- United States

- /

- Aerospace & Defense

- /

- NYSE:HWM

3 US Stocks That May Be Undervalued In August 2024

Reviewed by Simply Wall St

As of July 2024, the US stock market has shown significant resilience, with the S&P 500 and Nasdaq closing sharply higher amid a rally in chip stocks and growing optimism about potential interest rate cuts. Investors are closely watching Federal Reserve signals and economic indicators to gauge future market movements. In this environment, identifying undervalued stocks can be particularly rewarding. A good stock typically exhibits strong fundamentals, growth potential, and is trading below its intrinsic value relative to current market conditions.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Atlanticus Holdings (NasdaqGS:ATLC) | $35.77 | $71.48 | 50% |

| Heartland Financial USA (NasdaqGS:HTLF) | $54.52 | $106.71 | 48.9% |

| Progress Software (NasdaqGS:PRGS) | $58.40 | $115.64 | 49.5% |

| BioMarin Pharmaceutical (NasdaqGS:BMRN) | $84.33 | $166.12 | 49.2% |

| Silicon Laboratories (NasdaqGS:SLAB) | $120.13 | $239.85 | 49.9% |

| Zynex (NasdaqGS:ZYXI) | $9.00 | $17.96 | 49.9% |

| Open Lending (NasdaqGM:LPRO) | $6.30 | $12.53 | 49.7% |

| Global-E Online (NasdaqGS:GLBE) | $34.32 | $67.94 | 49.5% |

| Clearwater Analytics Holdings (NYSE:CWAN) | $19.55 | $38.34 | 49% |

| SunOpta (NasdaqGS:STKL) | $5.30 | $10.60 | 50% |

We're going to check out a few of the best picks from our screener tool.

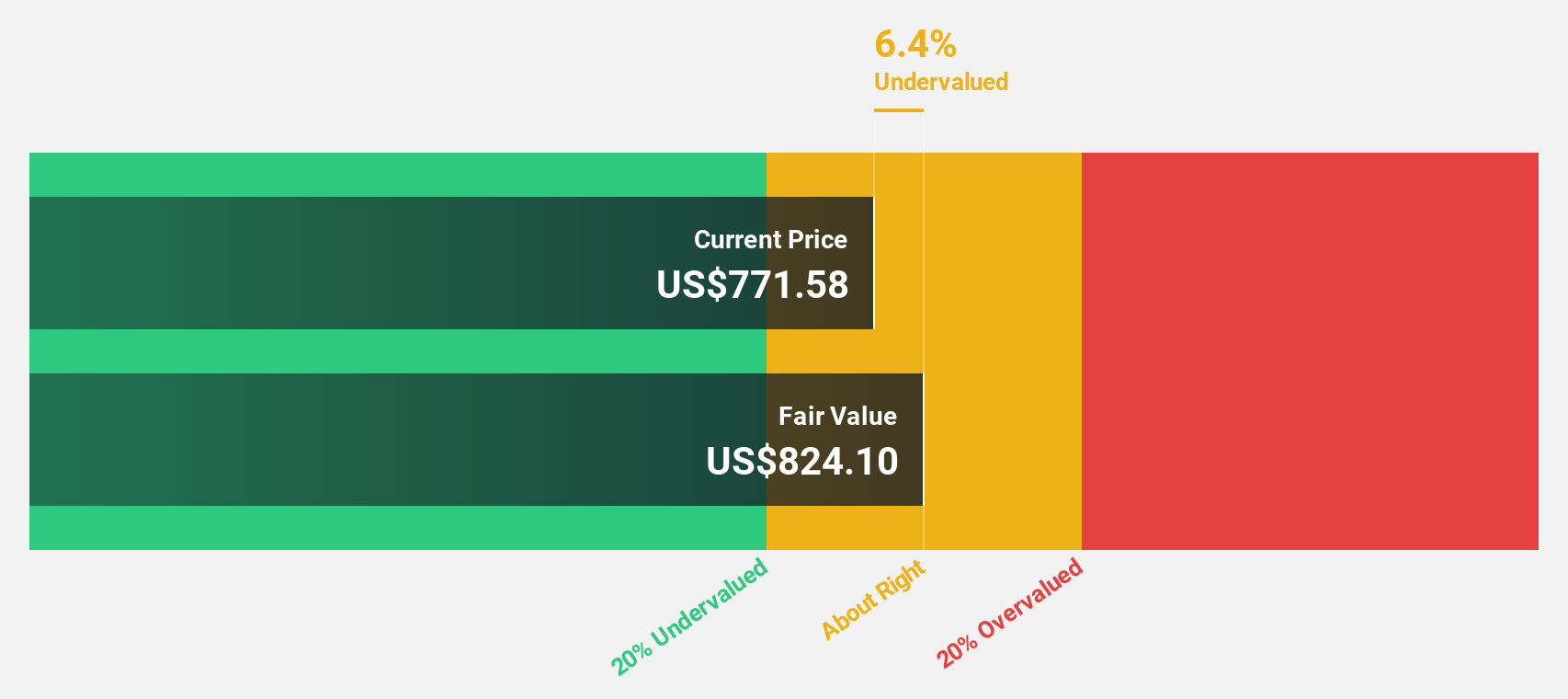

Adobe (NasdaqGS:ADBE)

Overview: Adobe Inc. operates as a diversified software company worldwide and has a market cap of approximately $244.60 billion.

Operations: Adobe's revenue segments consist of Digital Media ($15.03 billion), Digital Experience ($5.11 billion), and Publishing and Advertising ($284 million).

Estimated Discount To Fair Value: 25.3%

Adobe is trading at 25.3% below its estimated fair value of US$738.54, with a forecasted annual earnings growth of 17.2%, outpacing the US market average of 15%. Despite recent executive changes and a significant shelf registration filing for US$2.63 billion, Adobe’s robust cash flows and innovative AI-driven product enhancements in Acrobat and Lightroom position it as an undervalued stock based on discounted cash flow analysis.

- Upon reviewing our latest growth report, Adobe's projected financial performance appears quite optimistic.

- Take a closer look at Adobe's balance sheet health here in our report.

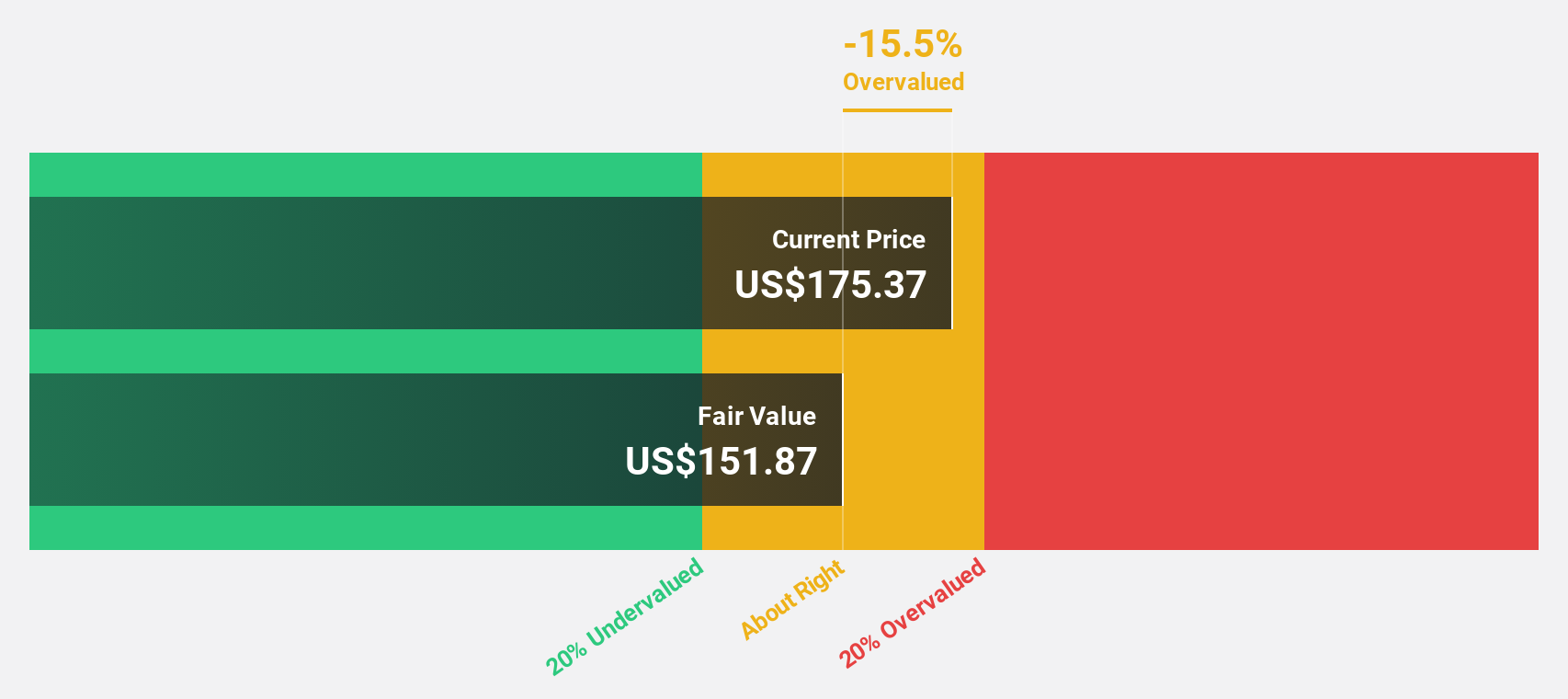

Intuit (NasdaqGS:INTU)

Overview: Intuit Inc. offers financial management and compliance solutions for consumers, small businesses, self-employed individuals, and accounting professionals across the United States, Canada, and internationally with a market cap of approximately $180.96 billion.

Operations: Intuit's revenue segments include Pro-Tax ($598 million), Consumer ($4.46 billion), Credit Karma ($1.65 billion), and Small Business and Self-Employed ($9.11 billion).

Estimated Discount To Fair Value: 40.4%

Intuit, trading at 40.4% below its estimated fair value of US$1086.97, demonstrates strong cash flow potential. Recent board appointments and AI-driven product innovations in Mailchimp enhance its strategic positioning. Despite forecasted revenue growth of 11.2% per year being slower than the ideal 20%, earnings are expected to grow at a robust 15.7% annually, outpacing the US market average of 15%. Intuit's high forecasted Return on Equity (26.2%) further underscores its undervaluation based on discounted cash flows analysis.

- Our earnings growth report unveils the potential for significant increases in Intuit's future results.

- Navigate through the intricacies of Intuit with our comprehensive financial health report here.

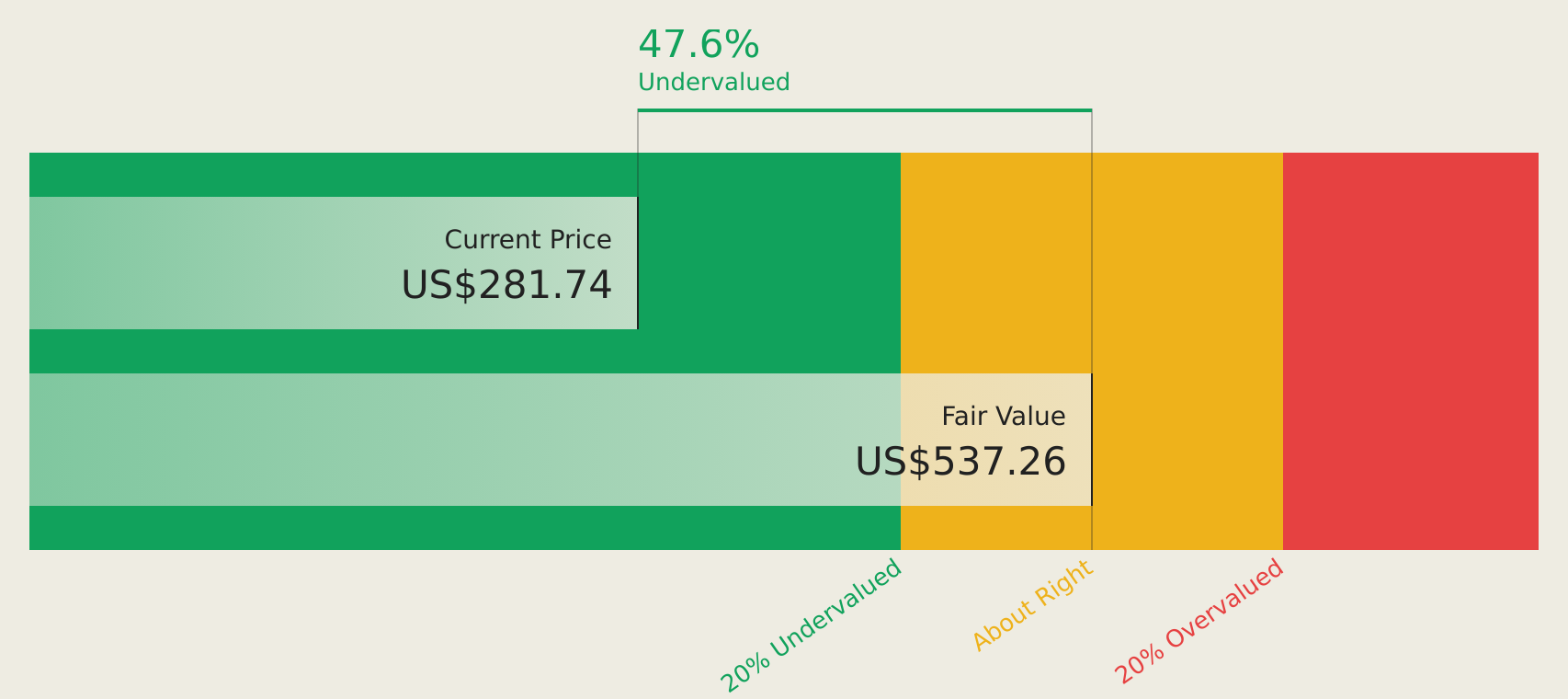

Howmet Aerospace (NYSE:HWM)

Overview: Howmet Aerospace Inc. offers advanced engineered solutions for the aerospace and transportation industries globally, with a market cap of approximately $39.06 billion.

Operations: The company's revenue segments include Forged Wheels at $1.13 billion, Engine Products at $3.48 billion, Fastening Systems at $1.49 billion, and Engineered Structures at $1.01 billion.

Estimated Discount To Fair Value: 46%

Howmet Aerospace, trading at US$95.7 and estimated to be worth US$177.35, is significantly undervalued based on discounted cash flows. Despite a high debt level and recent significant insider selling, its earnings grew 75.7% last year and are forecasted to grow 15.2% annually, outpacing the market average of 14.9%. Recent Q2 earnings showed strong performance with net income rising from US$193 million to US$266 million year-over-year.

- Our expertly prepared growth report on Howmet Aerospace implies its future financial outlook may be stronger than recent results.

- Click here to discover the nuances of Howmet Aerospace with our detailed financial health report.

Make It Happen

- Delve into our full catalog of 186 Undervalued US Stocks Based On Cash Flows here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Howmet Aerospace might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HWM

Howmet Aerospace

Provides advanced engineered solutions for the aerospace and transportation industries in the United States, Japan, France, Germany, the United Kingdom, Mexico, Italy, Canada, Poland, China, and internationally.

Outstanding track record with reasonable growth potential.