Advertisement

- United States

- /

- Software

- /

- NasdaqGS:CFLT

Is Confluent (NASDAQ:CFLT) A Risky Investment?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Confluent, Inc. (NASDAQ:CFLT) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Confluent

What Is Confluent's Net Debt?

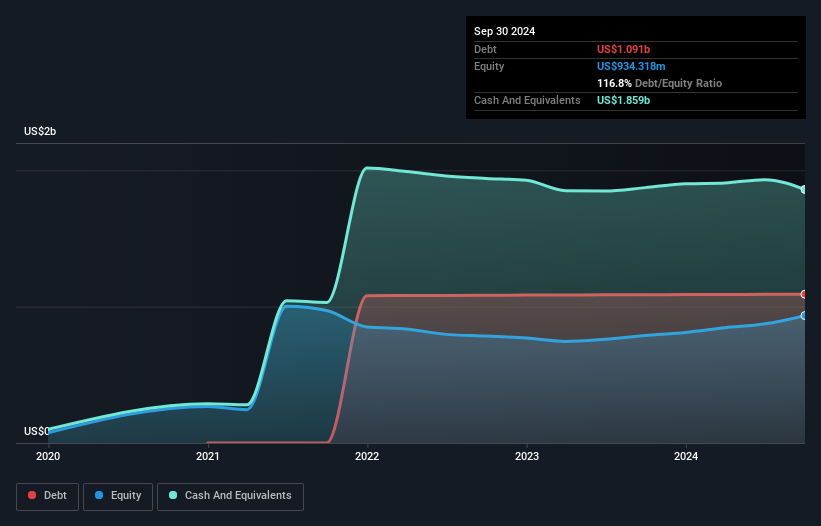

The chart below, which you can click on for greater detail, shows that Confluent had US$1.09b in debt in September 2024; about the same as the year before. However, its balance sheet shows it holds US$1.86b in cash, so it actually has US$768.3m net cash.

How Strong Is Confluent's Balance Sheet?

We can see from the most recent balance sheet that Confluent had liabilities of US$535.0m falling due within a year, and liabilities of US$1.14b due beyond that. On the other hand, it had cash of US$1.86b and US$278.7m worth of receivables due within a year. So it can boast US$464.5m more liquid assets than total liabilities.

This surplus suggests that Confluent has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Confluent has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Confluent's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, Confluent reported revenue of US$916m, which is a gain of 25%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Confluent?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Confluent lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$13m and booked a US$351m accounting loss. While this does make the company a bit risky, it's important to remember it has net cash of US$768.3m. That kitty means the company can keep spending for growth for at least two years, at current rates. With very solid revenue growth in the last year, Confluent may be on a path to profitability. By investing before those profits, shareholders take on more risk in the hope of bigger rewards. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 3 warning signs for Confluent you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:CFLT

Confluent

Operates a data streaming platform in the United States and internationally.

Excellent balance sheet with very low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This OVERLOOKED Gold Stock Could TRIPLE - 3.3M Ounces, Bottom-of-Peer Valuation

Fair Value:CA$471.5% undervalued

41 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17037.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38032.7% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.9% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

DC

DCA_rules on Micron Technology ·

Micron Technology (MU): Riding the AI Supercycle to a $100B+ Revenue Horizon and Historic 40%+ Net Profit Margins

Fair Value:US$1.25k17.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Aoyama Zaisan Networks CompanyLimited ·

Preparing for re-acceleration in FY12/27

Fair Value:JP¥1.31k0.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Freegold Ventures ·

Freegold Ventures, Eric Sprott is Betting Big on This 31 Moz Alaska Gold Beast

Fair Value:CA$33.0196.4% undervalued

15 followersusers have followed this narrative

5 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.2% undervalued

122 followersusers have followed this narrative

2 commentsusers have commented on this narrative

35 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9718.0% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1926.1% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

18 likesusers have liked this narrative