- United States

- /

- Semiconductors

- /

- NasdaqGS:NXPI

Is NXP Semiconductors (NXPI) Building a Durable Edge in Autonomous Trucking Technology?

Reviewed by Simply Wall St

- Kodiak Robotics recently announced that it has integrated NXP Semiconductors’ automotive processors and network solutions to enhance the performance and reliability of its autonomous trucking platform, leveraging NXP’s S32G3 vehicle network processor, S32K3 microcontroller, VR5510 PMIC, and PF53 core supply regulator.

- This collaboration highlights growing adoption of NXP’s advanced automotive technologies in the emerging autonomous vehicle segment, emphasizing the company’s role in powering critical safety and real-time functions in next-generation commercial transportation systems.

- We’ll now assess how NXP’s involvement in powering Kodiak’s autonomous truck systems informs the company’s broader investment narrative and future outlook.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

NXP Semiconductors Investment Narrative Recap

To be a shareholder in NXP Semiconductors, the big picture centers on believing in sustained growth from automotive, industrial, and IoT chip demand, as well as the company’s ability to capture design wins in advanced driver-assistance and autonomous vehicle markets. The Kodiak Robotics integration demonstrates tangible traction in next-generation automotive, but the near-term revenue impact remains limited compared to the broader challenge of modest end-demand recovery and ongoing margin pressures, especially in China’s competitive environment.

Among recent announcements, NXP’s continued stream of interim dividends, like the board-approved US$1.014 per share set for Q3 2025, reinforces the company’s disciplined capital return approach. This reliability in shareholder returns is happening even as management works through acquisition integrations and as immediate growth in automotive and industrial end markets remains measured, highlighting NXP’s effort to balance payout stability with operational investments.

Yet, in contrast, investors should be aware of margin risks from rising competition in China and...

Read the full narrative on NXP Semiconductors (it's free!)

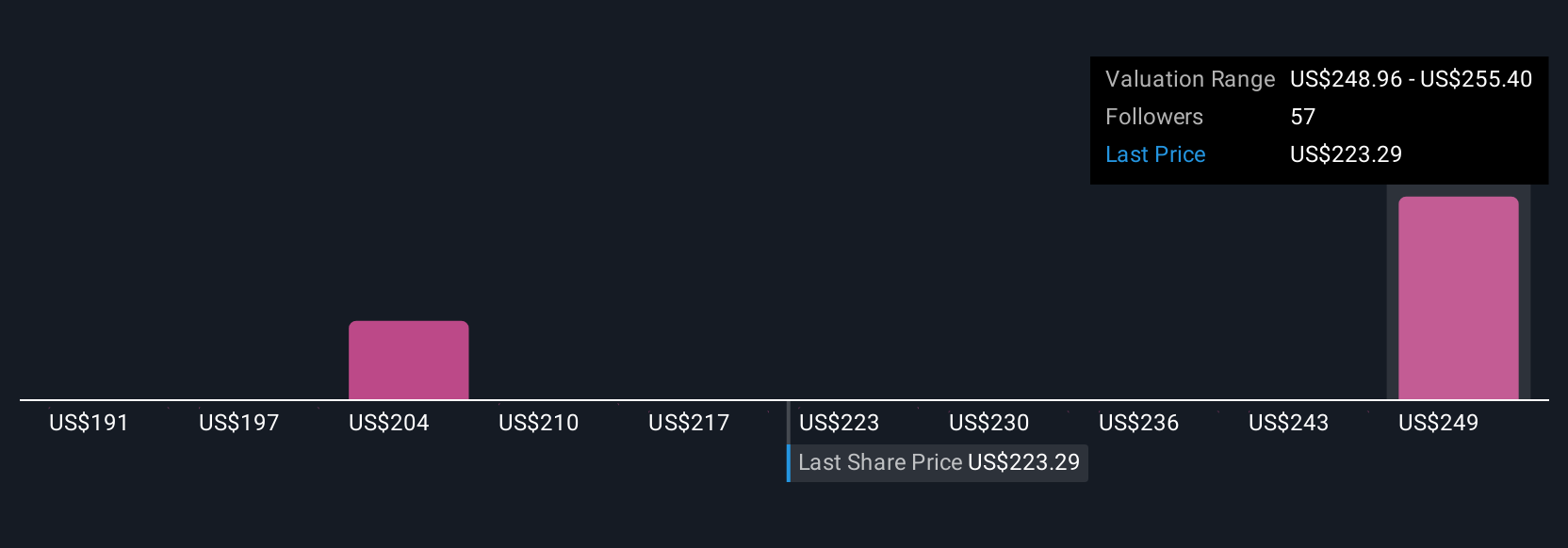

NXP Semiconductors is forecast to achieve $15.5 billion in revenue and $3.5 billion in earnings by 2028. This outlook is based on an expected annual revenue growth rate of 8.6% and a $1.4 billion increase in earnings from the current $2.1 billion.

Uncover how NXP Semiconductors' forecasts yield a $257.48 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Nine individual fair value estimates from the Simply Wall St Community span US$187.08 to US$257.48 per share, illustrating a broad spectrum of investor expectations. With competitive pressures from local OEMs in China posing a risk to NXP's margins, these differing perspectives remind you to explore a variety of outlooks before forming your own view.

Explore 9 other fair value estimates on NXP Semiconductors - why the stock might be worth as much as 8% more than the current price!

Build Your Own NXP Semiconductors Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your NXP Semiconductors research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free NXP Semiconductors research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NXP Semiconductors' overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- Find companies with promising cash flow potential yet trading below their fair value.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if NXP Semiconductors might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:NXPI

NXP Semiconductors

Provides semiconductor products in China, the United States, Germany, Japan, Singapore, South Korea, Mexico, the Netherlands, Taiwan, and internationally.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion