Advertisement

- United States

- /

- Specialty Stores

- /

- NasdaqGS:UPBD

Will Upbound Group’s (UPBD) Extended Debt Maturity Strengthen Its Long-Term Financial Flexibility?

Simply Wall St

Reviewed by Simply Wall St

- On August 19, 2025, Upbound Group, Inc. announced it had amended its Term Loan Credit Agreement, extending the loan maturity to August 19, 2032, and secured an additional US$77 million in incremental commitments, resulting in total aggregate borrowings of US$875 million under the agreement.

- This amendment points to improved liquidity and enhanced financial flexibility for Upbound Group, allowing the company greater capacity to manage working capital and corporate initiatives.

- We’ll now examine how Upbound Group’s extension of its loan maturity could influence the sustainability of its investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Upbound Group Investment Narrative Recap

To be a shareholder in Upbound Group, you need to believe in its ability to generate sustainable growth through merchant expansion, new product offerings, and operational improvements, while managing financing costs and competitive pressures. The recent extension of the company’s term loan maturity to 2032 improves liquidity, but its impact on the most important short-term catalyst, merchant partner growth, and the biggest current risk from regulatory and legal challenges does not appear materially changed for now.

Among company developments, the May 2025 opening of a new Rent-A-Center store in Harlan, Kentucky stands out, reflecting Upbound’s ongoing focus on scale and physical presence. While these expansion efforts may play into merchant and revenue growth catalysts, short-term investor attention may remain on Upbound’s financial flexibility and ability to navigate regulatory headwinds. Yet, with the regulatory lawsuit against Acima leasing ongoing, investors should be mindful of...

Read the full narrative on Upbound Group (it's free!)

Upbound Group's narrative projects $4.8 billion revenue and $278.5 million earnings by 2028. This requires 3.9% yearly revenue growth and a $197.3 million increase in earnings from $81.2 million today.

Uncover how Upbound Group's forecasts yield a $36.25 fair value, a 44% upside to its current price.

Exploring Other Perspectives

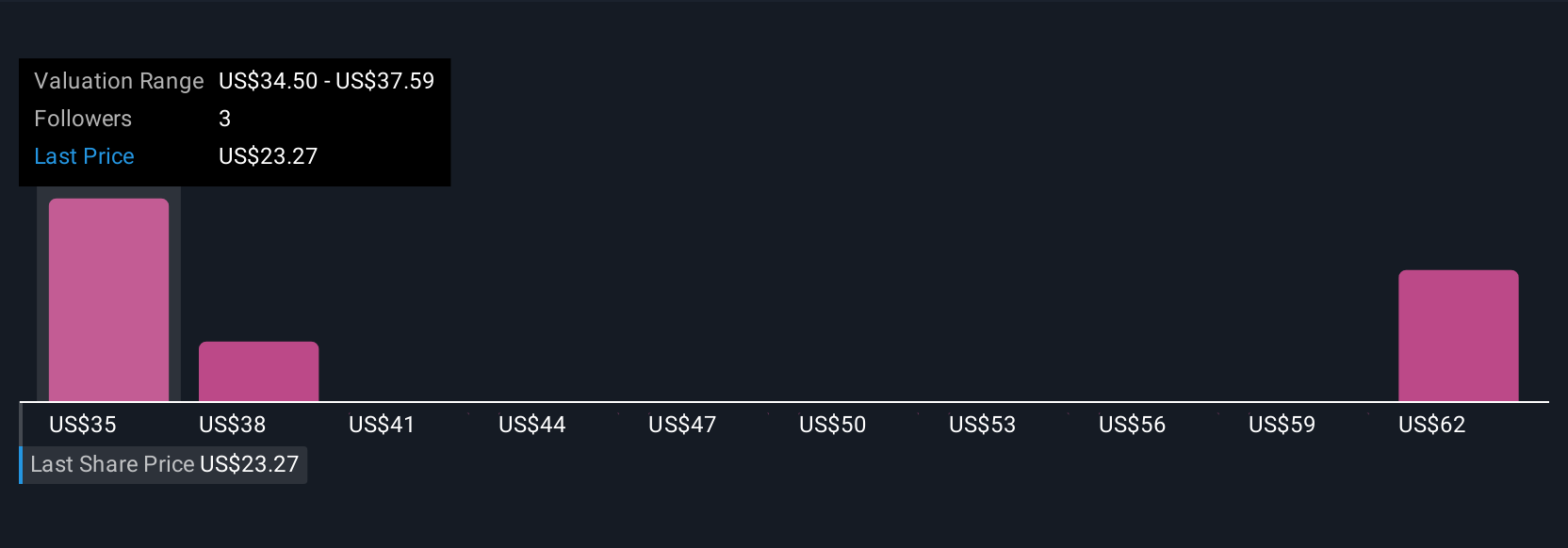

Simply Wall St Community members have produced four distinct fair value estimates ranging from US$34.50 to US$67.24 per share. Many highlight growth expectations as a key factor, but concerns about regulatory and legal uncertainty are front of mind for some, offering you several contrasting viewpoints to consider.

Explore 4 other fair value estimates on Upbound Group - why the stock might be worth over 2x more than the current price!

Build Your Own Upbound Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Upbound Group research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Upbound Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Upbound Group's overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:UPBD

Upbound Group

Upbound Group, Inc. leases household durable goods to customers on a lease-to-own basis in the United States, Puerto Rico, and Mexico.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|51.2% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|6.7% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|24.6% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|53.6% overvalued

RO

Community Contributor