Advertisement

- United States

- /

- Software

- /

- NasdaqGS:CHKP

Check Point Software Technologies' (NASDAQ:CHKP) Solid Earnings Have Been Accounted For Conservatively

Check Point Software Technologies Ltd.'s (NASDAQ:CHKP) recent earnings report didn't offer any surprises, with the shares unchanged over the last week. We did some analysis to find out why and believe that investors might be missing some encouraging factors contained in the earnings.

We check all companies for important risks. See what we found for Check Point Software Technologies in our free report.

Zooming In On Check Point Software Technologies' Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

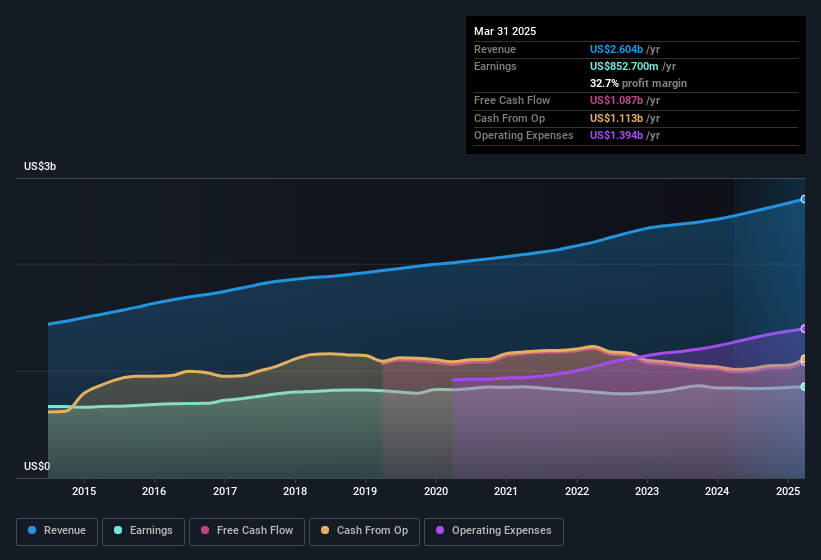

For the year to March 2025, Check Point Software Technologies had an accrual ratio of -0.19. That indicates that its free cash flow quite significantly exceeded its statutory profit. To wit, it produced free cash flow of US$1.1b during the period, dwarfing its reported profit of US$852.7m. Check Point Software Technologies' free cash flow improved over the last year, which is generally good to see.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Check Point Software Technologies' Profit Performance

As we discussed above, Check Point Software Technologies' accrual ratio indicates strong conversion of profit to free cash flow, which is a positive for the company. Based on this observation, we consider it possible that Check Point Software Technologies' statutory profit actually understates its earnings potential! And on top of that, its earnings per share have grown at 27% per year over the last three years. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. Obviously, we love to consider the historical data to inform our opinion of a company. But it can be really valuable to consider what other analysts are forecasting. At Simply Wall St, we have analyst estimates which you can view by clicking here.

This note has only looked at a single factor that sheds light on the nature of Check Point Software Technologies' profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:CHKP

Check Point Software Technologies

Develops, markets, and supports a range of products and services for IT security worldwide.

Outstanding track record and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0774.4% undervalued

214 followersusers have followed this narrative

1 commentusers have commented on this narrative

30 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.4% undervalued

54 followersusers have followed this narrative

2 commentsusers have commented on this narrative

21 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0716.3% undervalued

14 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3812.7% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

CG

CG86 on Bausch + Lomb ·

$BLCO & $COO The Silence BEFORE the AGM: A Retail Investor’s Timeline, Findings, and Opinion on SUSPICIOUS SILENCE!

Fair Value:US$39.2358.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on INTLOOP ·

Renewed focus on business investment

Fair Value:JP¥4.17k56.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GO

GoranLagea on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d. future looks bright with a profit margin change of 38%

Fair Value:€36036.7% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3956.1% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

42 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3136.9% undervalued

1350 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

37 followersusers have followed this narrative

11 commentsusers have commented on this narrative

31 likesusers have liked this narrative

Trending Discussion

EL

Element1 on Greatland Resources ·

I can’t believe how inaccurate and out of date this site is—and people rely on it. Greatland owns tw...

0

|0

MI

Mikeymike on Auxly Cannabis Group ·

Id like to understand why they believe the profit margin is going decline so dramatically. Is it ene...

0

|0