Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:BURL

Burlington Stores (BURL) Is Up 12.1% After Strong Q3, Raised Outlook and Buybacks - What's Changed

Simply Wall St

Reviewed by Sasha Jovanovic

- In the past week, Burlington Stores reported higher third-quarter revenue of US$2,710.44 million and net income of US$104.75 million, raised full-year sales guidance, continued share repurchases totaling US$429.21 million across two programs, and reaffirmed plans to open 104 net new stores by fiscal year-end 2025.

- This combination of stronger earnings, ongoing buybacks, and an aggressive store-opening plan underscores management’s confidence in Burlington’s off-price model and its capacity-led growth strategy.

- We’ll now examine how these stronger third-quarter results and upgraded full-year sales outlook may influence Burlington’s existing multi-year margin expansion and store growth narrative.

These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Burlington Stores Investment Narrative Recap

To own Burlington Stores, you need to believe its off price model can keep converting steady traffic into higher margins while a large new store pipeline scales efficiently. The latest third quarter beat and raised full year sales guidance support that near term earnings momentum is intact, while the most immediate risk remains that a softer value focused consumer or over aggressive expansion could magnify fixed costs and pressure profitability; the new data does not remove that risk.

The most relevant update here is Burlington’s plan to open 104 net new stores by fiscal year end 2025, which ties directly into its capacity led growth story. This expansion program is central to the current catalyst of capturing more value seeking shoppers, but it also amplifies the risk that a slower economy or weaker in store traffic could leave the company with higher operating leverage and more volatile earnings.

But investors should also be aware that if store growth outpaces sustainable demand, then...

Read the full narrative on Burlington Stores (it's free!)

Burlington Stores' narrative projects $14.3 billion revenue and $993.7 million earnings by 2028.

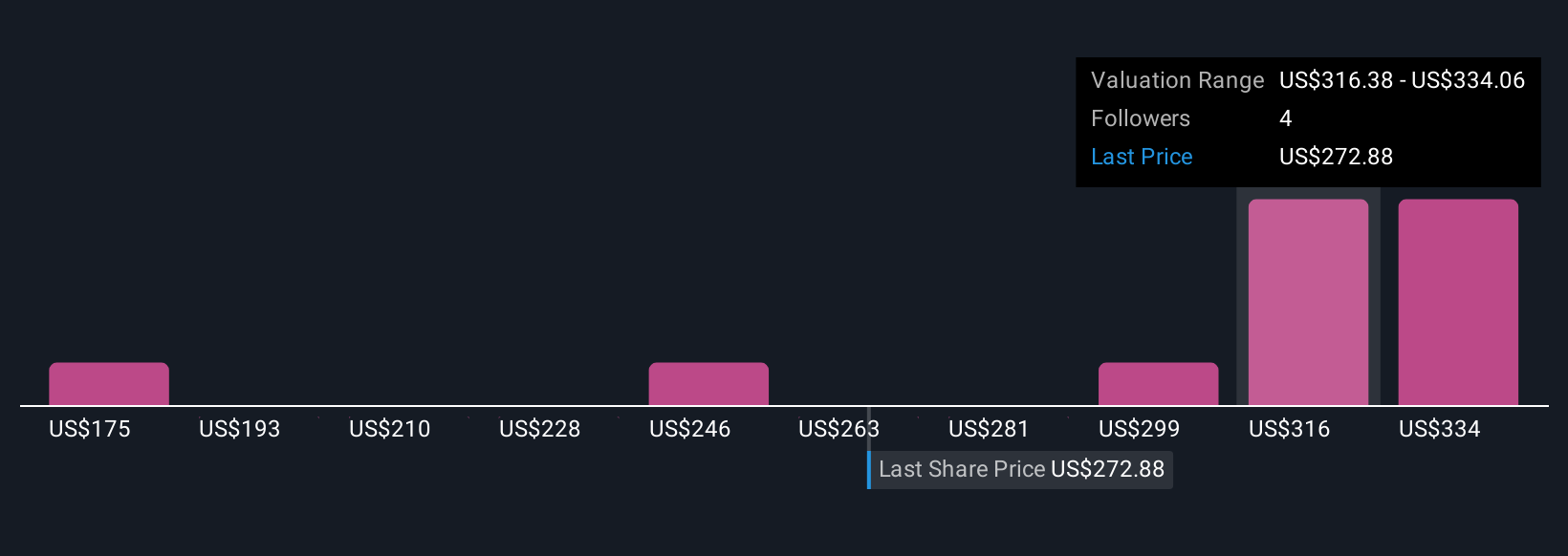

Uncover how Burlington Stores' forecasts yield a $336.20 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Five Simply Wall St Community fair value estimates for Burlington range from US$174.88 to US$377.53, showing how differently individual investors view its prospects. When you set these against Burlington’s large planned store rollout, it becomes clear that opinions on how expansion will affect future performance can vary widely, so it is worth exploring several viewpoints before making up your mind.

Explore 5 other fair value estimates on Burlington Stores - why the stock might be worth 36% less than the current price!

Build Your Own Burlington Stores Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Burlington Stores research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Burlington Stores research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Burlington Stores' overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 37 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Burlington Stores might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BURL

Burlington Stores

Operates as a retailer of branded merchandise in the United States and Puerto Rico.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

65 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Magma Silver ·

Silver's Breakout to over $50US will make Magma’s future shine with drill sampling returning 115g/t Silver and 2.3 g/t Gold at its Peru Mine

Fair Value:CA$0.3534.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on SEGRO ·

SEGRO's Revenue to Rise 14.7% Amidst Optimistic Growth Plans

Fair Value:UK£9.3924.7% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PI

PicaCoder on Microsoft ·

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value:US$42015.0% overvalued

62 followersusers have followed this narrative

12 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

958 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

65 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative