Advertisement

- United States

- /

- Food and Staples Retail

- /

- NYSE:TGT

Target’s (NYSE:TGT) Capital Allocation is Working in the Company's Favor Despite Current Margin Pressure

The market’s knee jerk reaction to Target's (NYSE:TGT) third quarter results was to sell the stock due to declining margins. If we look beyond margin pressure - which may be temporary - the company has some strong underlying trends in place.

Third quarter financial highlights:

- Revenue of $25.6 billion up 13% YoY and $1.09 billion ahead of consensus estimate

- GAAP EPS of $3.04 up 51.6% and $0.27 ahead of consensus estimate

- Comparable sales up 12.7%.

- Store comparable sales up 9.7%.

- Digital comparable sales up 29%.

- Fourth quarter guidance for comparable sales: high-single digit to low-double digit growth.

These were strong results but the market reacted negatively to a decline in the gross which fell from 30.6% to 28%. The company has indicated that it intends to ‘hold the line’ on prices, rather than raising the prices it charges consumers. This should be a temporary headwind as the company will no doubt be forced to raise prices if inflation persists.

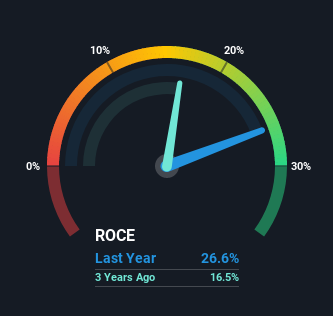

If these headwinds are indeed temporary, price weakness may provide an opportunity for investors. We decided to have a look at Target’s returns on capital employed (ROCE) to get an idea of the company’s long term profitability. Ideally we like to see companies with an ROCE that are increasing, in conjunction with a growing amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities.

Return On Capital Employed (ROCE): What is it?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Target is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.27 = US$8.5b ÷ (US$51b - US$19b) (Based on the trailing twelve months to July 2021).

So, Target has an ROCE of 27%. That's a fantastic return and not only that, it outpaces the average of 13% earned by companies in a similar industry.

View our latest analysis for Target

In the above chart we have measured Target's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Target here for free.

What Can We Tell From Target's ROCE Trend?

Investors should be pleased with what's happening at Target. The data shows that returns on capital have increased substantially over the last five years to 27%. The amount of capital employed has increased too, by 22%. So we're very much inspired by what we're seeing at Target thanks to its ability to profitably reinvest capital.

What We Can Learn From Target's ROCE

To sum it up, Target has proven it can reinvest in the business and generate higher returns on that capital employed, which is terrific. And with the stock having performed exceptionally well over the last five years, these patterns are being accounted for by investors. Therefore, we think it would be worth your time to check if these trends are going to continue.

Target’s ROCE trend suggests a strong business model, but this is just one aspect of the business. If you would like to know more about the company, take a look at our analysis of Target. In particular you may want to keep an eye on the valuation and forecast growth rates to assess the current opportunity.

If you'd like to see other companies earning high returns, check out our free list of companies earning high returns with solid balance sheets here.

Valuation is complex, but we're here to simplify it.

Discover if Target might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.

About NYSE:TGT

6 star dividend payer and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4034.1% undervalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6090.0% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

17 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8142.8% undervalued

34 followersusers have followed this narrative

3 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

CW

Cwburton on Verano Holdings ·

Waiting for the Inevitable

Fair Value:CA$5.5278.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.11k18.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LE

lexdrew1 on Corning ·

Corning's Revenue Will Climb by 12.73% in Just Five Years

Fair Value:US$108.6313.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

119 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.6% undervalued

963 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8688.6% undervalued

76 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative