Advertisement

- United States

- /

- Software

- /

- NasdaqGS:APP

Assessing AppLovin (APP) Valuation as Shares Rally on Solid Growth

Reviewed by Simply Wall St

If you have been following AppLovin (APP) recently, you might be wondering what is fueling all the interest in the stock. There is no headline event driving the latest move, but sometimes the absence of news can raise as many questions as a splashy announcement. Curious investors are left to read between the lines, weighing whether the stock’s current momentum is just noise or if it hints at something deeper occurring in the business or the market’s expectations.

This year, AppLovin’s share price has seen its fair share of swings, delivering a roughly 4.7% return over the past year and a bigger 43% gain since January. Momentum has been building over the past three months as shares have jumped by 28%, and their annual revenue and profit growth numbers look solid compared to many of their software peers. No single event stands out right now, but that steady growth and price movement could be signaling a shift in how the market values AppLovin’s long-term prospects.

So is AppLovin offering investors a real buying opportunity at these levels, or is the market already betting heavily on future growth?

Most Popular Narrative: 1.8% Undervalued

The consensus among analysts is that AppLovin is trading just below its fair value, with only a slight discount implied by recent projections and underlying assumptions.

"Expanded rollout of the self-service AXON ads manager and Shopify integration is expected to open AppLovin's platform to a massive new base of small and mid-sized advertisers globally, dramatically increasing advertiser count and driving sustained uplift in topline revenue."

Wondering what is fueling AppLovin's near-fair valuation? Is it possible for the company to maintain this momentum? The main factor in this story is a bold projection for future growth, powered by significant product moves and ambitious margin upgrades. Interested in which financial milestones analysts are anticipating? Learn how these estimates could influence perceptions of value.

Result: Fair Value of $499.14 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, tightening privacy regulations and AppLovin’s reliance on third-party mobile platforms could create challenges for its growth thesis going forward.

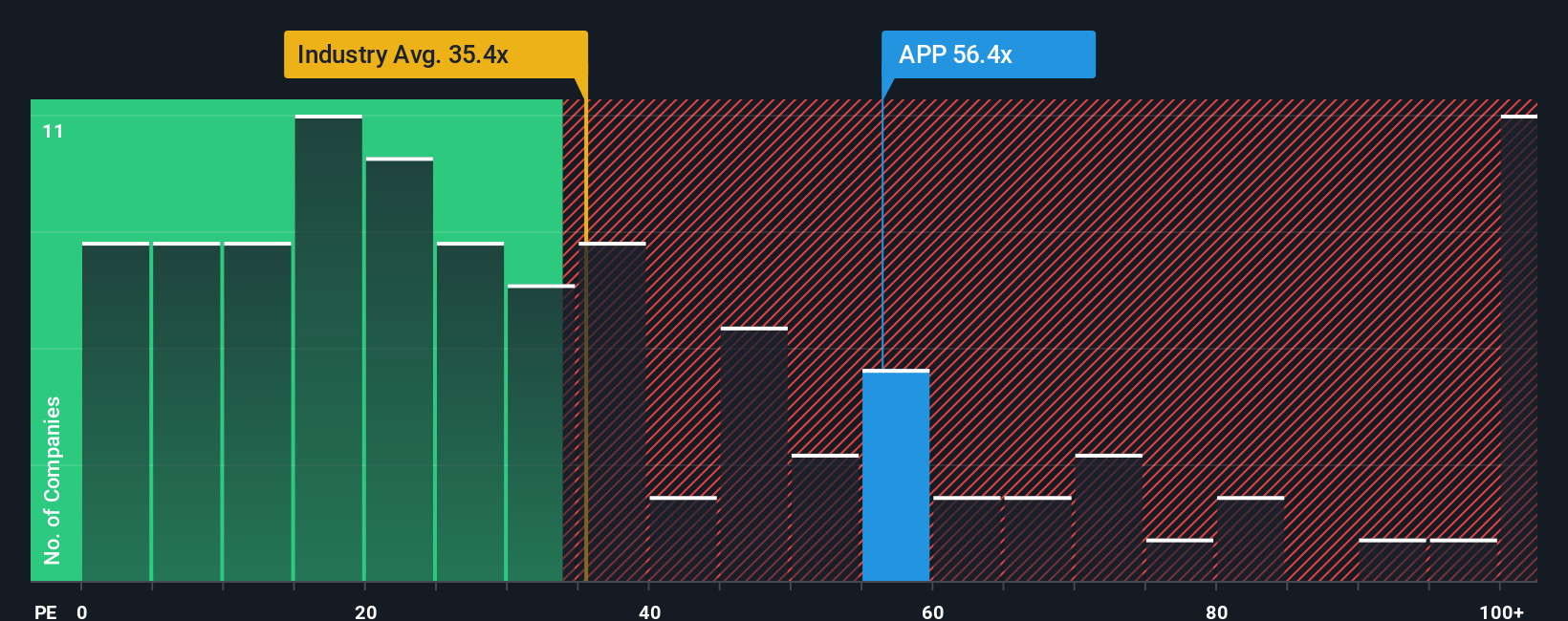

Find out about the key risks to this AppLovin narrative.Another View: Valuing AppLovin by Industry Comparison

Looking at AppLovin through the lens of a simple price-to-earnings comparison with other US software companies provides a less flattering view. This suggests the stock appears expensive at current levels. Could this indicate the market is too optimistic?

See what the numbers say about this price — find out in our valuation breakdown.

Stay updated when valuation signals shift by adding AppLovin to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own AppLovin Narrative

If you see things differently, or would rather dig into the numbers on your own, you can craft a personalized take in just a few minutes. Do it your way

A great starting point for your AppLovin research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Don’t stick with just one pick when new opportunities are waiting. Use these curated screens to spot stocks that match your strategy and get ahead of the crowd.

- Uncover hidden value with companies trading below their true worth by using undervalued stocks based on cash flows to target overlooked opportunities.

- Build your passive income stream by searching for dividend stocks with yields > 3% outperforming others with reliable and attractive yields.

- Catch the next big wave in technology. Explore what’s leading the future with quantum computing stocks and position yourself for tomorrow’s breakthroughs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:APP

AppLovin

Provides end-to-end artificial intelligence-powered advertising solutions for businesses in the United States and internationally.

Exceptional growth potential with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2542.9% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$482.3% overvalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5450.6% undervalued

50 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$825.3% undervalued

26 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

PR

Premium_Bobcat_cwey on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6530.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Space Exploration Technologies ·

WHY YOU SHOULD NOT BUY THE SPACEX IPO

Fair Value:US$50224.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HI

Hidden_Rock_Capital on Fiserv ·

Temporary "perfect storm" leads to opportunity to buy financial services leader for less than 5x long-term earnings

Fair Value:US$119.9956.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.1% undervalued

80 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.3% undervalued

63 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7440.1% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative