- United States

- /

- Software

- /

- NasdaqCM:CLSK

Did CleanSpark's (CLSK) AI Data Center Pivot Just Redefine Its Long-Term Growth Narrative?

Reviewed by Sasha Jovanovic

- Earlier this week, CleanSpark announced the appointment of Jeffrey Thomas as Senior Vice President of AI Data Centers, marking its shift from exclusive Bitcoin mining to advanced AI infrastructure development in the United States.

- This move highlights CleanSpark's intent to leverage its existing power and land assets to diversify its business and pursue opportunities in high-performance AI computing.

- We'll examine how CleanSpark's entry into the AI data center sector with an experienced leader could alter its longer-term growth narrative.

Find companies with promising cash flow potential yet trading below their fair value.

CleanSpark Investment Narrative Recap

Owning CleanSpark shares requires confidence in the company's ability to transition from a largely Bitcoin mining business to an emerging player in the AI data center space. The recent appointment of Jeffrey Thomas as Senior Vice President of AI Data Centers may not materially impact the most important short-term catalyst, which remains CleanSpark’s leveraged exposure to Bitcoin price action, however, this pivot could help mitigate the biggest risk: the company’s outsized reliance on volatile crypto cycles.

Among the recent developments, CleanSpark’s opening of a US$100 million Bitcoin-backed credit facility in September stands out for its direct relevance, enabling the company to fund growth initiatives in its data center and high-performance computing expansion. This financial move could help CleanSpark better pursue efforts led by its new AI leadership, especially as it seeks to diversify and strengthen revenue amid shifting industry trends.

On the other hand, investors should be aware that CleanSpark’s business still faces significant hurdles if Bitcoin prices move unfavorably, putting revenue and margins at risk...

Read the full narrative on CleanSpark (it's free!)

CleanSpark's outlook anticipates $1.5 billion in revenue and $319.0 million in earnings by 2028. This is based on a 32.5% annual revenue growth rate and a $26.5 million earnings increase from the current $292.5 million.

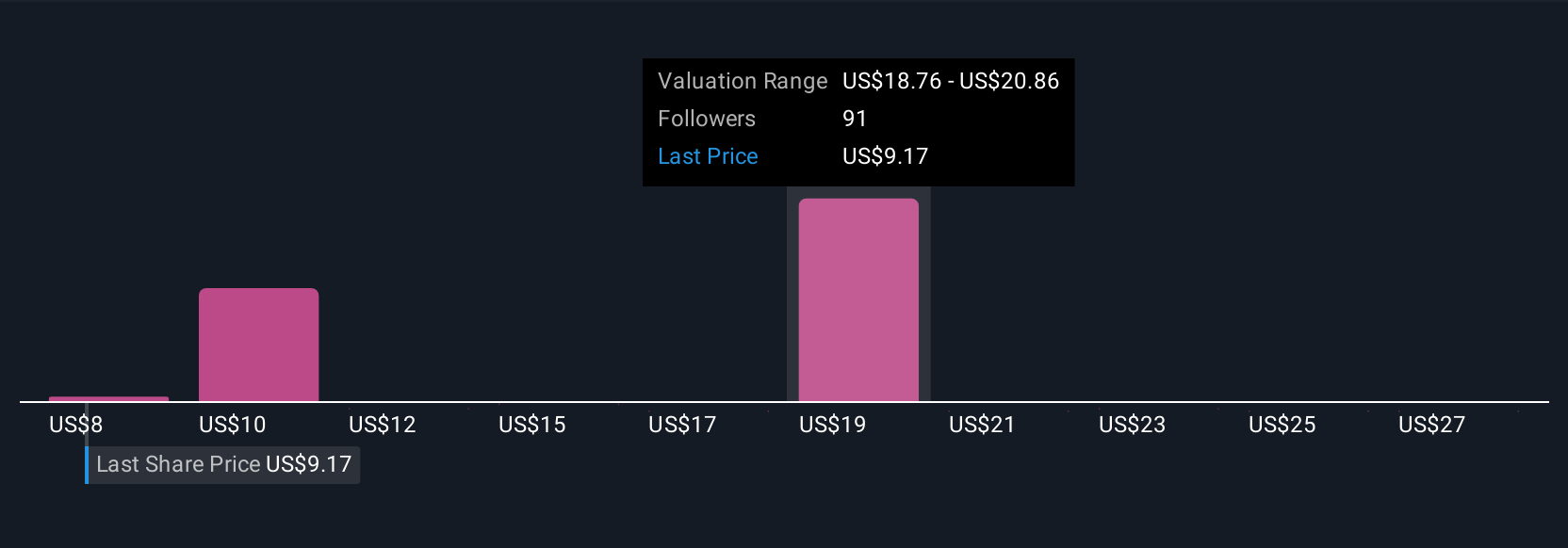

Uncover how CleanSpark's forecasts yield a $22.34 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Twenty individual analysts within the Simply Wall St Community set their fair value estimates for CleanSpark between US$5.20 and US$40, showing wide differences of opinion. Against this backdrop of diverging views, the company’s dependence on continued high Bitcoin prices remains a key consideration for future performance.

Explore 20 other fair value estimates on CleanSpark - why the stock might be worth less than half the current price!

Build Your Own CleanSpark Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CleanSpark research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CleanSpark research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CleanSpark's overall financial health at a glance.

No Opportunity In CleanSpark?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

- We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:CLSK

Slight risk and fair value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion