Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DDOG

Datadog (DDOG): Assessing Valuation After New Security and Cloud Marketplace Partnerships

Datadog (DDOG) just rolled out two client focused partnerships: one with Contrast Security to sharpen application threat detection inside Cloud SIEM and another with Flywl to simplify how enterprises buy and manage Datadog across cloud marketplaces.

See our latest analysis for Datadog.

Those partnerships land at an interesting moment for the stock, with a 30 day share price return of minus 20.83 percent but a 90 day share price return still up 10.97 percent, and a three year total shareholder return of 103.07 percent, which suggests that long term momentum is intact even as short term sentiment cools.

If these moves have you rethinking your exposure to software infrastructure, it could be worth exploring other high growth tech and AI names. You can use our high growth tech and AI stocks as a starting list of ideas.

With shares still more than 25 percent below estimated intrinsic value and trading at a roughly 40 percent discount to analyst targets, investors now face a pivotal question: is this a genuine buying window, or is future growth already priced in?

Most Popular Narrative Narrative: 28.6% Undervalued

Datadog's most popular narrative pegs fair value at roughly $211.97 per share versus a last close of $151.41, framing the stock as materially mispriced and setting up an aggressive long term growth story.

Ongoing product innovation (e.g., autonomous AI agents, enhanced security modules, expanded log and data observability) is increasing platform breadth and relevance, providing cross-selling opportunities and driving higher average revenue per user and net retention rate, which in turn improves recurring revenue predictability and gross margins.

Want to see the math behind this punchy upside case? The narrative leans on rapid scaling revenues, expanding margins, and a future earnings multiple that only elite software names usually command. Curious which specific growth and profitability assumptions justify that premium valuation path? Read on to uncover the projections driving this fair value call.

Result: Fair Value of $211.97 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upbeat path depends on Datadog dodging key risks, including hyperscaler competition and large AI customers aggressively optimizing, or even insourcing, observability spend.

Find out about the key risks to this Datadog narrative.

Another Angle on Valuation

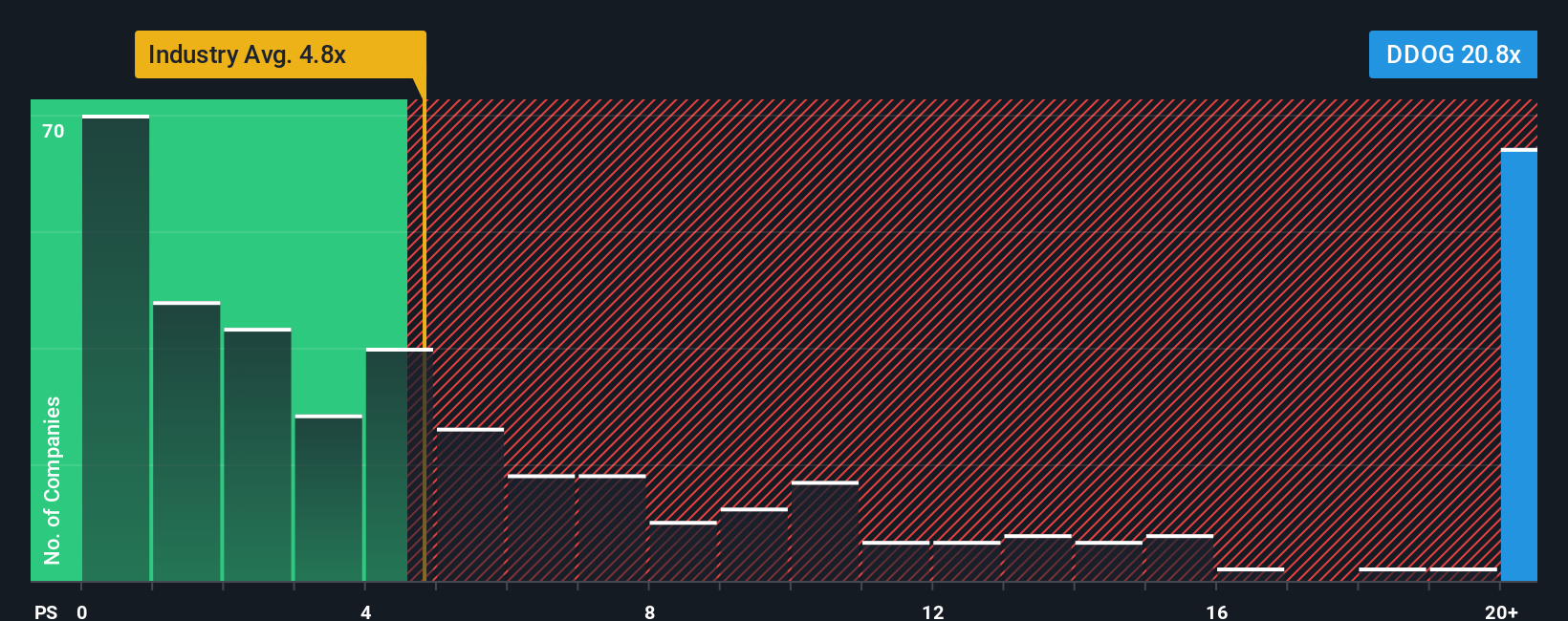

There is a catch, though. On a price to sales basis, Datadog looks expensive, trading at 16.5 times sales versus 7.4 times for peers and 4.9 times for the broader US software group, and even above its own 13.3 times fair ratio estimate. This points to meaningful multiple compression risk if growth stumbles.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Datadog Narrative

If you are not convinced by this view, or simply prefer to dig into the numbers yourself, you can build a custom Datadog thesis in just a few minutes, Do it your way.

A great starting point for your Datadog research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next set of opportunities by putting the Simply Wall St Screener to work across different themes and risk profiles.

- Capture early stage growth stories with these 3575 penny stocks with strong financials that already show solid financial underpinnings instead of betting blindly on hype.

- Position your portfolio for the next wave of automation and intelligence by targeting these 26 AI penny stocks shaping everything from infrastructure to real world applications.

- Strengthen your income stream and potential total return by focusing on these 15 dividend stocks with yields > 3% that can reward patience year after year.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DDOG

Datadog

Operates an observability and security platform for cloud applications in the United States and internationally.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7057.9% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17044.9% undervalued

42 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38033.4% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7447.4% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

Recently Updated Narratives

DA

davidlsander on Atlas Salt ·

Once In A Life Time Deeply Discounted Recession Proof Utility

Fair Value:CA$2.9660.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PI

PittTheYounger on SSAB ·

SSAB in pole position when it comes to the combination of steel tariffs and the EU's investment drive

Fair Value:SEK 79.1721.8% overvalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CH

ChuckN on XPLR Infrastructure ·

Investor Thesis: Why XPLR Infrastructure Could Be Deeply Undervalued in an AI Power Cycle

Fair Value:US$56697.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7447.4% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9722.6% undervalued

57 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1933.2% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

0

|0

CO

composite32 on Ronesans Gayrimenkul Yatirim ·

Selamlar Teşekkürler.. Radarımda olan bir şirket değil, Halka açıklık oranı %40'ın üzerinde olan şir...

0

|0