- United States

- /

- Semiconductors

- /

- NasdaqGS:CRUS

Cirrus Logic (CRUS) Profit Margins Expand, Reinforcing Bullish Narrative on Earnings Quality

Reviewed by Simply Wall St

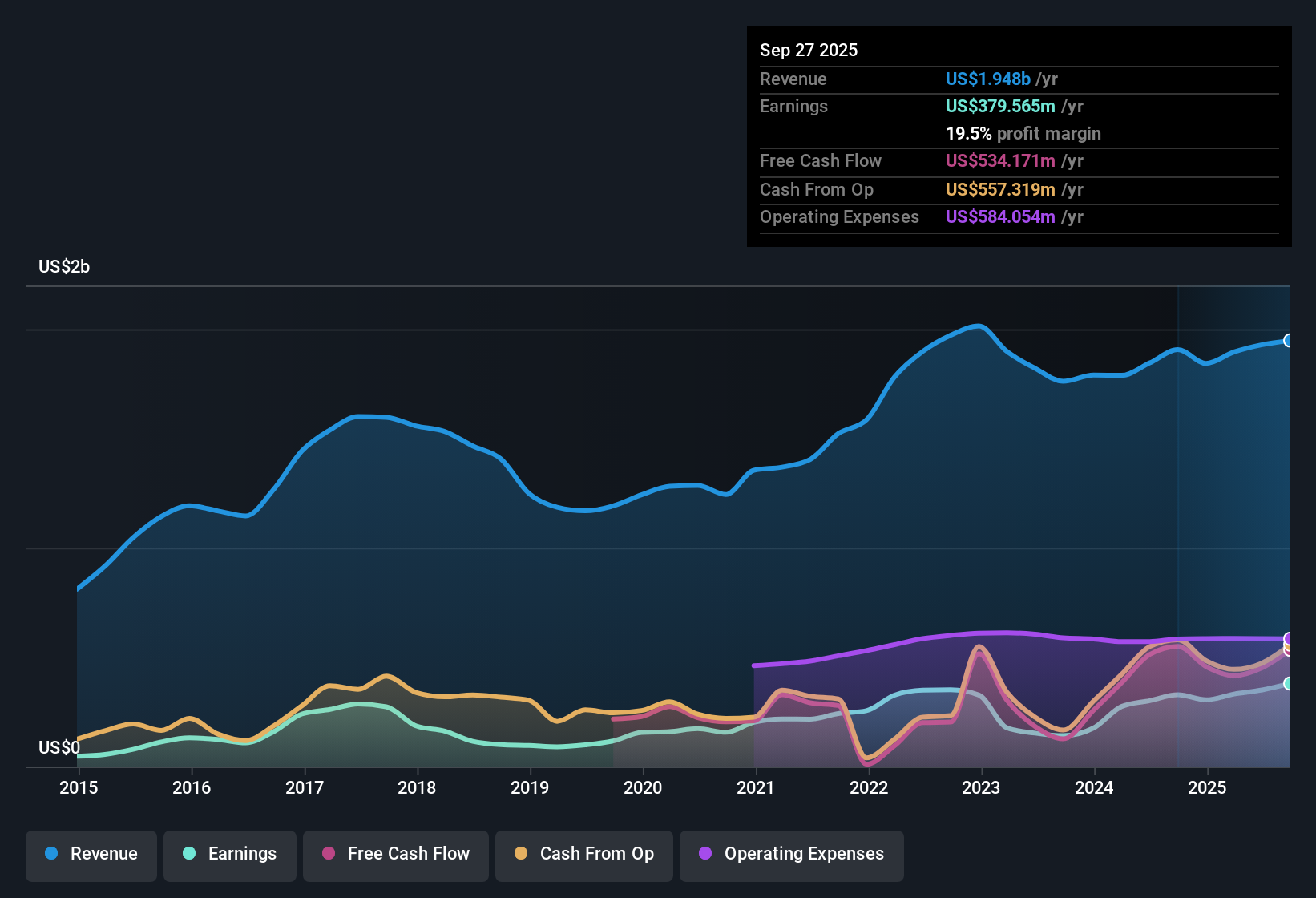

Cirrus Logic (CRUS) reported net profit margins of 18.1%, up from 16.3% a year ago, highlighting further expansion in profitability. Earnings grew 16.4% from the previous year, well above the company's five-year average annual growth rate of 7.7%. With margins on the rise and profit momentum solid, investors are likely viewing these results as a sign of high-quality earnings, even as future earnings and revenue growth are expected to slow compared to broader US market averages.

See our full analysis for Cirrus Logic.Next, we will see how these headline figures compare to some of the most commonly discussed narratives among Cirrus Logic investors. Some might be confirmed, and others called into question.

See what the community is saying about Cirrus Logic

Analyst Price Target Sits Above Today's Share Price

- At a share price of $119.42, Cirrus Logic trades around 12% below the one permitted analyst price target of $135.83. This suggests the market remains somewhat skeptical relative to average analyst expectations, despite recent profit growth.

- Analysts' consensus view notes that, although future earnings are projected to shrink to $295.7 million by 2028 (from $350.1 million today), the price target reflects a scenario where Cirrus Logic would trade at a 25.1x PE, which is lower than many semiconductor peers. It also assumes that long-term diversification into laptops, automotive, and IoT will offset slowdowns in the core smartphone segment.

- Consensus narrative highlights that, even with a forecast earnings decline and margin compression from 18.1% to 15.2%, Cirrus Logic's multi-market strategy and maintained profitability position it as relatively resilient in a cyclical sector.

- Despite expected slow growth, a positive valuation gap persists because industry comparables like the US semiconductor sector average much higher price-to-earnings multiples. This supports an argument that Cirrus could rerate if diversification pays off.

Relative Value Appeal Despite Slower Growth Forecasts

- Cirrus Logic's price-to-earnings ratio of 17.4x is below both the US semiconductor sector (35.8x) and peer average (35.9x), providing a notable discount even as the company’s own expected annual earnings growth of 3.2% lags market benchmarks.

- According to analysts' consensus view, this valuation gap substantially supports the investment case, since:

- The share’s discount to industry multiples makes Cirrus attractive for value-focused investors, especially given steady historical margin improvement and consistent profit expansion.

- General value considerations dominate current risk/reward assessments with zero new risk factors flagged, and rewards encompassing both relative value and evidence of robust underlying business strength.

Margins Projected to Tighten as Diversification Efforts Ramp

- Consensus narrative points to forecasts that net profit margin will decline from 18.1% now to just 15.2% over three years, as the mix broadens beyond legacy smartphone audio into early-stage markets like automotive and IoT.

- Analysts' consensus view emphasizes the tension in Cirrus Logic’s diversification push:

- While expansion into new sectors could stabilize long-term revenue, near-term risk remains high given that automotive and PC components add only marginal revenue now and scale-up is uncertain.

- Bears highlight that continued reliance on a few smartphone customers, together with early-stage bets in diversification, could amplify volatility in both earnings and margins if those segments do not achieve material revenue share soon.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Cirrus Logic on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have your own take on the numbers? Share your unique angle and add your voice to the discussion in just a few minutes. Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Cirrus Logic.

See What Else Is Out There

Cirrus Logic faces earnings and margin pressure as diversification efforts introduce near-term volatility and growth falls short of sector averages.

If you want steadier performance, focus your search with stable growth stocks screener (2073 results), where you’ll find companies delivering consistent revenue and profit expansion without sector-specific swings.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CRUS

Cirrus Logic

A fabless semiconductor company, develops mixed-signal processing solutions and audio products in China, the United States, and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion