Advertisement

Lowe's Companies, Inc. (NYSE:LOW) gained a good 44% in the span of one year. The last earnings report netted Lowe's some US$6.9b in trailing twelve month net income, representing a 22.6% annual earnings growth. Analysts are also estimating both revenue and profit growth in the future. However, the company seems to carry some risks, and we will examine it in our article today.

Lowe's strategy involves serving both consumer and professional clients in the home improvement industry. The company is pushing an omnichannel approach and is strengthening their connection to professionals that offer home improvement services, as well as their online presence. The company estimates to be in a US$900b and growing industry, which would put their revenues around a 10.5% market share.

Lowe's most prominent competitors for market share, are small, micro and service based companies, along with the giant Amazon (NASDAQ:AMZN).

As far as competition is concerned, Lowe's is doing their best to differentiate itself from the products that Amazon offers consumers and professionals. Considering that they have managed to stay afloat after Amazon drove many retailers out of business, it seems likely that there is a combination of product and service linking that drives value for Lowe's.

Before we look at the fundamental risks from debt, we should note that while the company's new strategy seems to be working in increasing sales, it also stands to reason that Lowe's benefited from a cyclical wave of home improvement enthusiasm that began in 2020. Further, this enthusiasm is sustained by the rising real-estate prices, which motivate sellers to fix-up the homes that they wish to sell, while at the same time detracting buyers from looking at new homes and reorienting them to fix what they currently have. Additionally, the price of raw materials, such as wood, may have also contributed to the final revenue number, which is not a result of growth, but of inflation.

Debt Analysis

An important factor for the risk in Lowe's is their debt burden. We will look at both short-term and long-term obligations, to see if Lowe's might have liquidity issues down the line.

Check out our latest analysis for Lowe's Companies

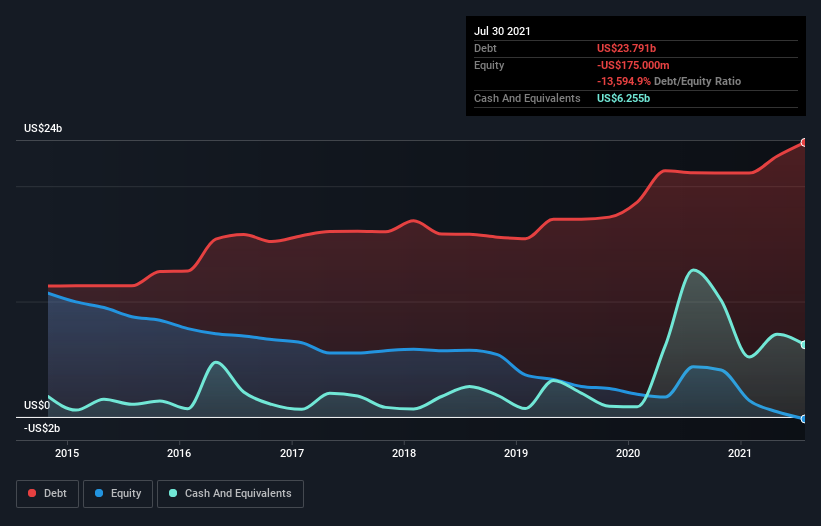

You can click the graphic below for the historical numbers, but it shows that as of July 2021 Lowe's Companies had US$23.8b of debt, an increase on US$21.2b, over one year.

On the flip side, it has US$6.26b in cash, leading to net debt of about US$17.5b. This number is large on the face value, but can be covered in a few years as the company's Earnings Before Interest and Tax are at US$11.5b.

How Healthy Is Lowe's Companies' Balance Sheet?

According to the last reported balance sheet, Lowe's Companies had liabilities of US$21.7b due within 12 months, and liabilities of US$27.9b due beyond 12 months. Offsetting these obligations, it had cash of US$6.26b as well as receivables valued at US$368.0m due within 12 months.

On a fundamental basis, its liabilities total US$43.0b more than the combination of its cash and short-term receivables.

This deficit isn't so bad because Lowe's Companies is worth a massive US$160.5b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose.

When looking at the company's ability to service long-term debt, we use two main ratios to inform us about debt levels relative to earnings.

The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Lowe's Companies's net debt is only 1.2 times its EBITDA.

EBIT covers its interest expense a 14.6 times over.

On top of that, Lowe's Companies grew its EBIT by 42% over the last twelve months, and that growth will make it easier to handle its debt.

If we count retail stores and other operating lease obligations as debt, we might want to add some US$3.8b to the debt balance, which should not be overlooked when analyzing the burden of a company

Key Takeaways

Lowe's has a total of short and long-term obligations (including operating leases) at around US$53b. While it is true that their financial performance also increased and EBIT is up by 42%, this might be due partly to a cycling of the economy, rather than the performance of the business. The debt, however, tends to stay on longer and will contribute to the increased risk of the company as it represents an additional fixed cost.

Companies use debt to move funds from the future to the present, while expensing the interest on debt. Another use, is for capital investments, and finally they get more debt when they need it.

Lowe is currently stable and can easily service their debt, however we might want to see the performance of the company beyond extraordinary circumstances, in order to get a better picture.

There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 2 warning signs for Lowe's Companies (1 can't be ignored!) that you should be aware of before investing here.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NYSE:LOW

Lowe's Companies

Operates as a home improvement retailer in the United States.

Established dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor