- United States

- /

- Software

- /

- NasdaqCM:BTDR

Bitdeer Technologies Group (NasdaqCM:BTDR) Sees 14% Dip After US$532 Million Net Loss Announced

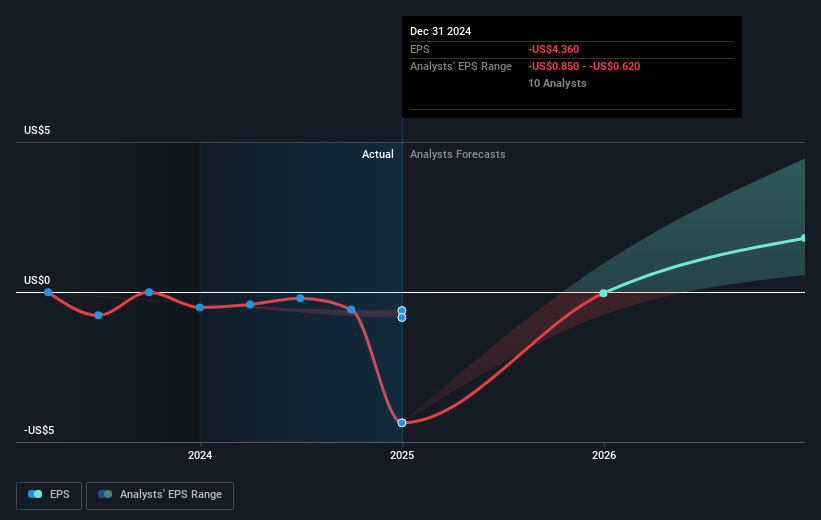

Bitdeer Technologies Group (NasdaqCM:BTDR) announced significant developments last week, including Q4 2024 results revealing a substantial net loss of USD 532 million, a stark contrast from the previous year, potentially influencing its 13.59% share price decline. Additionally, the company's announcement of a USD 20 million share repurchase program seems to have offered limited immediate reassurance to investors amidst the broader market downturn. The financial report reflected declining sales, amplifying concerns raised amidst a challenging economic landscape marked by fresh US tariffs impacting global trade dynamics. Notably, market indices also faced declines, with the S&P 500 falling 1.8%, suggesting that external pressures such as tariffs and economic uncertainties heavily influenced investor sentiment towards tech firms, including Bitdeer. This broad market sentiment, combined with Bitdeer's earnings performance, presents a comprehensive backdrop to the company's recent price movement.

Dig deeper into the specifics of Bitdeer Technologies Group here with our thorough analysis report.

Over the last year, Bitdeer Technologies Group delivered a total return of 65.74%, significantly outpacing both the US market and software industry benchmarks of 15.3% and 4.4%, respectively. Several pivotal events shaped this performance. The launch of advanced AI training platforms in August 2024 and the ReMine peer-to-peer market in January 2025 likely fueled investor optimism for future growth. Moreover, the company's strategic expansion through a 30-year lease for power capacity in June 2024 may have contributed to this positive sentiment.

In contrast, the last year presented financial hurdles, highlighted by a large increase in net losses, from US$56.66 million in 2023 to US$599.15 million in 2024. The ongoing share buyback initiatives, including the US$10 million repurchase completed in February 2025, might have counterbalanced some market skepticism, preserving shareholder confidence despite the volatile and challenging external factors.

- Analyze Bitdeer Technologies Group's fair value against its market price in our detailed valuation report—access it here.

- Discover the key vulnerabilities in Bitdeer Technologies Group's business with our detailed risk assessment.

- Is Bitdeer Technologies Group part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bitdeer Technologies Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:BTDR

Bitdeer Technologies Group

Operates as a technology company for blockchain and high-performance computing (HPC) in Singapore, the United States, Bhutan, and Norway.

Moderate risk with limited growth.

Similar Companies

Market Insights

Weekly Picks

Is this the AI replacing marketing professionals?

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

The Rising Deal Risk That Helped Sink Netflix’s $72 Billion Bid for Warner Bros. Discovery

The Infrastructure AI Cannot Be Built Without

Recently Updated Narratives

Near zero debt, Japan centric focus provides future growth

Promigas E.S.P looks to a promising future with 35% revenue growth

Kratos Defense & Security Solutions (KTOS): Scaling "Attritable" Dominance in a New Era of Aerial Conflict.

Popular Narratives

Nu holdings will continue to disrupt the South American banking market

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks