Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:SEDG

SolarEdge Technologies (SEDG) Valuation Check After Sharp One Year Rebound And Multi Year Weakness

SolarEdge Technologies stock overview after recent performance shift

SolarEdge Technologies (SEDG) has caught investors’ attention after a sharp 1 year total return of 155.48%, alongside a 3 year total return decline of 88.91% and 5 year total return decline of 88.32%.

Over shorter periods, the stock shows mixed performance, with a 1 day return of 2.62%, a 7 day decline of 4.14%, a month gain of 7.86%, and a past 3 months decline of 11.85%.

See our latest analysis for SolarEdge Technologies.

The recent 1 day share price return of 2.62% and 30 day share price return of 7.86% sit against a 1 year total shareholder return of 155.48%, alongside much weaker 3 and 5 year total shareholder returns. This suggests that short term momentum is rebuilding after a very difficult longer period.

If SolarEdge’s moves have you reassessing the solar and chip space, this could be a good moment to scan other high growth tech and AI stocks that are catching investors’ attention.

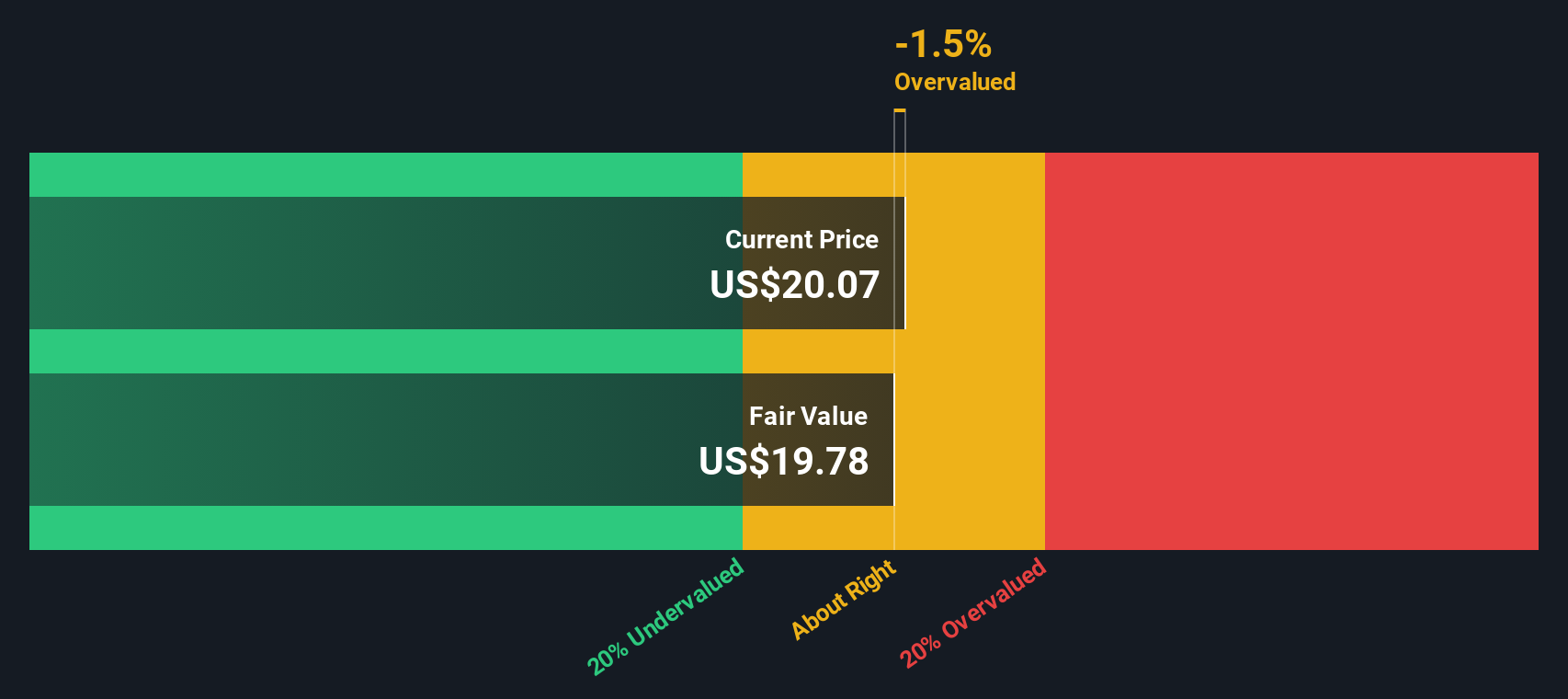

With the shares at $33.34, trading slightly above the current analyst price target and with an intrinsic value estimate that sits higher again, the key question is whether the recent rebound leaves upside on the table or whether the market is already pricing in a healthier future for SolarEdge.

Price-to-Sales of 1.9x: Is it justified?

On a P/S of 1.9x, SolarEdge screens cheaper than many semiconductor names, even after the sharp 1 year rebound in the share price.

The P/S ratio compares the company’s market value with its annual revenue, which can be useful for loss making businesses where earnings are not yet a helpful guide. For SolarEdge, current revenue of US$1,045.3m and a reported loss of US$560.8m mean investors are effectively paying under 2x sales for a business that is still in the red.

Relative to the US Semiconductor industry average P/S of 6.3x and a peer average of 2.9x, the stock trades at a clear discount. At the same time, the estimated fair P/S ratio is also 1.9x, which implies the current multiple sits right on the level the market could eventually gravitate toward if those fair value assumptions hold.

Explore the SWS fair ratio for SolarEdge Technologies

Result: Price-to-Sales of 1.9x (ABOUT RIGHT)

However, you still have to weigh the current US$560.8m loss, as well as any potential shifts in solar demand or policy, which could quickly challenge the recent share price recovery.

Find out about the key risks to this SolarEdge Technologies narrative.

Another view using our DCF model

If you look past the 1.9x P/S, our DCF model presents a different perspective. With SolarEdge at US$33.34 and our estimate of future cash flow value at US$22.32, the shares appear expensive on this measure. This raises the question of how much optimism is already reflected in the price.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out SolarEdge Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 881 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own SolarEdge Technologies Narrative

If you prefer to weigh the numbers yourself or reach a different conclusion, you can build a personalised SolarEdge view in just a few minutes with Do it your way.

A great starting point for your SolarEdge Technologies research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If SolarEdge has sparked your curiosity, do not stop here. Use this momentum to check other opportunities before the next move leaves you watching from the sidelines.

- Spot potential value in beaten down names by scanning these 3534 penny stocks with strong financials that still carry solid financial underpinnings.

- Lean into the growth story by filtering for these 23 AI penny stocks that are tied to artificial intelligence themes attracting strong attention.

- Strengthen your income play by reviewing these 13 dividend stocks with yields > 3% that could add more consistent yield to your portfolio mix.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SEDG

SolarEdge Technologies

Operates as an energy technology company in the United States, Europe, and internationally.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.167.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on Lagenda Properties Berhad ·

Lagenda Continues To Offer Earnings Visibility Backed By Strong Sales Pipeline

Fair Value:RM 2.0330.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on CAR Group ·

CAR Group. A wonderful compounding franchise at a fair-not-cheap price.

Fair Value:AU$3223.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative