- United States

- /

- Software

- /

- NasdaqGS:ADBE

Can Adobe's (ADBE) AI Push in Travel Redefine Its Competitive Edge?

Reviewed by Sasha Jovanovic

- Red Sea Global recently announced a partnership selecting Adobe for Business products as the foundation for personalized digital experiences on VisitRedSea.com, with implementation led by technology partner Globant.

- This collaboration showcases Adobe’s ongoing expansion into large-scale, AI-powered solutions designed for the travel and hospitality sector, broadening the scope of its digital experience offerings beyond traditional creative markets.

- We'll examine how Adobe's growing role as a provider of AI-driven digital platforms for clients like Red Sea Global may influence its investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Adobe Investment Narrative Recap

To be a shareholder in Adobe, you need to believe in the company's ability to drive growth by expanding its AI-powered digital experiences beyond its creative core. The recent Red Sea Global partnership highlights this push into new verticals but does not materially change the most immediate catalyst, Adobe's pace of innovation in AI or its biggest risk, which remains intensifying competition in AI and digital media.

Of recent announcements, Adobe’s collaboration with Qualcomm, where it used GenStudio’s generative AI to streamline marketing, stands out as especially relevant. This move directly supports the catalyst of expanding enterprise AI adoption to boost higher value contracts and revenue growth by demonstrating how Adobe’s latest tools are being embedded in large-scale, data-driven client campaigns.

By contrast, investors should also keep an eye on the operational challenges Adobe faces when integrating third-party AI alongside its own tools, which could affect net margins if implementation becomes complex or costly…

Read the full narrative on Adobe (it's free!)

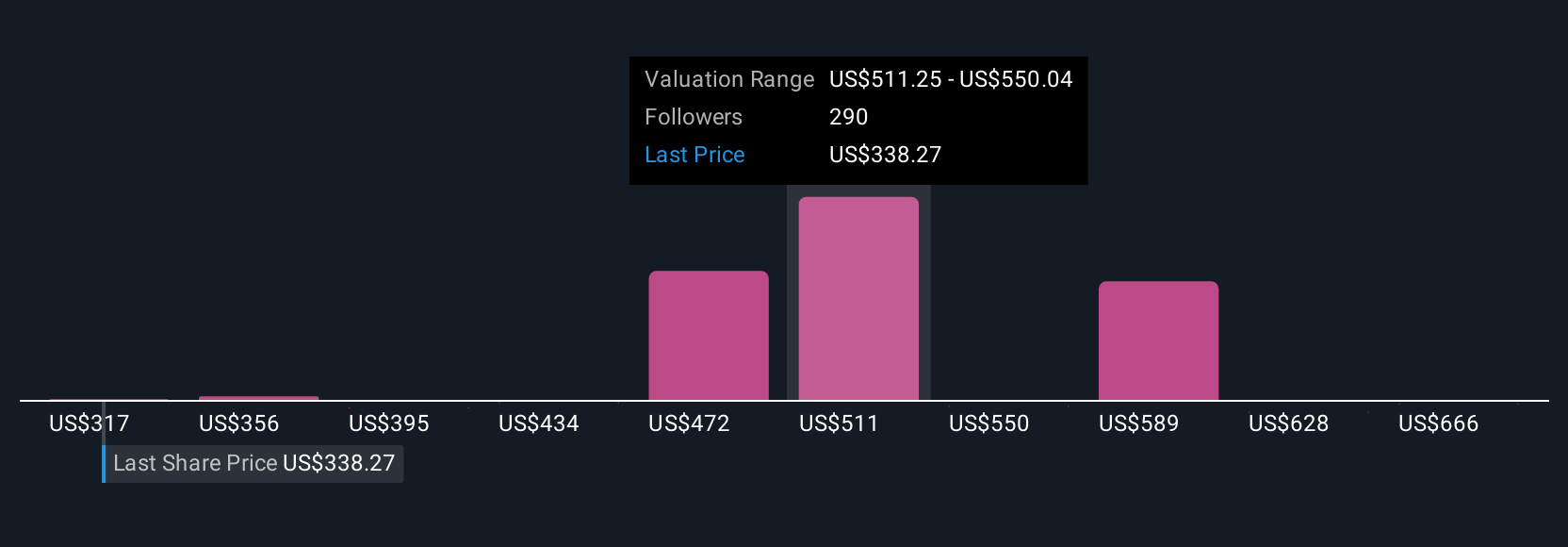

Adobe's outlook projects $29.3 billion in revenue and $8.7 billion in earnings by 2028. This reflects a 9.0% annual revenue growth rate and a $1.8 billion increase in earnings from the current $6.9 billion.

Uncover how Adobe's forecasts yield a $456.18 fair value, a 38% upside to its current price.

Exploring Other Perspectives

Compared to consensus, the lowest analysts take a more cautious approach, forecasting slower annual revenue growth at just 7 percent and predicting that profit margins could steadily decline. If you identify with these estimates, you should know views on risks like heavy reliance on AI features and new growth strategies can really diverge. Explore how upcoming news could shift even the most pessimistic of forecasts in the US$8 billion earnings range.

Explore 106 other fair value estimates on Adobe - why the stock might be worth over 2x more than the current price!

Build Your Own Adobe Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Adobe research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Adobe research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Adobe's overall financial health at a glance.

Searching For A Fresh Perspective?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Rare earth metals are the new gold rush. Find out which 39 stocks are leading the charge.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ADBE

Outstanding track record and undervalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Hemisphere Energy Looks Forward to a Remarkable 38% Profit Margin Surge

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion