Cellebrite DI (CLBT) has been attracting interest given its recent share movement and the company's evolving position in digital intelligence solutions. Investors have noticed the stock’s mixed performance over the past month and year, which is driving conversation about future prospects.

Momentum around Cellebrite DI has seen its ups and downs, with a sharp 18.3% dip in the past month hinting at shaken confidence. However, the company’s longer-term story remains compelling, underscored by a 221.9% total shareholder return over the last three years.

If the recent swings in tech stocks have you curious, this could be the right time to discover See the full list for free.

The real question now is whether Cellebrite DI’s recent pullback signals an undervalued opportunity for investors, or if the market is already factoring in its growth prospects and future momentum. Is now the time to buy?

Advertisement

Most Popular Narrative: 32.5% Undervalued

With the most popular narrative fair value sitting well above Cellebrite DI’s last closing price, the market may be missing optimism on future growth and profit turnaround. The current stage is set for upside, provided the company's transformation plans deliver and industry dynamics work in its favor.

The accelerating shift by law enforcement and intelligence agencies toward more advanced digital investigation platforms, driven by surging digitalization, larger data volumes, and increasing crime sophistication, is fueling rapid adoption of Cellebrite's cloud/SaaS solutions and digital forensics platforms (Inseyets, Guardian, Pathfinder). This trend is expected to drive continued double-digit subscription revenue and ARR growth over the coming years.

Want to know the catalyst behind this bullish estimate? This narrative hinges on a leap from unprofitability to sizeable profits, fueled by bold assumptions on growth, margins and recurring revenue dominance. Discover what dramatic profit turnaround and future premium is driving this high fair value.

However, concerns persist that future U.S. federal budget constraints or regulatory shifts could slow Cellebrite’s growth trajectory and challenge analyst optimism.

Another View: Multiple-Based Valuation Raises Questions

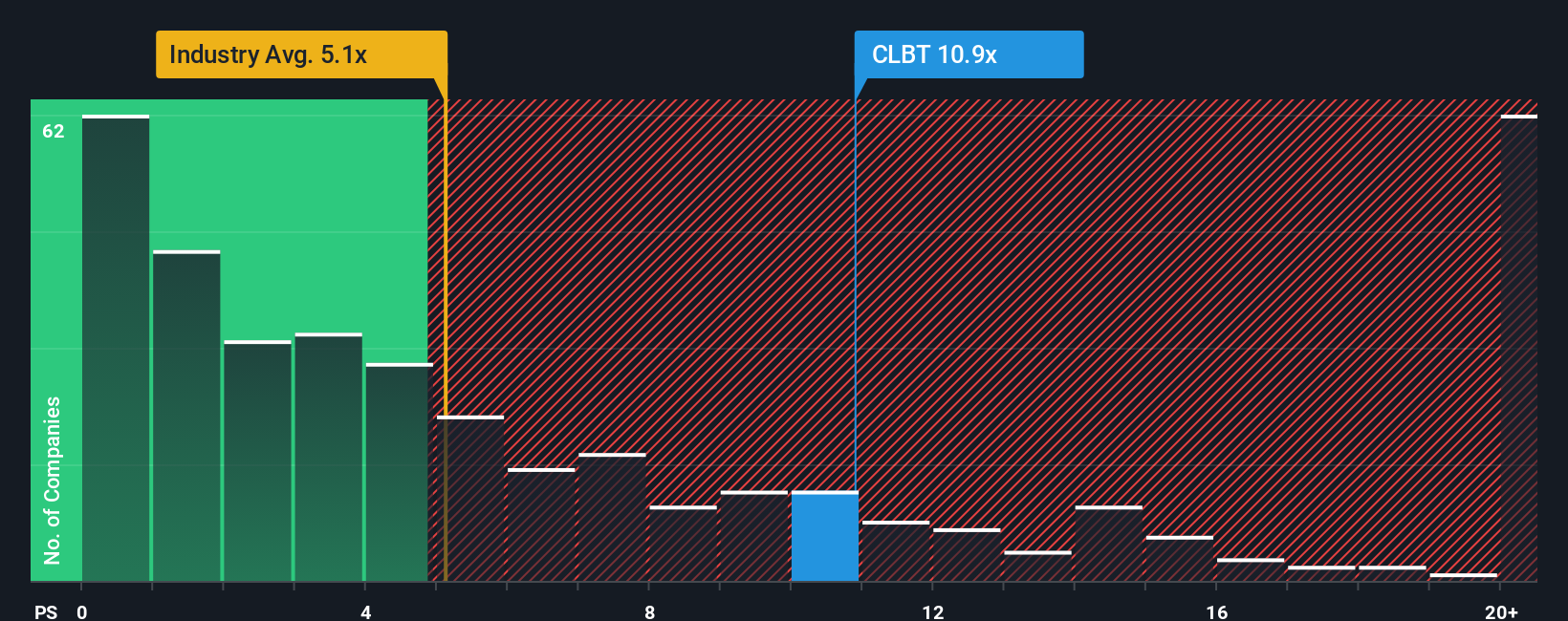

Looking at Cellebrite DI through the lens of its price-to-sales ratio, a different picture emerges. The company trades at 8.7x sales, making it appear far more expensive than both the US Software industry average of 4.8x and its peer group at 6.3x. Even compared to the fair ratio of 6.5x, Cellebrite looks richly valued, which suggests the market is already pricing in a lot of future success. Could investors be overlooking valuation risk in the excitement about growth?

If the numbers and arguments above don't line up with your own view, dive into the data and craft your version of Cellebrite's story in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Cellebrite DI.

Looking for more investment ideas?

Don’t limit yourself to just one opportunity. With the right strategies and tools, you can stay ahead of market moves and uncover stocks worth your attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies