlook usually justifies a lower one.

DocuSign currently trades on a P/E of about 32x. That sits above the broader Software industry average of around 26.9x, but below the peer average of roughly 36.3x. Simply Wall St also estimates a Fair Ratio for DocuSign of 29.9x. This is a proprietary figure that blends factors like earnings growth, margins, industry, market cap and risk profile into a single “fit for this company” multiple.

Because the Fair Ratio is tailored to DocuSign, it can be more informative than a simple comparison with generic industry or peer averages. With the current P/E of 32x sitting modestly above the Fair Ratio of 29.9x, the shares look slightly expensive on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your DocuSign Narrative

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St's Community page you can use Narratives, where you build a simple story for DocuSign, plug in your own assumptions for future revenue, earnings and margins, link that story to a forecast and fair value, then compare that Fair Value to the current price. The platform keeps your view updated as new news or earnings arrive, and you can see how one investor might land on a higher fair value near US$117 per share while another lands closer to US$53, all using the same company data but different perspectives.

Do you think there's more to the story for DocuSign? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DOCU

DocuSign

Provides electronic signature solution in the United States and internationally.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4342.5% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7833.2% undervalued

31 followersusers have followed this narrative

5 commentsusers have commented on this narrative

18 likesusers have liked this narrative

ST

SteveGruber on Warner Bros. Discovery ·

The Rising Deal Risk That Helped Sink Netflix’s $72 Billion Bid for Warner Bros. Discovery

Fair Value:US$18.1752.7% overvalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6435.3% undervalued

35 followersusers have followed this narrative

3 commentsusers have commented on this narrative

17 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on Circle Internet Group ·

Circle Internet Group (CRCL): The Programmable Dollar Powerhouse – Post-IPO Momentum and Stablecoin Dominance.

Fair Value:US$1206.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on TTM Technologies ·

TTM Technologies (TTMI): The Backbone of the AI Tsunami and Defense Modernization.

Fair Value:US$119.7319.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Bloom Energy ·

Bloom Energy Corp (BE): The AI "Bridge-to-Power" – Scaling to 2GW Capacity for the Next-Gen Data Center.

Fair Value:US$160.65.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.2% undervalued

51 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.8% undervalued

1102 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59631.3% undervalued

1302 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative