Advertisement

- United States

- /

- Specialty Stores

- /

- NasdaqGS:URBN

Does Urban Outfitters Rally After Free People Expansion Signal a Good Entry in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Urban Outfitters stock is a hidden gem or overhyped? If you have even a passing curiosity about how much the company is really worth, you are in the right place.

- Urban Outfitters has caught investor attention with its shares up 21.0% over the past week, 36.5% year-to-date, and a 59.2% jump over the last year. This puts growth potential and risk in the spotlight.

- Much of this momentum has come alongside major headlines such as the company’s expansion of its Free People brand and new technology investments. Both of these factors have stirred up bullish sentiment among retail watchers. These updates provide fresh fuel for the price surge and shape how analysts and investors are weighing the next moves.

- On our valuation scorecard, Urban Outfitters clocks a 4 out of 6 for being undervalued. This suggests there is real substance behind the hype. We will break down what goes into that score using several valuation approaches, so stick around because the most revealing perspective might come at the end of this article.

Approach 1: Urban Outfitters Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's value by projecting its future cash flows and discounting them back to today's dollars. This approach helps investors determine what a business is truly worth based on how much cash it is expected to generate going forward.

For Urban Outfitters, the most recent Free Cash Flow stands at $403 million. Analysts forecast modest growth, projecting the company's Free Cash Flow to reach roughly $453 million by 2029. After analyst estimates end, Simply Wall St extends these projections using estimated trends and moderate improvements in annual cash flow over a ten-year period.

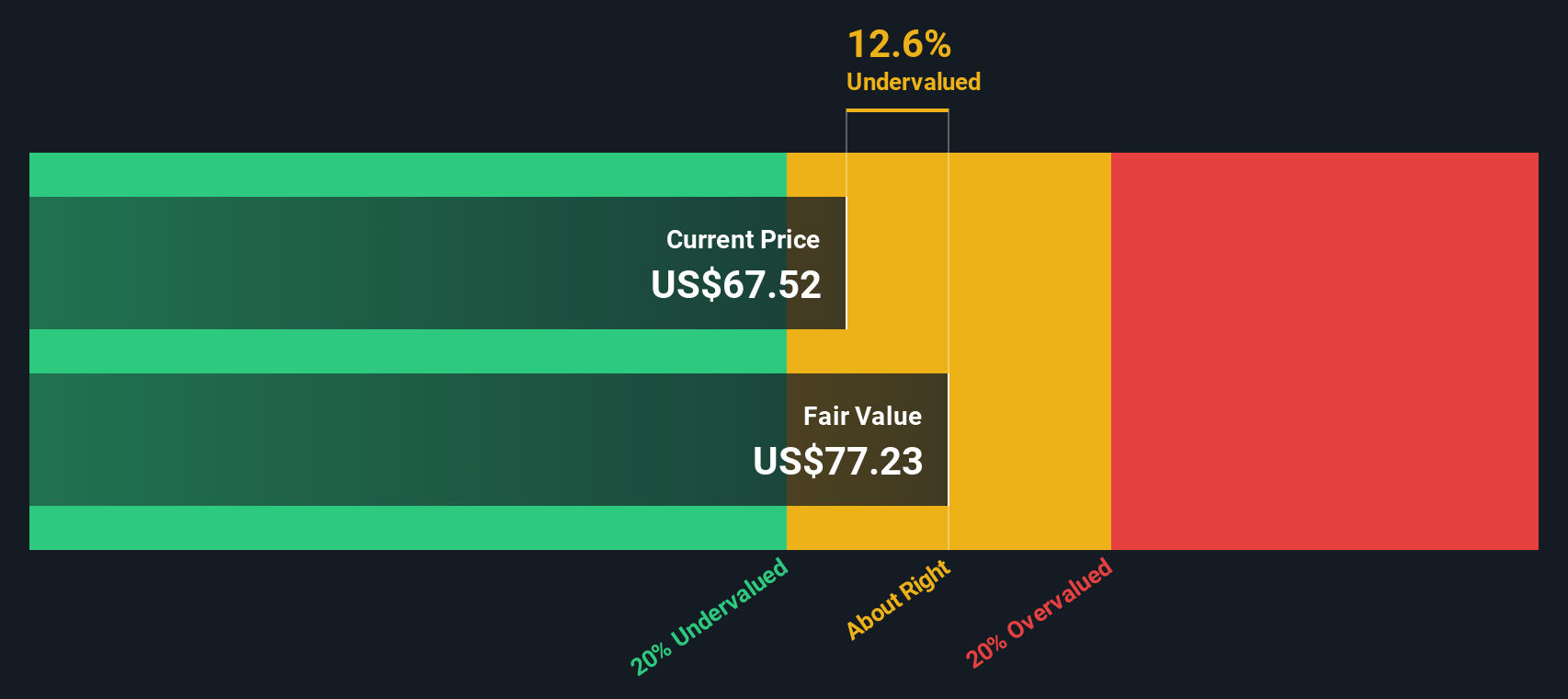

Using this two-stage DCF model, the calculated intrinsic value per share is $84.14. Compared to the current market price, this implies the stock trades at a 7.8% discount to its fair value. In other words, while there is some undervaluation, it is not extreme.

Result: ABOUT RIGHT

Urban Outfitters is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Urban Outfitters Price vs Earnings

The price-to-earnings (PE) ratio is widely used to value profitable companies because it ties a company's stock price directly to its actual earnings. For investors, the PE ratio offers a straightforward way to assess how much they are paying for each dollar of earnings. This can be helpful when considering if a stock's price makes sense given its current profit levels.

Deciding what counts as a “fair” or “normal” PE ratio largely depends on growth expectations and risk. A company with rapid growth and low risk can justify a higher PE ratio, since investors are willing to pay more today for greater potential future profits. In contrast, higher risks or stagnating growth typically warrant lower PE multiples.

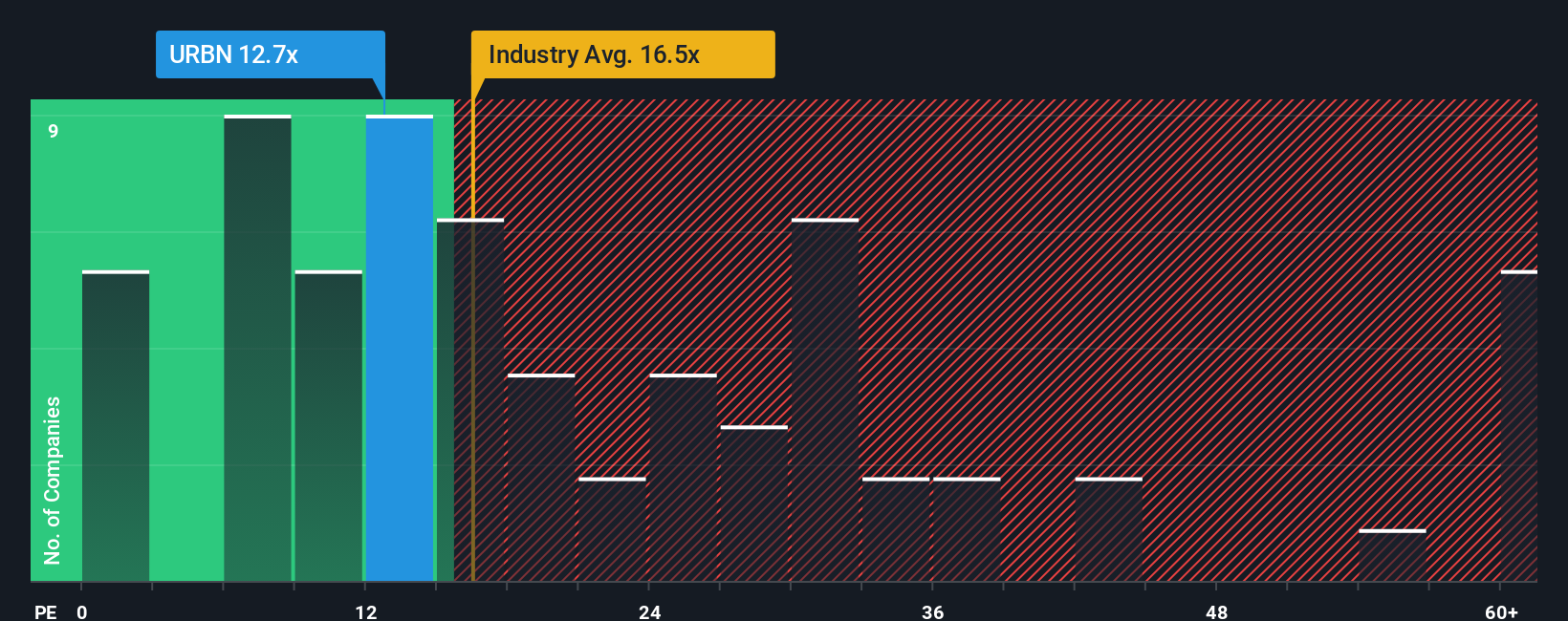

Urban Outfitters currently trades at a PE ratio of 14.2x. For context, this sits below the Specialty Retail industry average of 18.0x and below the average of its closest peers at 16.6x. On the surface, this might suggest the stock is undervalued compared to its sector.

However, Simply Wall St’s proprietary “Fair Ratio” model calculates what Urban Outfitters’ PE ratio should be, taking into account the company’s specific growth outlook, profit margins, risk profile, market cap, and industry positioning. Unlike a basic peer or industry comparison, the Fair Ratio provides a more nuanced target that adjusts for what truly makes Urban Outfitters unique in the market.

For Urban Outfitters, the Fair Ratio is 16.5x. With the stock currently trading at 14.2x, this places its valuation slightly below what Simply Wall St’s model deems appropriate. Still, the difference is modest.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1438 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Urban Outfitters Narrative

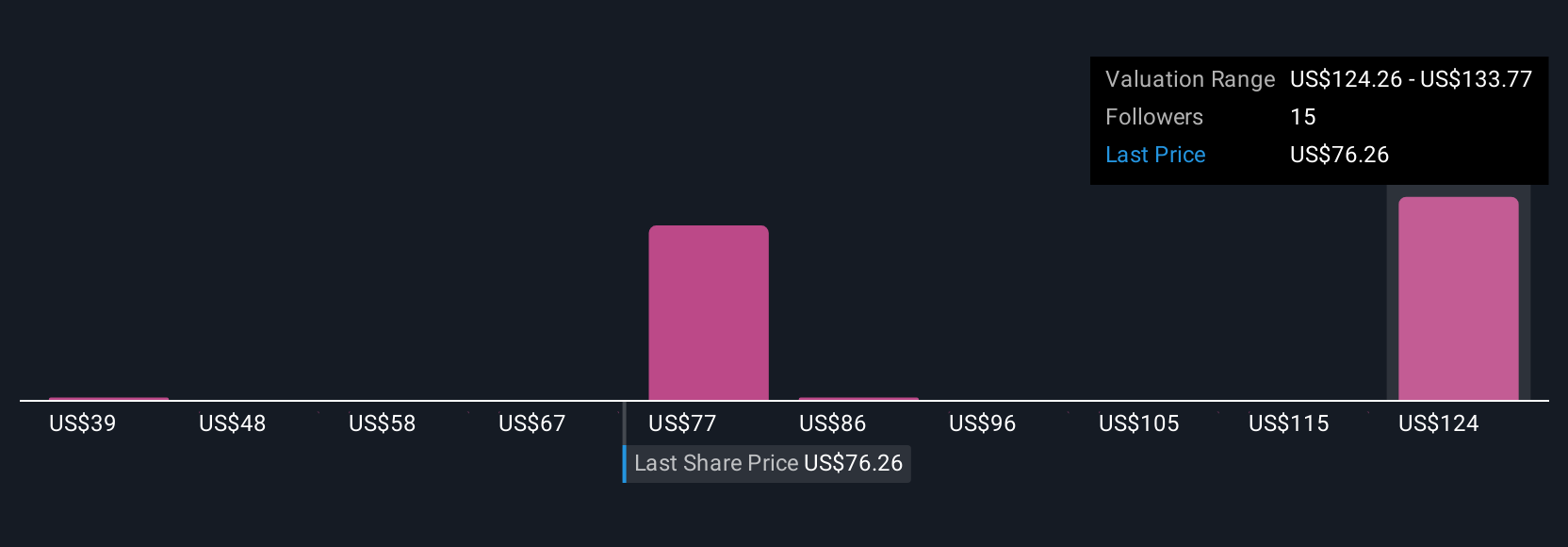

Earlier we mentioned that there is an even better way to understand valuation. Let's introduce you to Narratives. A Narrative is a simple, yet powerful, way for investors to bring their view of a company’s story together with objective financial forecasts, such as fair value estimates, future growth, and profit margins, so you can see how your perspective stacks up against both peers and numbers. Narratives start with your beliefs about Urban Outfitters' future and link them to financial assumptions, like revenue or earnings trends. They instantly calculate a fair value based on your scenario, all within the Community page on Simply Wall St's platform, where millions of investors share and compare insights.

With Narratives, you can easily decide when to buy or sell by comparing your scenario-based Fair Value to the current stock price. Since they update dynamically with new news or earnings, your analysis always stays relevant. For example, an optimistic investor might project that Urban Outfitters earns $615.7 million in 2028 (implying a fair value of $93.0). A more cautious view could peg earnings at just $451 million (with a fair value of $52.0), showing how different stories can change a valuation dramatically.

Do you think there's more to the story for Urban Outfitters? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:URBN

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

96 followersusers have followed this narrative

10 commentsusers have commented on this narrative

19 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative