Advertisement

- United States

- /

- Specialty Stores

- /

- NasdaqGS:FIVE

Five Below (NASDAQ:FIVE) Is Looking To Continue Growing Its Returns On Capital

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Speaking of which, we noticed some great changes in Five Below's (NASDAQ:FIVE) returns on capital, so let's have a look.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Five Below is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

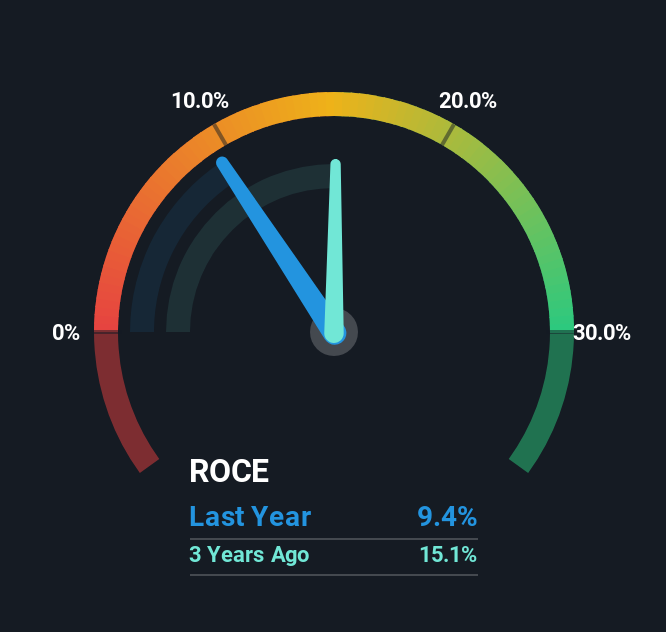

0.094 = US$339m ÷ (US$4.5b - US$862m) (Based on the trailing twelve months to May 2025).

Therefore, Five Below has an ROCE of 9.4%. In absolute terms, that's a low return and it also under-performs the Specialty Retail industry average of 13%.

View our latest analysis for Five Below

Above you can see how the current ROCE for Five Below compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free analyst report for Five Below .

What Can We Tell From Five Below's ROCE Trend?

Even though ROCE is still low in absolute terms, it's good to see it's heading in the right direction. Over the last five years, returns on capital employed have risen substantially to 9.4%. The amount of capital employed has increased too, by 129%. The increasing returns on a growing amount of capital is common amongst multi-baggers and that's why we're impressed.

What We Can Learn From Five Below's ROCE

In summary, it's great to see that Five Below can compound returns by consistently reinvesting capital at increasing rates of return, because these are some of the key ingredients of those highly sought after multi-baggers. Since the stock has only returned 18% to shareholders over the last five years, the promising fundamentals may not be recognized yet by investors. So with that in mind, we think the stock deserves further research.

Like most companies, Five Below does come with some risks, and we've found 1 warning sign that you should be aware of.

While Five Below may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:FIVE

Five Below

Operates as a specialty value retailer in the United States.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0769.0% undervalued

290 followersusers have followed this narrative

1 commentusers have commented on this narrative

43 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.1% undervalued

106 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4524.2% undervalued

8 followersusers have followed this narrative

3 commentsusers have commented on this narrative

4 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2802.6% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

FU

FundamentalFlow on Samsara ·

Samsara’s 30% ARR Growth Could Drive 70%+ Upside

Fair Value:US$6554.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Boab Metals ·

Aussie's Silver Play Ignored by Mr. Legend Eric Sprott

Fair Value:AU$11.6996.3% undervalued

5 followersusers have followed this narrative

4 commentsusers have commented on this narrative

1 likeusers have liked this narrative

KA

kapirey on Karoon Energy ·

Karoon Energy will target efficiency and cost reduction with Brazilian FPSO acquisition

Fair Value:AU$2.6725.8% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.1% undervalued

106 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.229.5% undervalued

70 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9326.1% undervalued

1399 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative