Lowe's Companies (LOW) has seen a modest slip in its stock price over the past month, with shares drifting about 4% lower. Despite this dip, the retailer's long-term performance remains in focus for investors looking to assess value.

Lowe's share price has ebbed slightly after its earlier momentum this year, reflecting a more cautious tone in the market. However, when viewed over a longer period, total shareholder returns over three and five years have remained solid. This suggests investors continue to see value in its steady growth and reliable dividends.

The real question now is whether Lowe’s current dip signals an attractive entry point, or if the stock’s price already reflects expectations for its future growth. Is there value left for new investors, or is everything already priced in?

Advertisement

Most Popular Narrative: 12.2% Undervalued

Lowe’s valuation narrative places its fair value noticeably above the most recent close. Market watchers will want to dig deeper into the strategic assumptions underpinning this target before deciding what comes next.

Ongoing pent-up demand from delayed home improvement projects, combined with record-high aging U.S. housing stock and an estimated 18 million new homes needed by 2033, points to a significant runway for future growth in renovation, repair, and new construction. This will positively affect revenue and support sustained top-line expansion as the housing cycle recovers.

Curious what exactly justifies such a bullish fair value? The narrative’s ambitious outlook hinges on some eye-opening growth forecasts and robust profitability assumptions, but the projected margin lift alone might surprise you. Which bold assumptions move the needle most? Read on to find out.

However, risks remain, including potential integration issues from recent acquisitions as well as pressure on margins from ongoing labor shortages and rising operational costs.

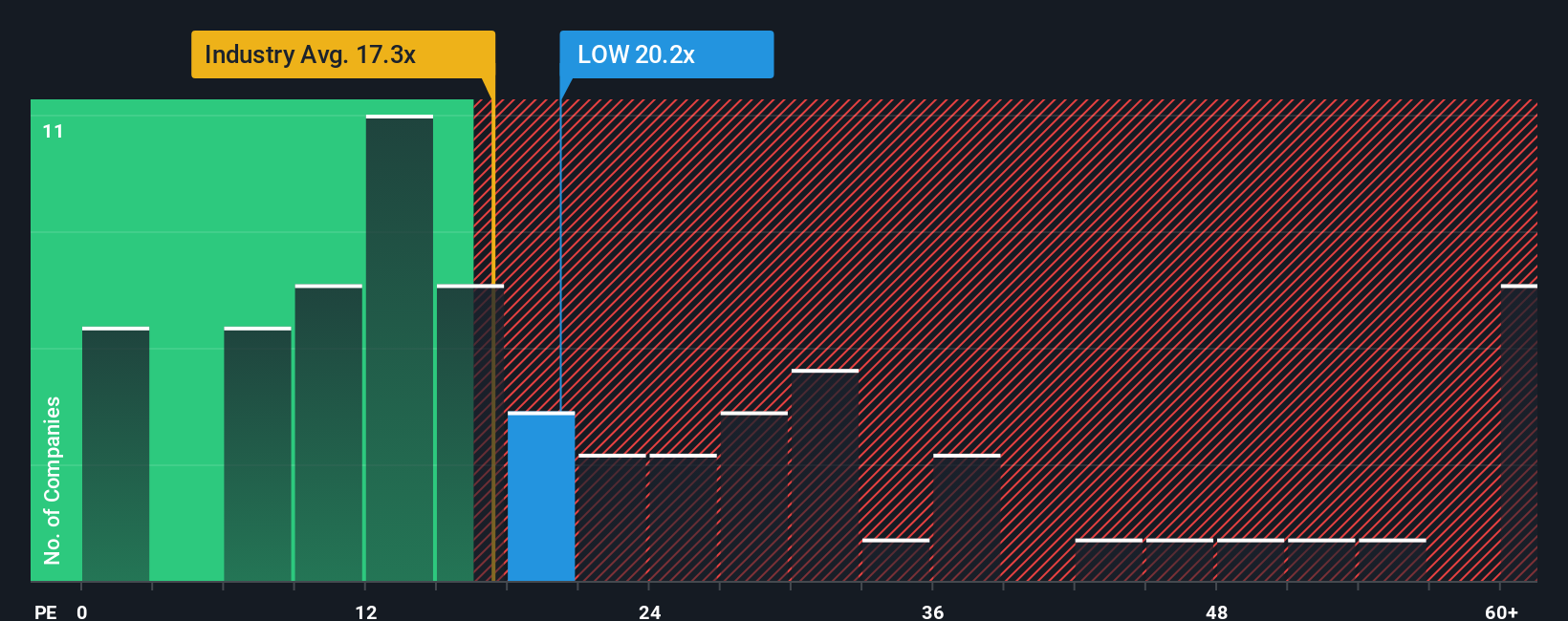

Another Perspective: Multiples Paint a Different Picture

While the fair value narrative suggests Lowe’s shares are undervalued, a look at its current price-to-earnings ratio of 20.3x tells a more nuanced story. This ratio is above the industry average of 17.2x, but still beneath the peer group’s 48.3x benchmark and close to the fair ratio of 21.1x. This could mean Lowe’s is not as much of a bargain as it first appears, or perhaps the market is missing something. Where should investors look next?

If these narratives do not align with your outlook, or you would prefer to analyze the numbers yourself, it is quick and easy to craft your own viewpoint in just minutes. Do it your way

A great starting point for your Lowe's Companies research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Ready for More Winning Ideas?

You owe it to yourself to jump on fresh investment opportunities that others might overlook. Don't wait. Put your money to work with smarter picks now!

Capture future market leaders by tapping into these 24 AI penny stocks as they transform entire industries with artificial intelligence innovation.

Position yourself at the forefront of financial breakthroughs when you check out these 78 cryptocurrency and blockchain stocks disrupting traditional finance with blockchain and cryptocurrency solutions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies