- United States

- /

- Specialty Stores

- /

- NYSE:HD

3 Points to Check Before Buying The Home Depot, Inc. (NYSE:HD) For Its Dividend

In the face of inflation concerns, it is not surprising that real estate gets so much attention. Being the dominant presence in the home improvement sector, The Home Depot, Inc. (NYSE: HD) is certainly benefiting from those trends.

With the latest earnings reported and the ex-dividend date announced, we will examine its dividend trends over the last decade.

The Home Depot is a Georgia-based retailer focusing on home improvement and maintenance. It operates 2,298 stores across North America, focusing on the 2 key market segments: professionals and Do-it-yourself (DIY) customers.

The company reported a solid second-quarter result with improved earnings and revenues, although profit margins were flat.

Second quarter 2021 results:

- Revenue: US$41.1b (up 8.1% y/y).

- Net income: US$4.81b (up 11% y/y).

- Profit margin: 12% (in line).

- GAAP EPS: US$4.53 (beat by US$0.11)

Over the last 3 years on average, earnings per share have increased by 15% per year, whereas the company’s share price has increased by 18% per year.

However, comparable sales missed, delivering +4.5% vs. Consensus +5.61%, and gross margin fell 80bps to 33.2%.

The stock slumped on the results, with analysts quoting comparable sales miss and concerns for profit margins. Yet, Wells Fargo keeps a buy rating, quoting commodity prices and Delta variant risks to see heightened demand for home improvement.

Not to mention the incoming hurricane season.

Dividend Outlook

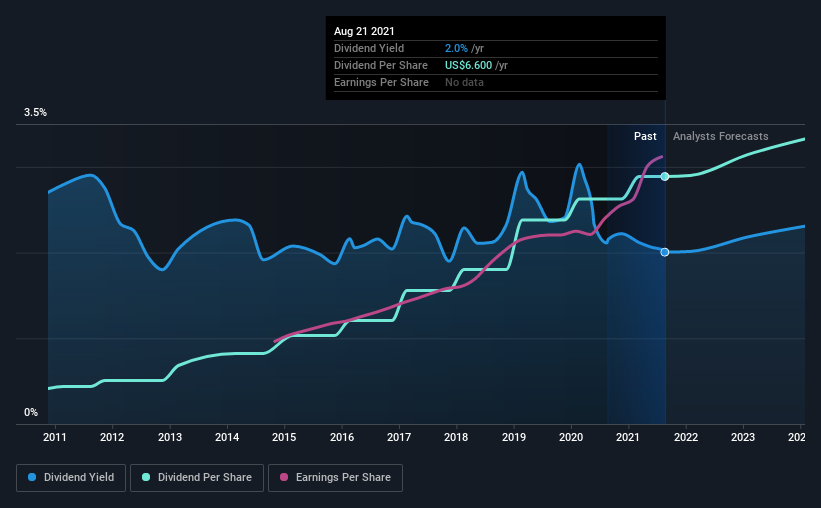

A 2.0% yield is not terribly exciting, but the long payment history suggests Home Depot has some staying power.

The company also returned around 1.9% of its market capitalization to shareholders in stock buybacks over the past year.

Explore this interactive chart for our latest analysis on Home Depot!

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable.

Home Depot paid out 44% of its profit as dividends over the trailing twelve-month period. A medium payout ratio strikes a good balance between paying dividends and keeping enough back to invest in the business. Besides, if reinvestment opportunities dry up, the company has room to increase the dividend.

Another important check is to see if the free cash flow generated is sufficient to pay the dividend. The company paid out 59% of its free cash flow, which is not bad per se but does start to limit the amount of cash Home Depot has available to meet other needs.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

You can check our latest analysis on Home Depot's financial position here.

Volatility and Growth Potential

The dividend has been stable over the past 10 years, which is great. We think this could suggest some resilience to the business and its dividends. During the past 10-year period, the first annual payment was US$0.9 in 2011, compared to US$6.6 last year. Dividends per share have grown at approximately 21% per year over this time.

Dividends have been growing pretty quickly, and even more impressively, they haven't experienced any notable falls during this period.

While dividend payments have been relatively reliable, it would also be nice if earnings per share (EPS) grew, as this is essential to maintaining the dividend's purchasing power over the long term. Strong earnings per share (EPS) growth might encourage our interest in the company despite fluctuating dividends, which is why it's great to see Home Depot has grown its earnings per share at 19% per annum over the past five years.

A company paying out less than a quarter of its earnings as dividends, and growing earnings at more than 10% per annum, looks to be right on the cusp of its growth phase. At the right price, it is an interesting opportunity.

Conclusion

The Holy Trinity of a good dividend opportunity is affordability, stability, and growth prospects.

Home Depot's dividend payout ratios are within normal bounds, although we note its cash flow is not as strong as the income statement would suggest.

That said, we were glad to see it growing earnings and paying a fairly consistent dividend. Overall we think Home Depot scores well on our analysis. It's not quite perfect, but we'd definitely be keen to take a closer look.

Investors generally tend to favor companies with a consistent, stable dividend policy instead of those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analyzing a company. For example, we've picked out 1 warning sign for Home Depot that investors should know about before committing capital to this stock.

We have also put together a list of global stocks with a market capitalization above $1bn and yielding more 3%.

If you're looking to trade Home Depot, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Home Depot might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Stjepan Kalinic

Stjepan is a writer and an analyst covering equity markets. As a former multi-asset analyst, he prefers to look beyond the surface and uncover ideas that might not be on retail investors' radar. You can find his research all over the internet, including Simply Wall St News, Yahoo Finance, Benzinga, Vincent, and Barron's.

About NYSE:HD

Home Depot

Operates as a home improvement retailer in the United States and internationally.

Established dividend payer with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives