- United States

- /

- Semiconductors

- /

- NasdaqGS:NXPI

Does NXP Semiconductors (NASDAQ:NXPI) Have A Healthy Balance Sheet?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that NXP Semiconductors N.V. (NASDAQ:NXPI) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for NXP Semiconductors

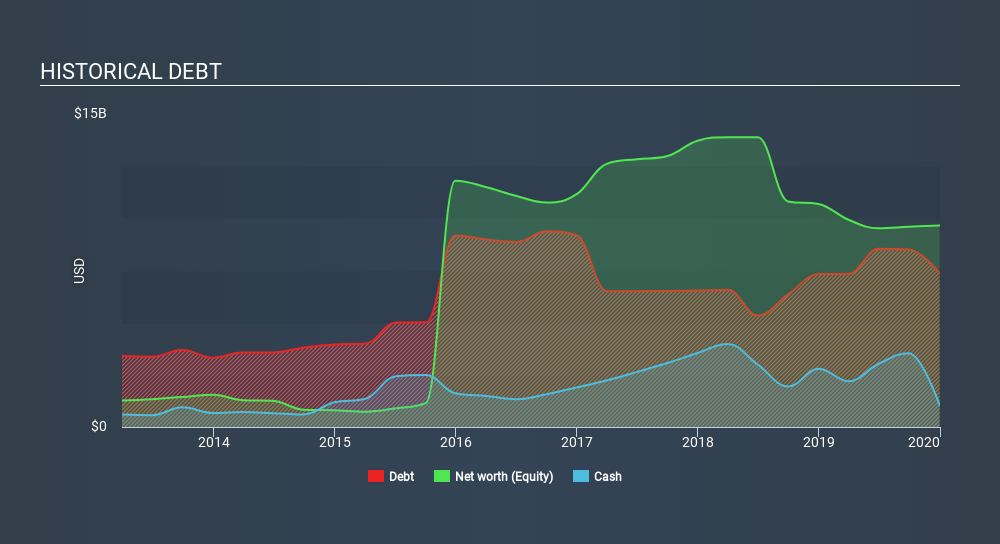

What Is NXP Semiconductors's Net Debt?

As you can see below, NXP Semiconductors had US$7.37b of debt, at December 2019, which is about the same as the year before. You can click the chart for greater detail. However, because it has a cash reserve of US$1.05b, its net debt is less, at about US$6.32b.

How Strong Is NXP Semiconductors's Balance Sheet?

We can see from the most recent balance sheet that NXP Semiconductors had liabilities of US$1.79b falling due within a year, and liabilities of US$8.57b due beyond that. Offsetting this, it had US$1.05b in cash and US$667.0m in receivables that were due within 12 months. So it has liabilities totalling US$8.65b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since NXP Semiconductors has a huge market capitalization of US$20.6b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While NXP Semiconductors has a quite reasonable net debt to EBITDA multiple of 2.3, its interest cover seems weak, at 2.1. The main reason for this is that it has such high depreciation and amortisation. While companies often boast that these charges are non-cash, most such businesses will therefore require ongoing investment (that is not expensed.) In any case, it's safe to say the company has meaningful debt. Unfortunately, NXP Semiconductors saw its EBIT slide 7.6% in the last twelve months. If that earnings trend continues then its debt load will grow heavy like the heart of a polar bear watching its sole cub. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if NXP Semiconductors can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, NXP Semiconductors actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Neither NXP Semiconductors's ability to cover its interest expense with its EBIT nor its EBIT growth rate gave us confidence in its ability to take on more debt. But the good news is it seems to be able to convert EBIT to free cash flow with ease. We think that NXP Semiconductors's debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Be aware that NXP Semiconductors is showing 3 warning signs in our investment analysis , and 1 of those is a bit unpleasant...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:NXPI

NXP Semiconductors

Offers various semiconductor products in China, the United States, Germany, Japan, Singapore, South Korea, Mexico, the Netherlands, Taiwan, and internationally.

Undervalued with mediocre balance sheet.

Similar Companies

Market Insights

Community Narratives