Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DDOG

Assessing Datadog (DDOG) Valuation After Storage Management Launch and Upbeat Growth Guidance

Datadog (DDOG) just rolled out its new Storage Management solution, targeting cloud object storage costs for organizations dealing with data and AI heavy workloads. The announcement arrives alongside impressive year-over-year revenue growth and an uptick in full-year guidance.

See our latest analysis for Datadog.

Datadog’s momentum is showing no signs of fading, with a 15.6% gain in the last month and an impressive 41.5% total shareholder return over the past year. While the share price cooled slightly this week, recent product rollouts and upbeat guidance continue to feed long-term optimism.

If you’re curious which other tech innovators are riding strong trends, explore See the full list for free. for more discovery opportunities.

With Datadog’s robust growth and fresh guidance lifting expectations, investors must now weigh whether the recent rally leaves room for further gains or if the stock’s current price already captures much of its future potential.

Most Popular Narrative: 10.1% Overvalued

With Datadog’s widely followed fair value estimate at $168.91, the last close price of $185.97 pushes the stock into premium territory. This sets the stage for a valuation built around aggressive growth expectations and ongoing platform dominance.

Ongoing product innovation, such as autonomous AI agents, enhanced security modules, and expanded log and data observability, is increasing platform breadth and relevance. This provides cross-selling opportunities and drives higher average revenue per user and net retention rate, which in turn improves recurring revenue predictability and gross margins.

Want to know what powers Datadog’s hefty price tag? The growth forecasts, built on platform expansion and a jump in profitability, might surprise you. Can the business truly deliver the scale and margin leap that the narrative demands? Unpack the make-or-break projections fueling this forward-looking value call.

Result: Fair Value of $168.91 (OVERVALUE D)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent heavy R&D investment and mounting competition from cloud hyperscalers could put pressure on Datadog’s margins and future growth outlook.

Find out about the key risks to this Datadog narrative.

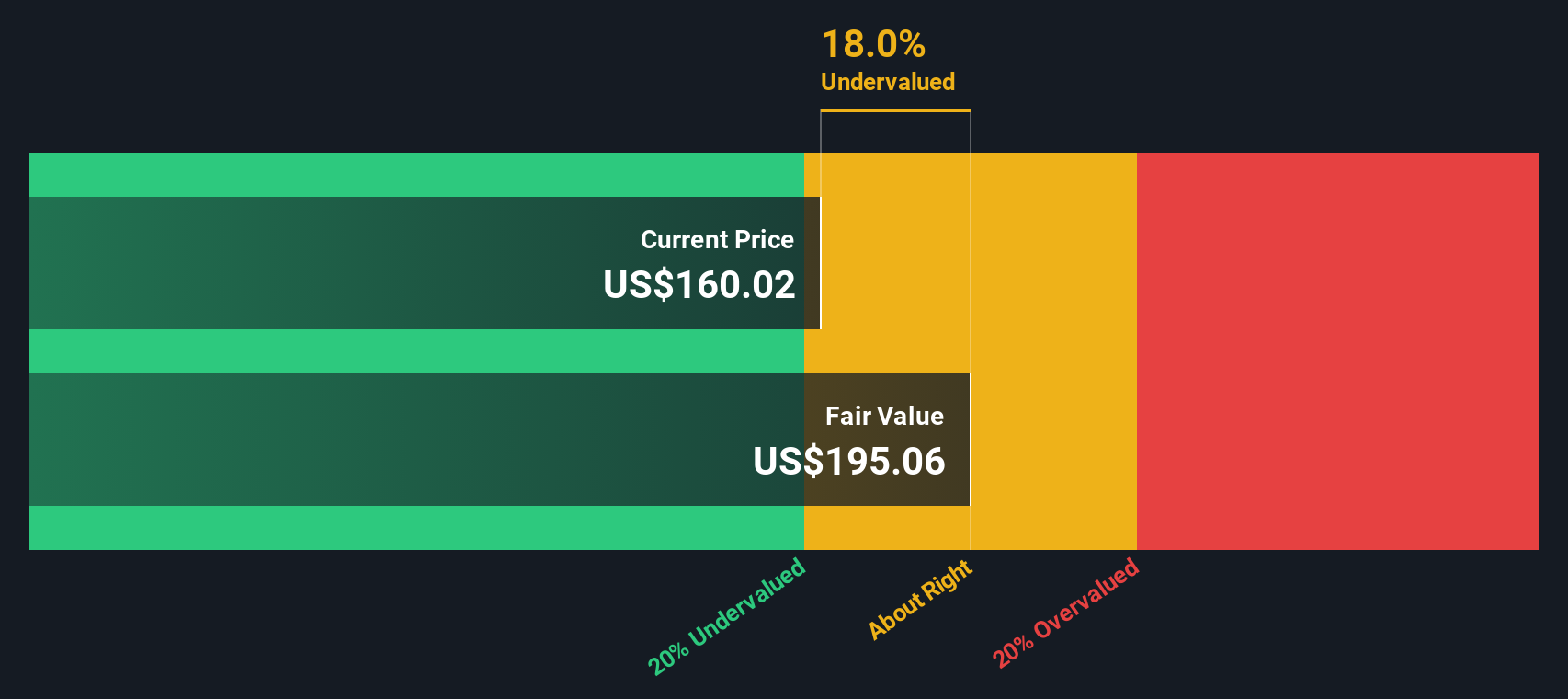

Another View: DCF Model Offers a Different Signal

Looking at our SWS DCF model, a different story emerges. Datadog's current share price is about 11.7% below its estimated fair value of $210.50. This suggests that, despite premium outlooks from multiples, there may be more upside left than the overvalued narrative implies. Could this signal justify further optimism, or does it flag hidden risks beneath the surface?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Datadog for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 885 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Datadog Narrative

If you have a different take on Datadog’s outlook or want to dig into the data yourself, you can craft your own story in just minutes. Do it your way

A great starting point for your Datadog research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Seize the chance to uncover tomorrow’s standout stocks with unique angles and growth potential. Don’t let the next opportunity pass you by.

- Tap into future healthcare breakthroughs by checking out these 31 healthcare AI stocks and see which companies are advancing AI-driven patient solutions.

- Spot value before the crowd by reviewing these 885 undervalued stocks based on cash flows, where cash flow fundamentals highlight companies trading below their intrinsic worth.

- Boost passive income potential by considering these 15 dividend stocks with yields > 3% featuring businesses offering reliable yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DDOG

Datadog

Operates an observability and security platform for cloud applications in the United States and internationally.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5370.8% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HE

HegelBayeBagel on PlaySide Studios ·

PlaySide Studios: Market Is Sleeping on a Potential 10M+ Unit Breakout Year, FY26 Could Be the Rerate of the Decade

Fair Value:AU$0.8460.7% undervalued

12 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

AN

AnimalDoctorKwon on Inotiv ·

Inotiv NAMs Test Center

Fair Value:US$1.278.3% undervalued

20 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

TH

TheValueDetector on Cognyte Software ·

This isn’t speculation — this is confirmation.A Schedule 13G was filed, not a 13D, meaning this is passive institutional capital, not acti

Fair Value:US$95.6792.9% undervalued

39 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

Recently Updated Narratives

AS

ASP on Rio Tinto Group ·

Rio Tinto (RIO): Cash Machine with a China Beta Problem — and a Copper Glow-Up

Fair Value:UK£69.782.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnimalDoctorKwon on Inotiv ·

Inotiv NAMs Test Center

Fair Value:US$1.278.3% undervalued

20 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

UN

unknown on Goldman Sachs Group ·

Goldman Sachs Group (GS) The Titan Reclaims Its Crown: Return to Core Excellence

Fair Value:US$1.06k12.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.887.9% undervalued

61 followersusers have followed this narrative

5 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.4% undervalued

1292 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TA

Talos on Tesla ·

The "Physical AI" Monopoly – A New Industrial Revolution

Fair Value:US$665.3638.1% undervalued

47 followersusers have followed this narrative

19 commentsusers have commented on this narrative

22 likesusers have liked this narrative

Trending Discussion

TH

TheInvestingFool on PlaySide Studios ·

Looks interesting, I am jumping into the finances now. Your 15% margin seems high for a conservative model, can't just ignore the years they need to invest. You didnt seem to mention that they had to dilute the sharebase by issuing ~40mil shares. raising ~8 mil. should be enough if mouse does OK. If not they will need to raise more to suvive. Losing 20m a year, 14m after there 6m cutbacks. Am I reading it right that they have no debt. have they any history of raising debt? First look it is too dependant on the mouse and GoT games. they do well stock will 2-3x, poorly and it will drop. I am not sure I agree with your work for hire backstop. Unlikely meta horizons will continue with the same size contract going forward. say 10% margins and 15x multiple on 30m. that is 45m, which with the new sharecount is 10c. It is a backstop but maybe not that strong. Mouse fails and devs could start jumping ship and outside contracts could dry up. Hmm on top of all that AI could be disrupting the work for hire model. I think I have mostly talked myself out of it. Although Mouse looks good and does seem like the type of game that could go viral on twitch for a few months. If it does you will likly get a great return 5x plus. crap maybe I am talking myself back in.

1

|0