Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:BBY

Is Best Buy’s 3.7% Stock Rebound a Sign of Changing Value in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Curious if Best Buy is a hidden gem or waiting for a turnaround? Let’s dig into what the numbers and recent events say about its value.

- Best Buy’s stock has seen a 3.7% bounce over the last week but is still down 8.0% year-to-date. This suggests sentiment might be shifting or that risks are being reassessed.

- Recent headlines highlight intensified competition from both online giants and specialty electronics retailers, as well as persistent supply chain and consumer demand concerns. These developments have been key drivers of the stock's short-term ups and downs.

- On our simple valuation score, Best Buy registers a 2 out of 6. This means it is currently undervalued in only two categories. Next, we will walk through what those checks mean and explore alternative valuation angles, including a better way to know if this stock is truly worth your attention.

Best Buy scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Best Buy Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model works by projecting a company's future cash flows and then discounting those projections back to today's value to estimate its intrinsic worth. This helps investors gauge whether a stock is attractively valued compared to its current market price.

For Best Buy, the current Free Cash Flow is about $1.48 billion. Analyst estimates suggest that Free Cash Flow will grow steadily, reaching approximately $2.20 billion by 2030. While analyst coverage usually extends only five years, further projections are systematically extrapolated to provide a ten-year outlook.

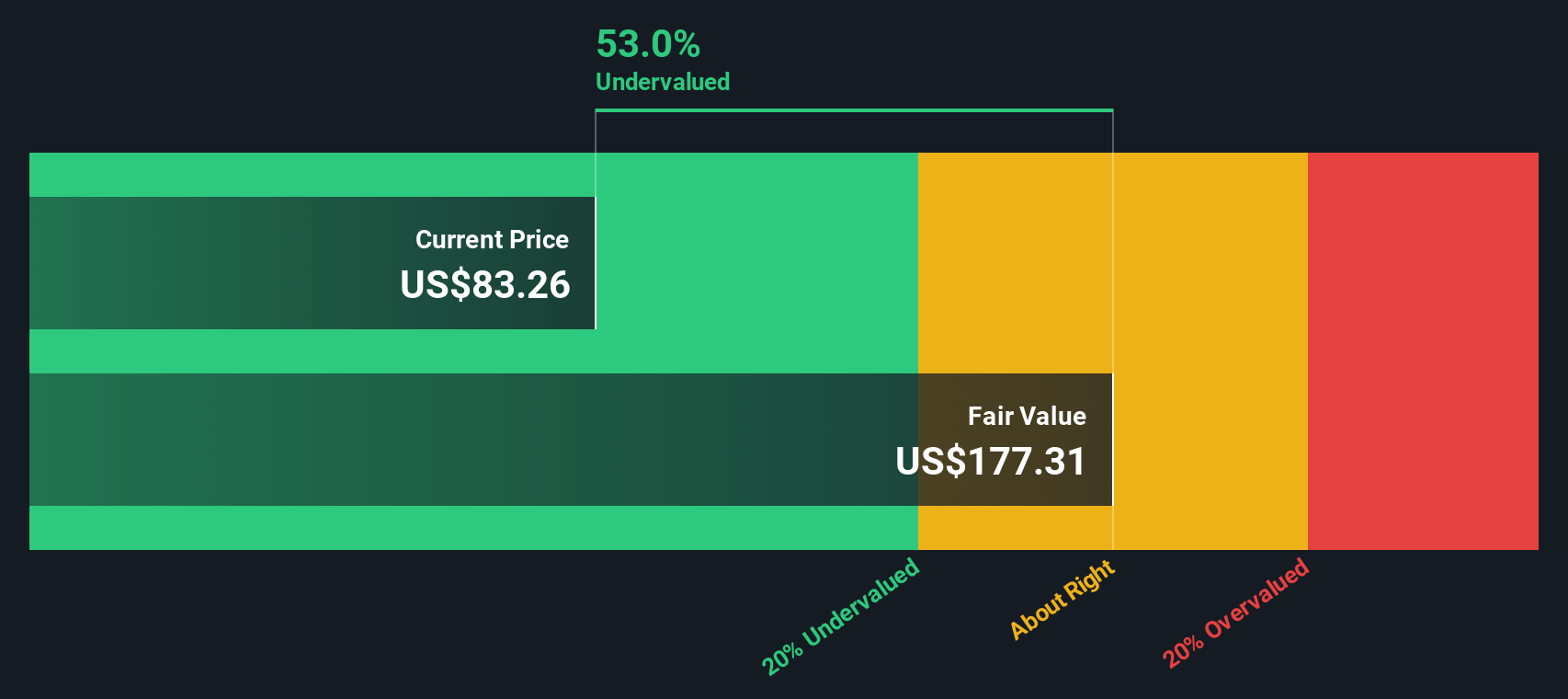

Simply Wall St's DCF analysis uses a two-stage Free Cash Flow to Equity model, taking into account these projected cash flows and their appropriate discount rates. Using this approach, Best Buy's estimated intrinsic value is $173.28 per share. The current market price is trading at a 54.2% discount to this intrinsic value, which indicates that Best Buy is undervalued according to its future cash flow outlook.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Best Buy is undervalued by 54.2%. Track this in your watchlist or portfolio, or discover 917 more undervalued stocks based on cash flows.

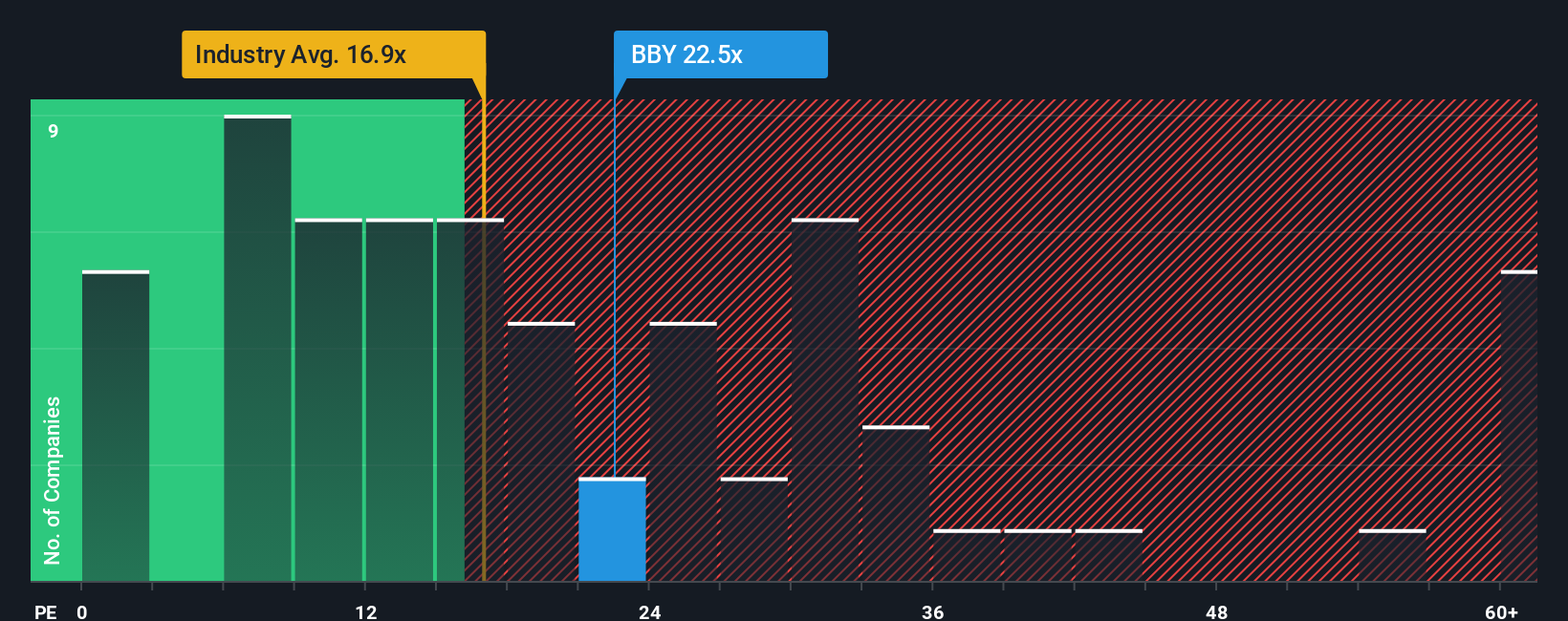

Approach 2: Best Buy Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is one of the most widely used valuation tools for profitable companies like Best Buy. It shows how much investors are willing to pay today for each dollar of earnings, which can be a useful signal for assessing whether a stock is trading at an attractive price relative to its profits.

Growth expectations and perceived risks play a big part in shaping what is considered a “normal” or “fair” PE ratio for a company. Higher growth prospects or lower risks tend to justify a higher PE, while slower growth or more uncertainty typically push it lower.

Currently, Best Buy trades at a PE ratio of 25.8x. This is above the specialty retail industry average of 18.0x and higher than its peers, who on average trade at 22.1x. However, headline comparisons do not always tell the full story. That is where Simply Wall St’s “Fair Ratio” comes in. This proprietary benchmark incorporates growth expectations, profit margins, risk profile, market cap, and industry nuance to deliver a more tailored view. For Best Buy, the Fair Ratio is 22.6x, suggesting a more precise target multiple based on the company’s unique situation.

Compared to its Fair Ratio, Best Buy’s current PE ratio is only slightly higher, with the difference well under the typical range that would signal a clear over- or undervaluation. This suggests the stock is trading about right based on today’s earnings outlook and risk-adjusted profile.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Best Buy Narrative

Earlier, we mentioned there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is a simple, powerful way to blend your perspective or "story" about a company, such as how you expect its revenue, margins, and earnings to evolve, with a financial forecast and a fair value estimate. This approach goes deeper than just running numbers; it connects what you think will happen with what that means for the stock's real worth.

Narratives are available to everyone right within Simply Wall St’s Community page, making it easy for millions of investors to create and compare different views. They help you decide when to buy or sell by letting you see how your fair value estimate compares to the current price. Whenever new news or company results are released, Narratives update automatically, ensuring your investment decisions stay relevant and informed.

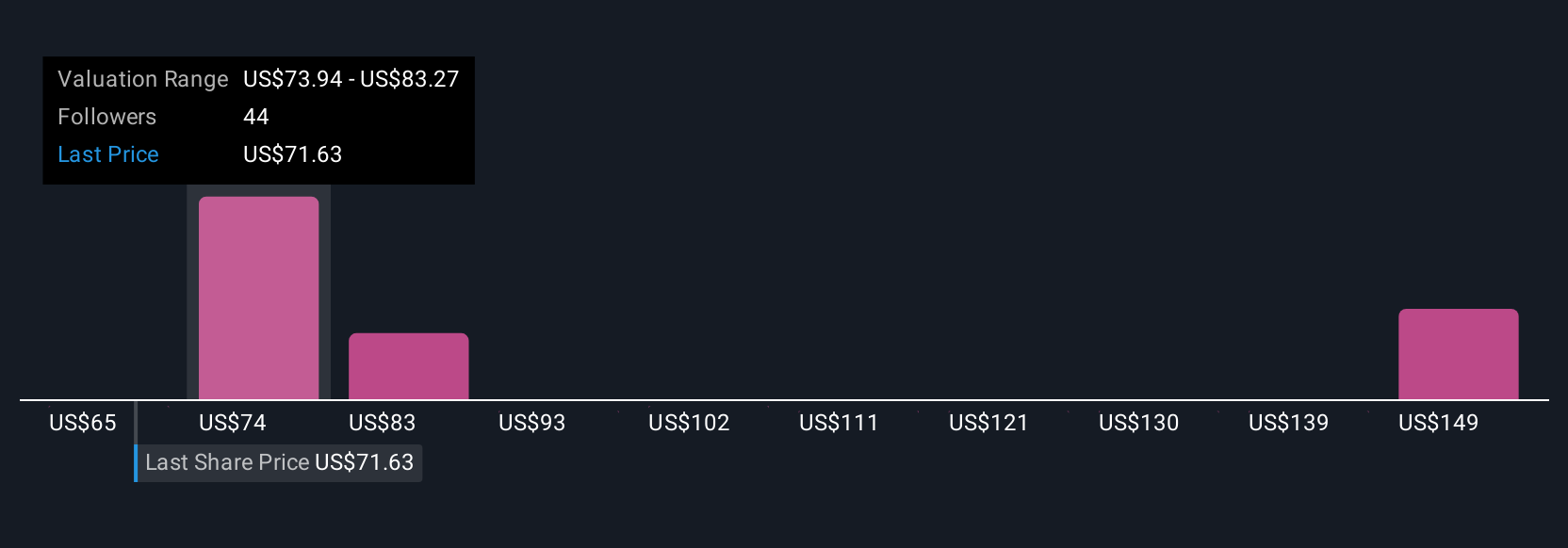

For example, one investor might believe ongoing cost-cutting, tech upgrades, and new services will drive Best Buy’s share price much higher. Another investor could see mounting online competition and shrinking margins as reasons for a bleaker outlook. One sets a fair value at $95 per share, while the other puts it at just $60.

Do you think there's more to the story for Best Buy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Best Buy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BBY

Best Buy

Offers technology products and solutions in the United States, Canada, and internationally.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

932 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative