Advertisement

- United States

- /

- Software

- /

- NasdaqGS:CVLT

Commvault Systems Q3 Margins Compressed To 7.3% Net Margin Challenge Bullish Growth Narrative

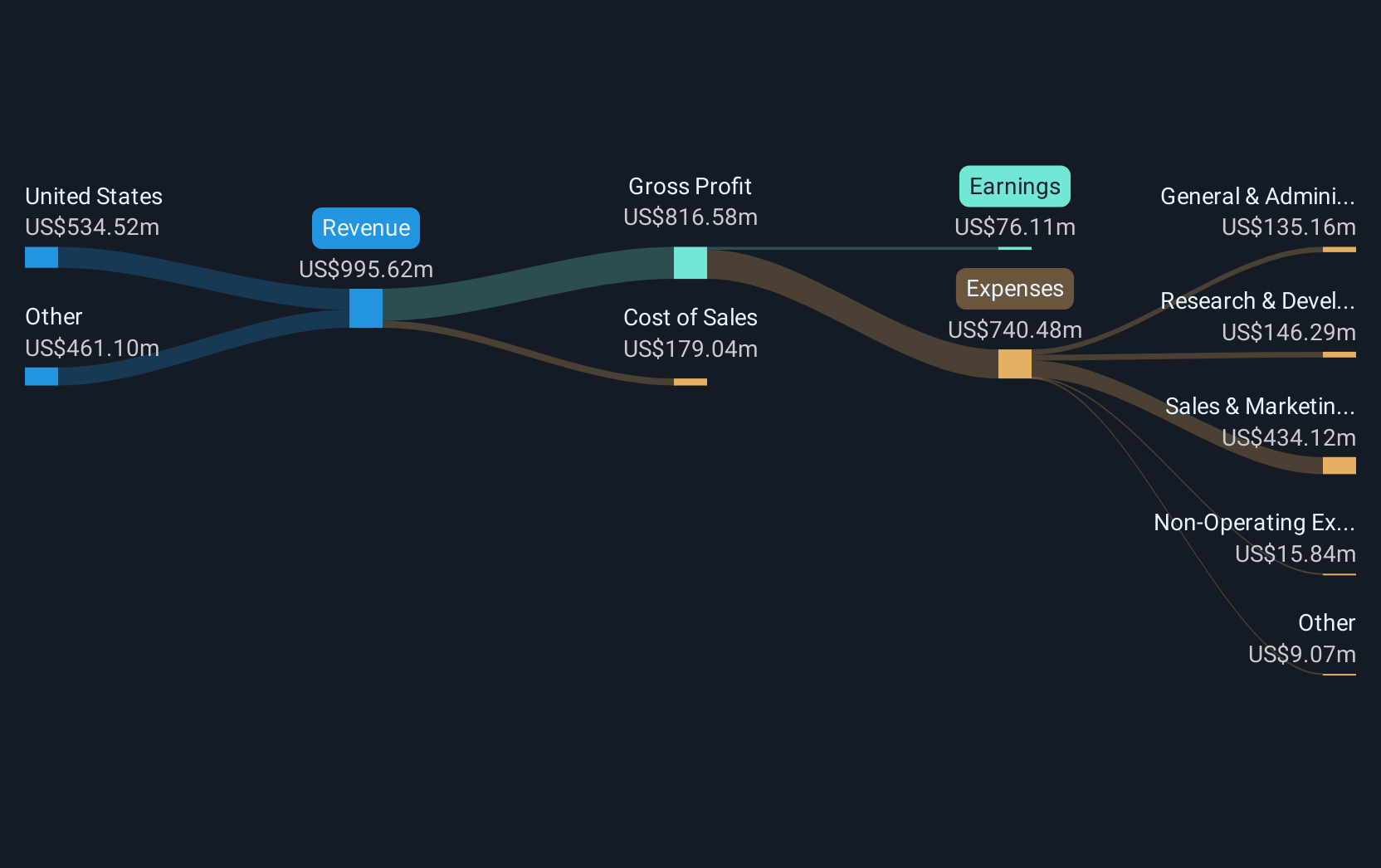

Commvault Systems (CVLT) opened its Q3 2026 scorecard with total revenue of US$313.8 million and basic EPS of US$0.40, alongside net income excluding extra items of US$17.8 million. This gives investors a fresh read on how the business is scaling. The company has seen quarterly revenue move from US$262.6 million in Q3 2025 to US$313.8 million in Q3 2026, while basic EPS shifted from US$0.25 to US$0.40 over the same period. This sets the backdrop for a discussion that now centers on how margins are holding up as growth plays through the income statement.

See our full analysis for Commvault Systems.With the headline numbers on the table, the next step is to see how this earnings print lines up against the widely followed growth and profitability narratives that have built up around Commvault over the past year.

Curious how numbers become stories that shape markets? Explore Community Narratives

Margins Squeezed, Even As Trailing Net Margin Sits At 7.3%

- Over the last 12 months, Commvault’s trailing net income excluding extra items was US$87.001 million on US$1.147b of revenue. This works out to a 7.3% net margin compared with 19.7% a year earlier.

- Bears focus on that margin step down, and the recent quarterly pattern gives them material support:

- Q3 2026 net income excluding extra items of US$17.782 million on US$313.832 million of revenue is below the prior trailing net margin level. Earlier quarters like Q4 2025 showed US$30.993 million on US$275.039 million.

- This sequence backs the bearish concern that profitability has been tighter over the last year, even as revenue moved from US$262.63 million in Q3 2025 to US$313.832 million in Q3 2026.

Forecast Earnings Growth Of 26.9% Versus Recent EPS Fluctuations

- On a trailing twelve month basis, basic EPS is US$1.97, built from quarterly EPS figures that ranged from US$0.25 in Q3 2025 up to US$0.70 in Q4 2025 and then US$0.40 in Q3 2026, alongside an earnings growth forecast of about 26.9% per year.

- Supporters of the bullish view lean on those growth forecasts, but the recent EPS pattern keeps the discussion grounded:

- Consensus narrative points to earnings expected to grow faster than the wider US market at roughly 26.9% per year, while the last four reported quarters show EPS moving between US$0.25 and US$0.70 rather than following a straight line.

- This combination heavily supports the bullish case for stronger long run earnings power, yet the quarter to quarter swings in reported EPS remind you that the path to that forecast is not perfectly smooth.

Premium Valuation With 49x P/E And US$168.83 Price Target

- The stock trades on a trailing P/E of 49x compared with a 30x P/E for the US software industry and about 45.2x for peers. The current share price of US$89.13 sits above a cited DCF fair value of roughly US$78.96 and below analysts’ implied price target of US$168.83.

- Critics highlight that premium as a key risk, yet the data also show why some investors still see room for upside:

- On one hand, the 49x P/E and price above the DCF fair value of about US$78.96 back the bearish argument that the shares are richly priced against both fundamentals and industry averages.

- On the other hand, analyst targets implying a move from US$89.13 to around US$168.83, together with the 26.9% earnings growth forecast and 10.8% revenue growth forecast, describe why some investors are comfortable paying above both the DCF fair value and sector P/E.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Commvault Systems's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Commvault’s compressed net margins and choppy quarterly EPS, alongside a 49x P/E above its DCF fair value, leave some investors questioning the price they are paying.

If paying up for that kind of earnings volatility feels uncomfortable, use our these 881 undervalued stocks based on cash flows to quickly focus on companies where current prices look more aligned with underlying fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CVLT

Commvault Systems

Provides cyber resiliency solutions for enterprises to protect, secure, and recover data, applications, and identity system.

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This OVERLOOKED Gold Stock Could TRIPLE - 3.3M Ounces, Bottom-of-Peer Valuation

Fair Value:CA$467.8% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9721.1% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1927.7% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$19.251.7% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$0.21.2k% overvalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DE

Delphic on NuScale Power ·

NuScale is Postioned For Long-Term Growth

Fair Value:US$10087.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Argenta Silver ·

Frank Giustra Backed: The High-Grade Silver Project Acquired for Just $3.5M Could Deliver 30x Silver Torque

Fair Value:CA$40.3598.7% undervalued

14 followersusers have followed this narrative

9 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.3% undervalued

116 followersusers have followed this narrative

2 commentsusers have commented on this narrative

33 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9721.1% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22040.4% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

32 likesusers have liked this narrative