Advertisement

- United States

- /

- Software

- /

- NasdaqCM:BTBT

Assessing Bit Digital (BTBT) Valuation As CEO Samir Tabar Expands Digital Asset And Sustainable Mining Focus

Recent attention on CEO Samir "Sam" Tabar’s dual leadership at Bit Digital (BTBT) and WhiteFiber has put the company’s push into digital asset infrastructure, Bitcoin mining, and renewable powered data centers in focus for investors.

See our latest analysis for Bit Digital.

The recent focus on Samir Tabar’s leadership comes as Bit Digital’s share price sits at US$2.21, with a 1 day share price return of 8.33% and a 7 day share price return of 14.51%. However, the 90 day share price return of a 45.30% decline and the 1 year total shareholder return of a 38.95% decline point to momentum that has been pressured over the longer term, despite a very large 3 year total shareholder return.

If this kind of digital infrastructure story has your attention, it could be a good moment to widen the lens and see how other tech driven names stack up through high growth tech and AI stocks.

With the share price at US$2.21, a very large 3-year total return and an analyst price target of US$5.13, you have to ask: Is Bit Digital still undervalued, or is the market already pricing in future growth?

Most Popular Narrative: 58.9% Undervalued

The most followed narrative puts Bit Digital’s fair value at US$5.38 per share versus the last close at US$2.21, framing a sizeable valuation gap.

The company's structural pivot to become a dedicated Ethereum treasury and staking platform positions it to capitalize on the growing acceptance of Ethereum among institutional investors and asset managers, expected to drive future revenue growth through larger scale ETH holdings and increased staking yields.

Want to see what is baked into that gap? Revenue compounding, margin rebuild, and a premium earnings multiple all sit at the core of this narrative.

Result: Fair Value of $5.38 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on Ethereum concentration and reliance on third party staking partners, where sharper token swings or operational issues could quickly challenge today’s upbeat assumptions.

Find out about the key risks to this Bit Digital narrative.

Another Angle On Valuation

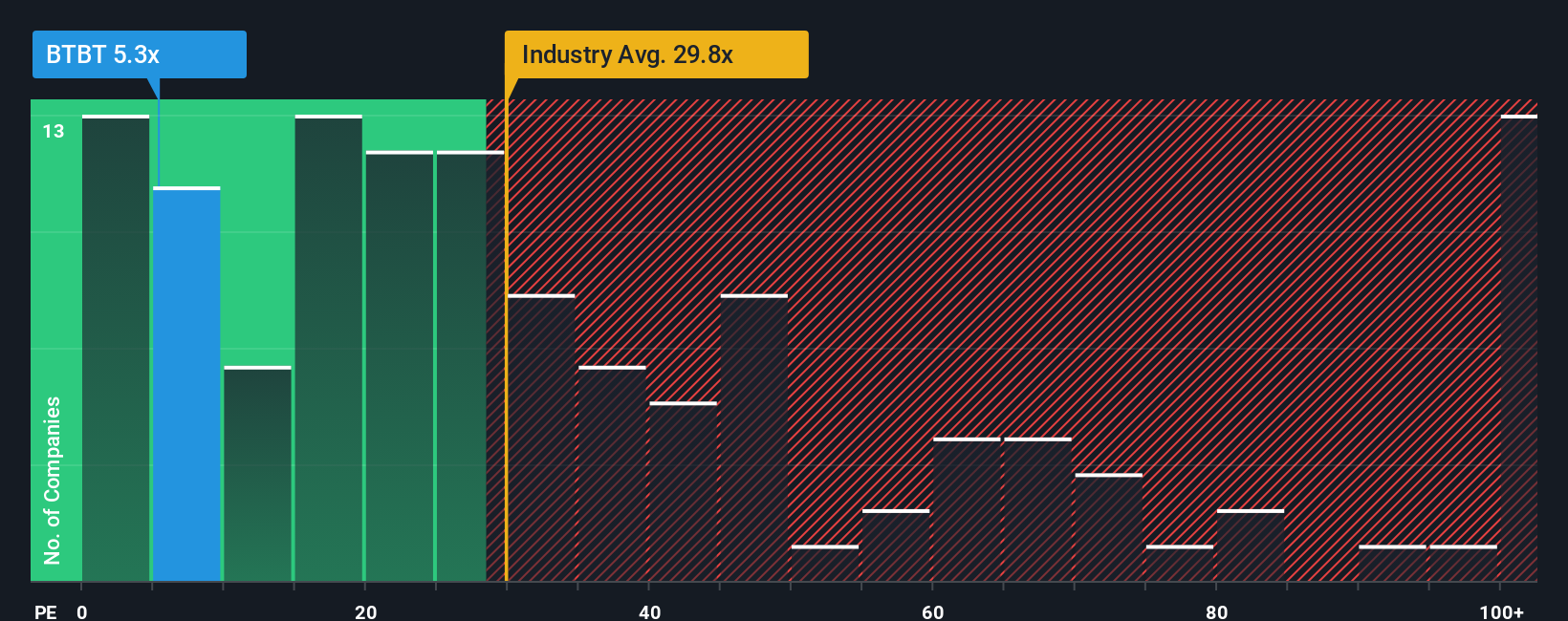

The narrative fair value of US$5.38 already suggests upside, but the earnings multiple tells a more complicated story. Bit Digital trades on a P/E of 5.2x, which looks cheap next to the US Software industry at 32.3x and peers at 31.6x, yet is above its fair ratio of 4.1x.

That gap hints at room for the share price to move either closer to richer software peers or back toward the lower fair ratio, depending on how you view its risks and earnings quality, especially the high level of non cash earnings. Which side of that trade off matters more to you right now?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Bit Digital Narrative

If you see the numbers differently or prefer to rely on your own work, you can test the data and develop a fresh thesis in minutes, then Do it your way.

A great starting point for your Bit Digital research is our analysis highlighting 3 key rewards and 5 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Bit Digital has sparked your interest, do not stop here, there are plenty of other opportunities worth putting on your radar.

- Target potential mispricings by reviewing these 880 undervalued stocks based on cash flows that might fit your return and risk preferences.

- Spot future facing themes by checking out these 25 AI penny stocks that are tied to artificial intelligence growth stories.

- Hunt for higher income potential with these 14 dividend stocks with yields > 3% that could complement more volatile growth names in your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bit Digital might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:BTBT

Bit Digital

Engages in the institutional grade ethereum treasury and staking business.

Fair value with low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1941.1% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

50 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.5% undervalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30154.5% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

AG

Agricola on Silver Storm Mining ·

A case for USD $26.00 (CAD 36.00) by 2030 with a MKT CAP of CAD$8.40 billion (USD$6.10) (10 bagger by Dec 2027)

Fair Value:CA$3698.8% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on First Mining Gold ·

First Mining Gold's competitive advantages in the mining sector.

Fair Value:CA$587.4% undervalued

23 followersusers have followed this narrative

4 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Central Asia Metals ·

A Case for Central Asia Metals to reach £8-12 by 2031 in a commodities bull market.

Fair Value:UK£1288.6% undervalued

2 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.6% undervalued

92 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5455.7% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3455.9% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

1

|0