Wayfair (W) shares have moved only slightly today, with no major news or corporate events sparking the latest price action. The stock’s performance remains largely driven by recent trends and broader market sentiment.

Wayfair’s recent 9.8% seven-day share price return and 26.6% gain over the last month show renewed momentum building behind the stock. This comes against a backdrop of a remarkable 132% total shareholder return over the past year. While multi-year returns remain mixed, recent performance has reignited investor interest and hints at shifting sentiment around the company's growth prospects.

The key question now for investors is whether Wayfair’s strong run has left it undervalued with more room to grow, or if the market has already priced in the company’s improving outlook and future gains.

Advertisement

Most Popular Narrative: 7.7% Undervalued

With Wayfair closing at $105.20 and the narrative's fair value set at $114, analysts still see upside potential above the recent price action. The gap between the current price and the narrative's estimate signals lingering optimism in the mid-term outlook.

Wayfair's proprietary logistics network, CastleGate, is expected to provide a meaningful growth unlock by improving efficiency and customer experience, which can positively impact revenue growth through higher conversion rates and potentially improved net margins.

Want to see which financial levers are fueling this bullish stance? The story banks on a dramatic turnaround in future profitability and aggressive operating improvements. Get the scoop on the ambitious targets packed inside this fair value formula. These are assumptions you will want to dig into before investors catch on.

However, macroeconomic headwinds such as persistent inflation or ongoing challenges in the housing market could quickly dampen momentum around Wayfair’s improving outlook.

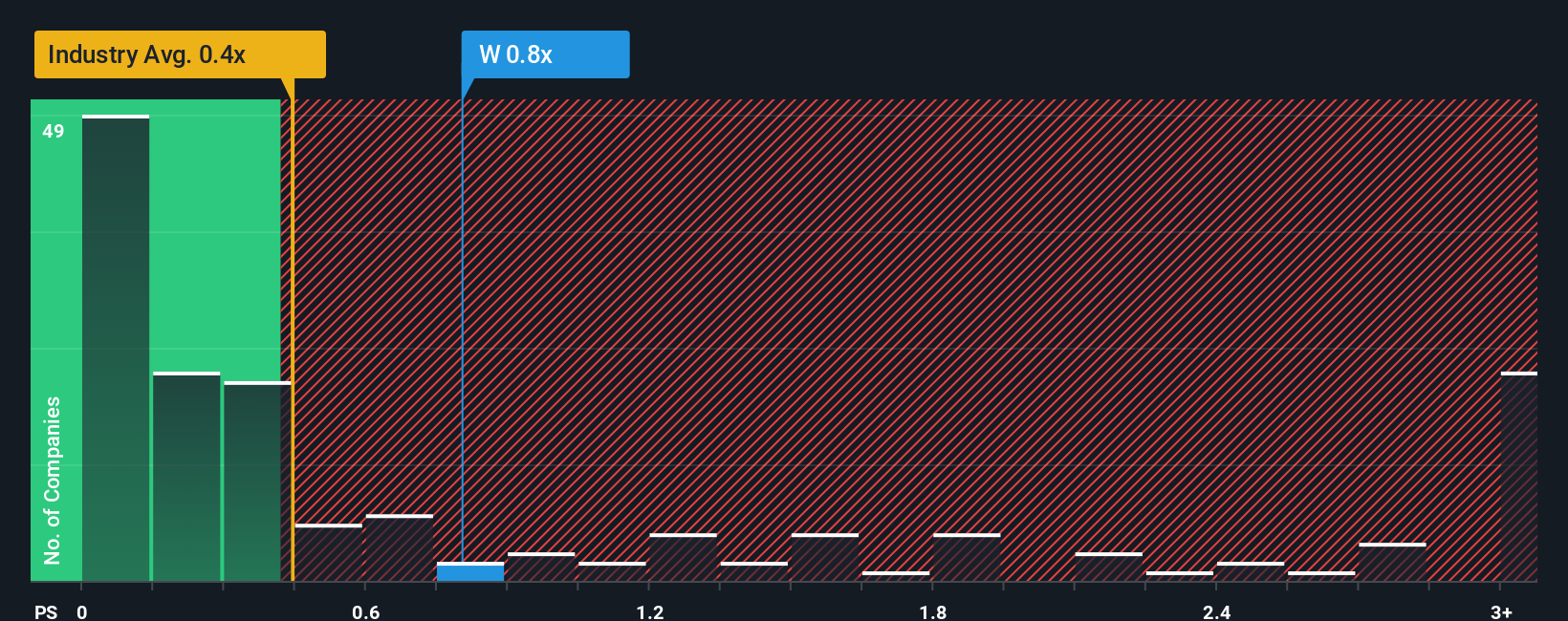

While the fair value estimate suggests Wayfair could be undervalued, a look at its price-to-sales ratio tells a different story. At 1.1x, Wayfair is considerably more expensive than both the US Specialty Retail industry average (0.5x) and its own fair ratio of 0.7x. This suggests investors are paying a premium for future growth hopes. How sustainable is that optimism if results fall short?

If you see the story differently or want to dig deeper into the numbers, you can easily craft your own perspective in just a few minutes with Do it your way.

Smart investing means always having fresh opportunities on your radar. Stay ahead by tracking unique stocks and sectors that could make a major impact on your portfolio.

Capitalize on tech breakthroughs by reviewing these 26 AI penny stocks, which are shaking up the world with artificial intelligence advancements and strong growth prospects.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wayfair might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.