Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:BNED

Barnes & Noble Education (NYSE:BNED) Has A Somewhat Strained Balance Sheet

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Barnes & Noble Education, Inc. (NYSE:BNED) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Barnes & Noble Education

How Much Debt Does Barnes & Noble Education Carry?

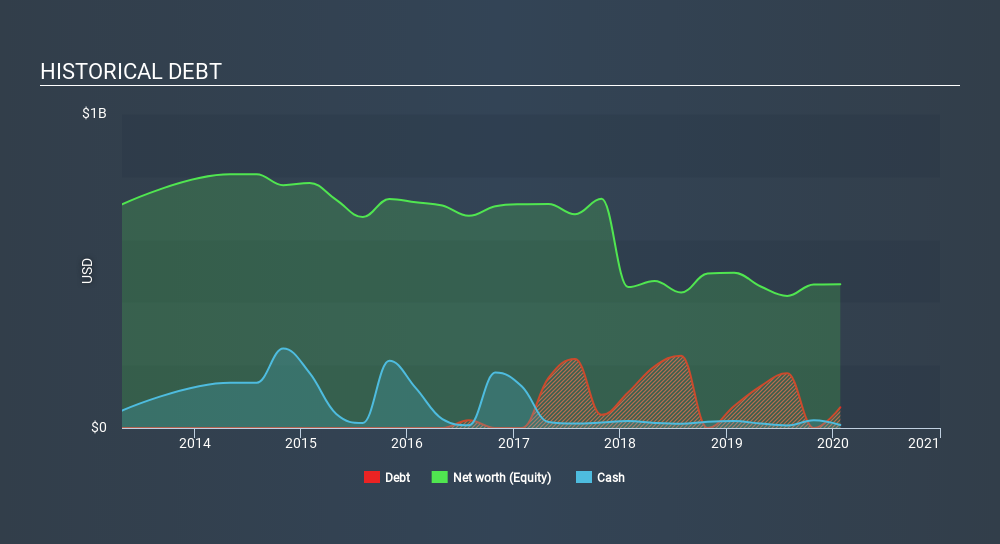

The image below, which you can click on for greater detail, shows that Barnes & Noble Education had debt of US$65.9m at the end of January 2020, a reduction from US$70.1m over a year. On the flip side, it has US$9.80m in cash leading to net debt of about US$56.1m.

How Healthy Is Barnes & Noble Education's Balance Sheet?

The latest balance sheet data shows that Barnes & Noble Education had liabilities of US$685.0m due within a year, and liabilities of US$285.7m falling due after that. Offsetting these obligations, it had cash of US$9.80m as well as receivables valued at US$238.0m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$722.8m.

This deficit casts a shadow over the US$58.4m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Barnes & Noble Education would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Given net debt is only 0.70 times EBITDA, it is initially surprising to see that Barnes & Noble Education's EBIT has low interest coverage of 1.7 times. So while we're not necessarily alarmed we think that its debt is far from trivial. Importantly, Barnes & Noble Education's EBIT fell a jaw-dropping 68% in the last twelve months. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Barnes & Noble Education can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the most recent three years, Barnes & Noble Education recorded free cash flow worth 55% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

On the face of it, Barnes & Noble Education's EBIT growth rate left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its net debt to EBITDA is a good sign, and makes us more optimistic. We're quite clear that we consider Barnes & Noble Education to be really rather risky, as a result of its balance sheet health. So we're almost as wary of this stock as a hungry kitten is about falling into its owner's fish pond: once bitten, twice shy, as they say. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Be aware that Barnes & Noble Education is showing 4 warning signs in our investment analysis , you should know about...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:BNED

Barnes & Noble Education

Operates bookstores for college and university campuses, and K-12 institutions primarily in the United States.

Slight risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|37.6% undervalued

TR

Community Contributor