Advertisement

- United States

- /

- General Merchandise and Department Stores

- /

- NasdaqGM:OLLI

Ollie’s Bargain Outlet Holdings (OLLI): Is the Stock Undervalued After a Strong Run This Year?

Simply Wall St

Reviewed by Simply Wall St

Ollie's Bargain Outlet Holdings (OLLI) has quietly outpaced the market this year, with shares up 17% year to date. Recent trading activity suggests investors are paying closer attention, likely because of the company's solid revenue and earnings growth.

See our latest analysis for Ollie's Bargain Outlet Holdings.

After a strong run earlier in the year, Ollie's has shifted gears, with its 7-day share price return of 2.4% suggesting renewed momentum as investors recognize the company’s improving fundamentals. The stock’s 1-year total shareholder return of nearly 38% highlights how much confidence has grown around its long-term growth prospects.

If Ollie’s latest move has you looking for more fast-rising retailers, this could be the perfect chance to discover fast growing stocks with high insider ownership

With Ollie’s stock now trading near all-time highs and outperforming the market, the real question is whether there is still room for upside or if the market has already priced in much of the expected future growth.

Most Popular Narrative: 13.4% Undervalued

Ollie’s last traded at $127, but the most widely followed narrative pegs fair value around $146.60, implying upside. This outlook relies heavily on whether recent momentum in revenue and margins can propel long-term returns above current market expectations.

The company is benefiting from a growing value-conscious consumer base, amplified by economic uncertainty and inflation. This is driving more customers toward discount retailers like Ollie's, boosting both store traffic and revenue growth, as seen by accelerated customer acquisition and rising loyalty program membership. (Revenue)

Want to know what drives this premium? The key lies in a bullish forecast of future earnings growth, with high-multiple valuations more often seen in fast-growing disruptors. What are analysts betting on that the market might be missing? Unlock the bold assumptions behind this winning narrative.

Result: Fair Value of $146.60 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Ollie's rapid store expansion and dependence on closeout inventory could pose risks if new locations underperform or if supply becomes less abundant.

Find out about the key risks to this Ollie's Bargain Outlet Holdings narrative.

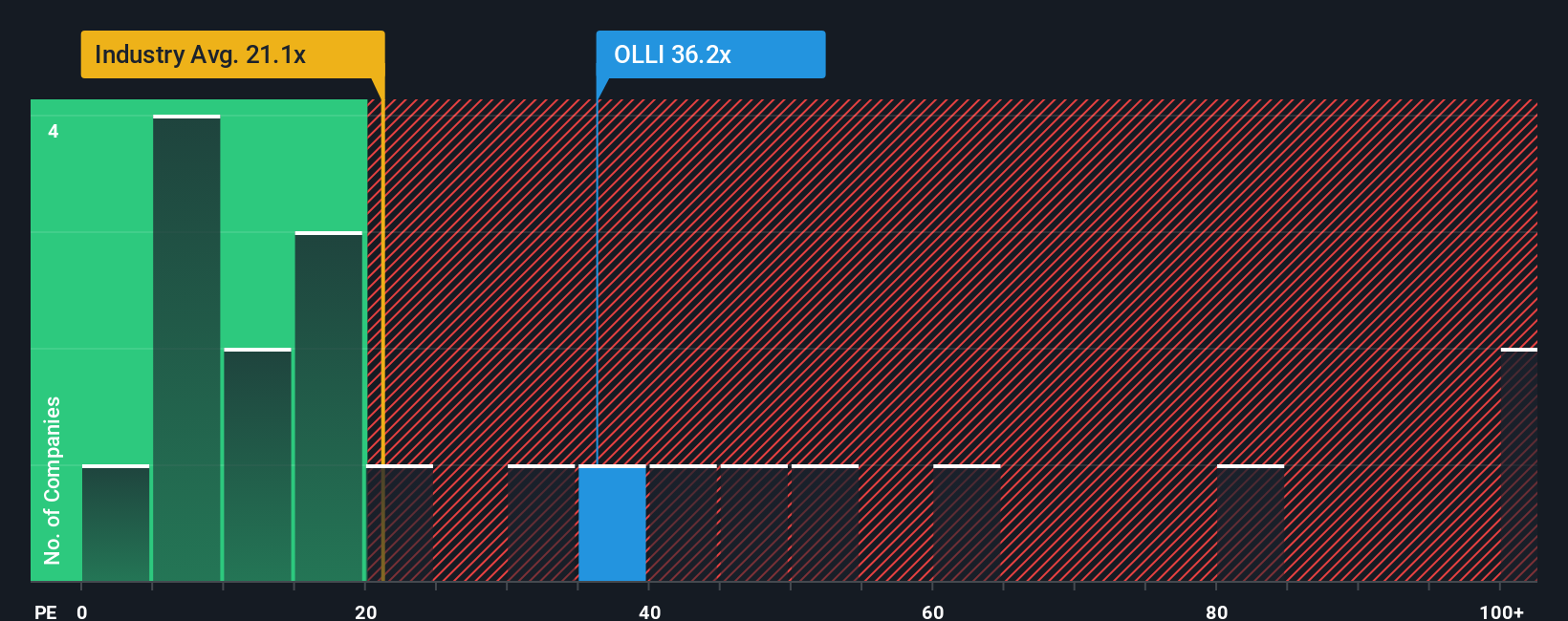

Another View: Multiples Paint a Cautious Picture

Looking at traditional valuation ratios, Ollie’s is trading at a price-to-earnings ratio of 36.5x. That is significantly higher than its peer average of 20.3x, the global industry’s 19.9x, and even the fair ratio of 19x. This large gap highlights valuation risk, as investors are paying a premium for future growth today. Will Ollie’s continue delivering on expectations, or could sentiment shift if growth wobbles?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Ollie's Bargain Outlet Holdings Narrative

If you have your own ideas or want to dig deeper into the numbers, building your own narrative is quick and easy. You can get started in just a few minutes. Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Ollie's Bargain Outlet Holdings.

Looking for More Investment Ideas?

Don't miss your chance to supercharge your portfolio with investment themes on the rise. Some of the market's most promising opportunities are waiting for you to act now.

- Unlock income potential by checking out these 15 dividend stocks with yields > 3%, offering attractive yields and steady cash flow for your next dividend play.

- Tap into the future of medicine as innovation accelerates by browsing these 32 healthcare AI stocks, at the forefront of AI-powered healthcare solutions.

- Move early where value meets momentum with these 858 undervalued stocks based on cash flows, which could be trading below their intrinsic worth right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:OLLI

Ollie's Bargain Outlet Holdings

Operates as a retailer of closeout merchandise and excess inventory in the United States.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor