Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:ABG

Will Analyst Attention on Asbury Automotive Group (ABG) Prompt a Rethink of Its Growth Trajectory?

Simply Wall St

Reviewed by Sasha Jovanovic

- Barclays recently initiated coverage on Asbury Automotive Group with an Equal-Weight rating, joining a period of heightened analyst activity, including rating actions from JP Morgan and Stephens & Co.

- This surge in analyst engagement reflects increased market attention on Asbury’s outlook and may prompt investors to reassess the company’s prospects and challenges.

- With Barclays’ new coverage highlighting shifting analyst perspectives, we’ll explore how this could influence Asbury Automotive Group’s investment narrative going forward.

We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Asbury Automotive Group Investment Narrative Recap

To be a shareholder in Asbury Automotive Group, you need to believe in its ability to execute on acquisition-led growth, strengthen profit margins through operational efficiency, and manage industry shifts toward digital sales. The recent Barclays initiation with an Equal-Weight rating, alongside other analyst actions, does not materially alter the company’s most important short-term catalyst, success integrating the Herb Chambers acquisition, nor does it immediately address the key risk from elevated leverage and related financial pressures. One recently announced development with direct relevance is Asbury’s sizable real estate term loan, secured in July, to fund expansion activities. This financing deepens the company’s bet on growth via acquisitions, but also elevates leverage at a time when successful integration and cost management are crucial for realizing anticipated synergies and protecting future profitability. By contrast, the company’s elevated leverage and financial flexibility are factors that investors should keep in mind as they consider...

Read the full narrative on Asbury Automotive Group (it's free!)

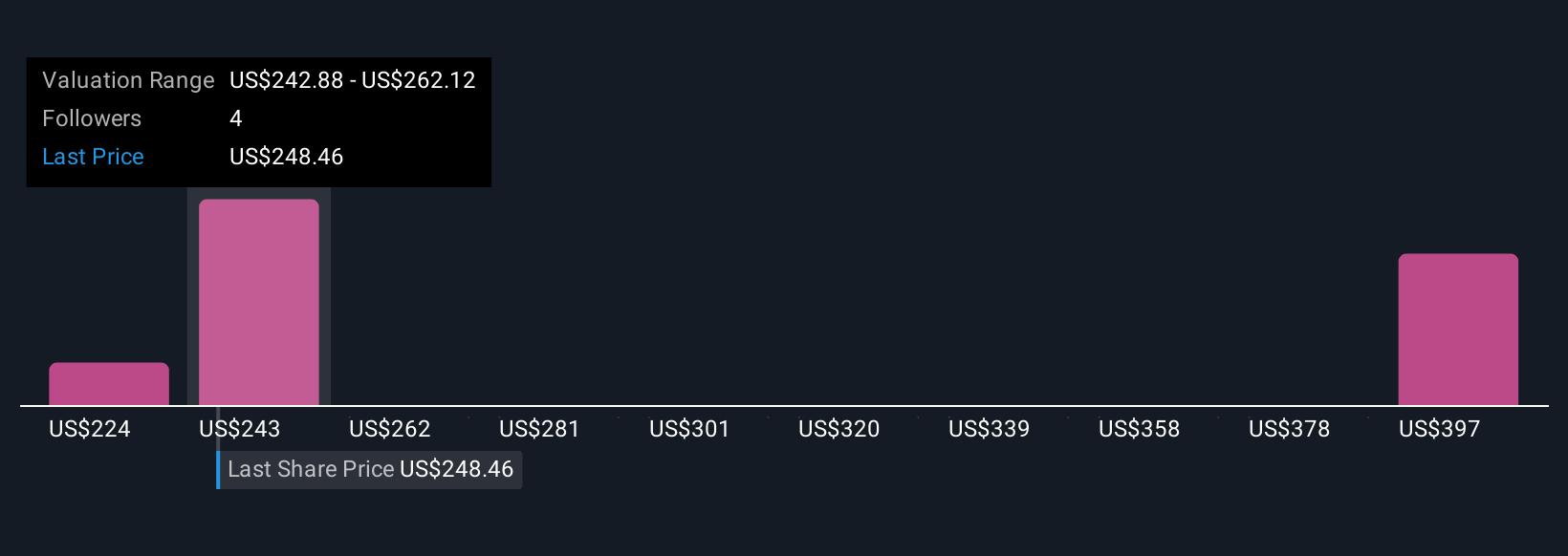

Asbury Automotive Group's narrative projects $21.6 billion in revenue and $676.4 million in earnings by 2028. This requires 7.7% yearly revenue growth and a $136.4 million earnings increase from $540.0 million in current earnings.

Uncover how Asbury Automotive Group's forecasts yield a $261.75 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community members have shared fair value estimates for Asbury, ranging widely from US$223.65 to US$446.36 per share. While some see significant upside potential, others remain cautious, echoing the ongoing debate about the risks of acquisition-driven growth and sustained debt levels.

Explore 3 other fair value estimates on Asbury Automotive Group - why the stock might be worth over 2x more than the current price!

Build Your Own Asbury Automotive Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Asbury Automotive Group research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Asbury Automotive Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Asbury Automotive Group's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our top stock finds are flying under the radar-for now. Get in early:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ABG

Asbury Automotive Group

Operates as an automotive retailer in the United States.

Undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor