Advertisement

- United States

- /

- IT

- /

- NasdaqGM:CLPS

Returns On Capital At CLPS Incorporation (NASDAQ:CLPS) Paint A Concerning Picture

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. However, after investigating CLPS Incorporation (NASDAQ:CLPS), we don't think it's current trends fit the mold of a multi-bagger.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on CLPS Incorporation is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.10 = US$3.9m ÷ (US$66m - US$28m) (Based on the trailing twelve months to December 2020).

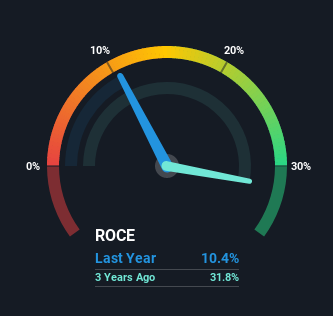

Therefore, CLPS Incorporation has an ROCE of 10%. That's a relatively normal return on capital, and it's around the 12% generated by the IT industry.

See our latest analysis for CLPS Incorporation

Historical performance is a great place to start when researching a stock so above you can see the gauge for CLPS Incorporation's ROCE against it's prior returns. If you're interested in investigating CLPS Incorporation's past further, check out this free graph of past earnings, revenue and cash flow.

What Can We Tell From CLPS Incorporation's ROCE Trend?

In terms of CLPS Incorporation's historical ROCE movements, the trend isn't fantastic. To be more specific, ROCE has fallen from 23% over the last four years. However, given capital employed and revenue have both increased it appears that the business is currently pursuing growth, at the consequence of short term returns. And if the increased capital generates additional returns, the business, and thus shareholders, will benefit in the long run.

On a side note, CLPS Incorporation has done well to pay down its current liabilities to 42% of total assets. So we could link some of this to the decrease in ROCE. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE. Keep in mind 42% is still pretty high, so those risks are still somewhat prevalent.

In Conclusion...

While returns have fallen for CLPS Incorporation in recent times, we're encouraged to see that sales are growing and that the business is reinvesting in its operations. And there could be an opportunity here if other metrics look good too, because the stock has declined 64% in the last three years. As a result, we'd recommend researching this stock further to uncover what other fundamentals of the business can show us.

One more thing, we've spotted 4 warning signs facing CLPS Incorporation that you might find interesting.

While CLPS Incorporation isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGM:CLPS

CLPS Incorporation

Provides information technology (IT), consulting, and solutions to institutions operating in banking, insurance, and financial sectors in the People’s Republic of China and internationally.

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|43.0% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|18.3% undervalued

BL

Community Contributor