Arhaus (ARHS) has attracted attention following recent trading activity, as shares saw moderate gains over the past week. Investors seem to be weighing the company's steady position in the home furnishings sector in light of broader market shifts.

Arhaus’s recent share price jump, capped by an impressive 18% return over the last week, has caught the eye of investors. While the 1-year total shareholder return sits at a modest 3.8%, momentum appears to be building again after a period of slower performance. This suggests renewed optimism around the company’s outlook.

Given Arhaus’s recent rally and solid returns, the key question now is whether shares remain undervalued and offer further upside, or if the market has already priced in the company’s future growth prospects.

Advertisement

Most Popular Narrative: 6.7% Undervalued

Arhaus's most-followed narrative suggests the shares are trading below the calculated fair value, with the last close at $10.48 versus a fair value estimate of $11.23. This difference points to room for upside if forecasts and assumptions play out as projected.

Ongoing investment in omnichannel platforms, digital content, and supply chain efficiency, including successful in-sourcing of distribution and implementation of new inventory/ERP systems, are expected to improve operating leverage and expand net margins as scale increases.

Curious what bold moves and aggressive expansion plans underpin this ambitious fair value estimate? The secret to this valuation lies in projections of margin gains and future revenue growth that challenge conventional expectations. Discover the core assumptions that could reshape Arhaus’s trajectory. Click through to unpack the financial story behind the stock.

However, persistent consumer uncertainty and rising input costs could challenge Arhaus’s growth narrative. These factors may potentially impact revenue momentum and future margin expectations.

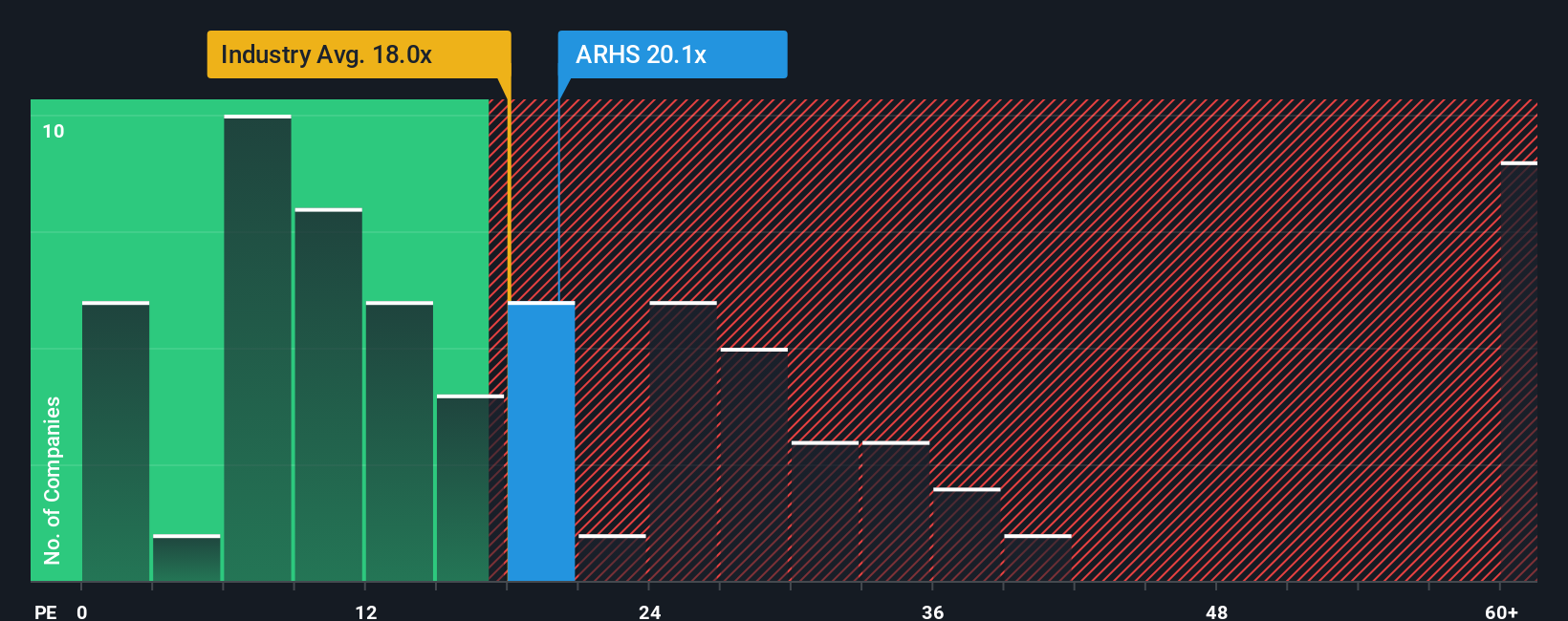

Taking a look at Arhaus's valuation through the lens of its price-to-earnings ratio, a different picture emerges. Shares are trading at 20.1 times earnings, which is higher than both the Specialty Retail industry average of 18.9 and the fair ratio of 15.2. This suggests investors are paying a premium, possibly making the stock more vulnerable to a shift in market sentiment. Could the premium be justified or is there risk in the current setup?

If you have a different take or want to dig into the numbers personally, you can easily craft your own narrative in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Arhaus.

Looking for More Investment Ideas?

Don’t let fresh investment opportunities pass you by. The right ideas at your fingertips today could fuel the results you want tomorrow. Here are a few standout stock themes you’ll want to consider:

Unleash the future of medicine by starting with these 30 healthcare AI stocks transforming healthcare with intelligent diagnostics and innovations in treatment.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks