Advertisement

- United States

- /

- General Merchandise and Department Stores

- /

- NasdaqGS:AMZN

Amazon.com (AMZN) Faces A Valuation Test Following AWS’s $1b AI Engineering Push

Amazon.com (AMZN) is back in focus after Amazon Web Services committed US$1b of internal resources to a new Forward Deployed Engineering division, embedding AI specialists inside client organizations to speed up enterprise adoption of artificial intelligence.

See our latest analysis for Amazon.com.

Amazon.com’s share price has been choppy recently, with the stock down about 12% on a 30 day share price return yet still showing a 13% gain over 90 days and an 8% 1 year total shareholder return. This suggests longer term momentum has held up despite renewed questions about heavy AI spending and regulatory scrutiny as AWS commits US$1b to forward deployed AI engineers.

If you are looking beyond Amazon.com for AI related opportunities, this is a good moment to see how other smaller players are positioned and scan 32 AI small caps.

With Amazon.com shares recently under pressure and Simply Wall St’s models suggesting the stock trades below both intrinsic value and analyst targets, the key question for investors is whether this weakness is a genuine opportunity or if the market is already correctly pricing in future growth potential.

Most Popular Narrative: 47% Undervalued

At a last close of $238.34 versus a fair value of $450 in the most followed narrative, Amazon.com is framed as materially mispriced, with current AI heavy spending seen as laying the groundwork for future earnings power rather than eroding it.

Amazon is sacrificing short-term margins to secure long-duration dominance in AI infrastructure, advertising, and automated commerce. These investments are already working, and margins are positioned to inflect upward by the end of 2026.

Want to see how this narrative gets to a much higher fair value for Amazon.com? It leans on accelerating earnings, rising margins and a richer future profit multiple. Curious which revenue streams and profit profile need to line up to support that target price? The full narrative breaks down the assumptions hiding behind those headline numbers.

Result: Fair Value of $450 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on Amazon.com continuing to win large AI workloads and keeping regulators at bay, because any slowdown or tighter rules could quickly challenge that bullish case.

Find out about the key risks to this Amazon.com narrative.

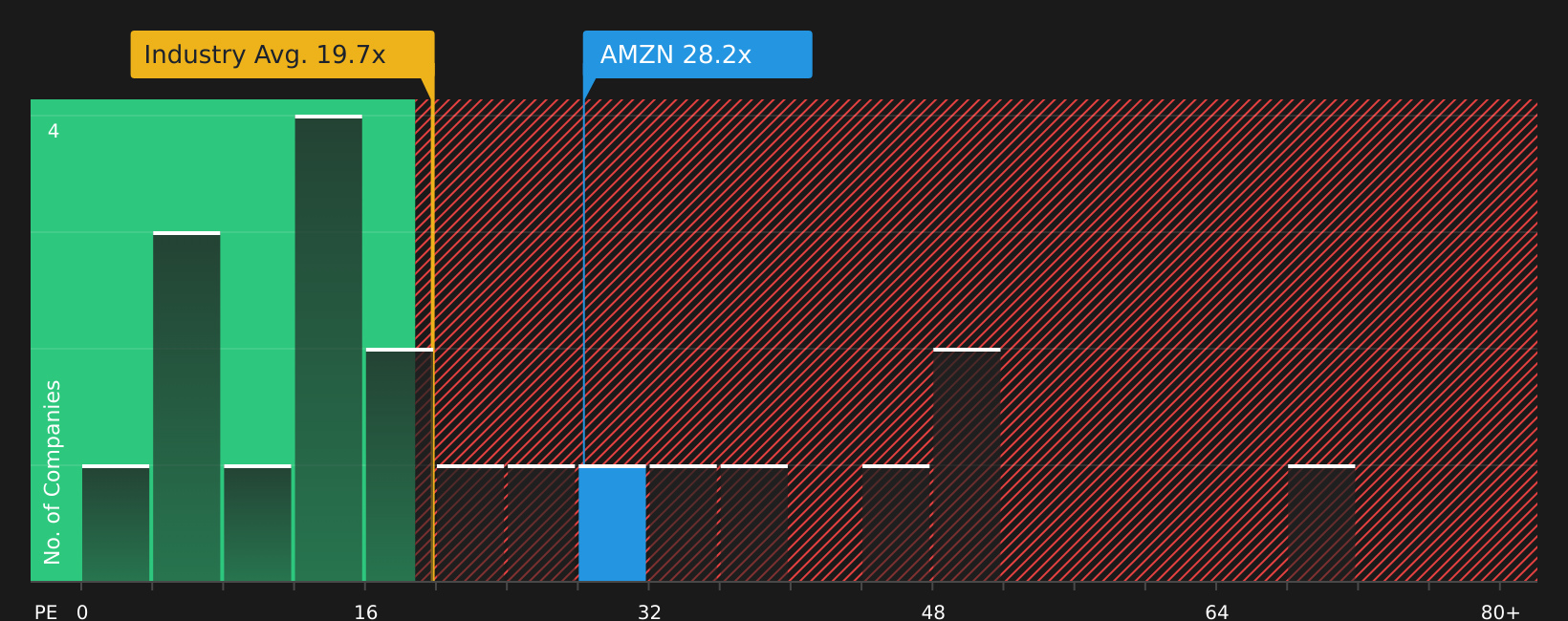

Another View: Amazon.com Looks Expensive On P/E

While the user narrative and intrinsic value work point to Amazon.com as undervalued, the P/E ratio tells a more cautious story. At 28.2x earnings, Amazon.com trades above both the global Multiline Retail industry at 19.4x and its peer average at 22.8x, even though the fair ratio is estimated at 45x. That gap suggests investors are already paying a premium today, so it may be worth considering how much upside could remain if earnings or sentiment slip.

For a closer look at what this valuation gap could mean in practice, including how it might limit or widen future upside, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed views on Amazon.com’s valuation and AI spending, this is a good time to review the numbers yourself, weigh both concerns and potential upsides, and then check the 4 key rewards and 1 important warning sign

Looking for more investment ideas beyond Amazon.com?

If you stop with Amazon.com, you could miss other stocks that fit your style, so take a few minutes to widen your watchlist using these focused ideas.

- Target potential mispricing by scanning companies that our models flag as having 43 high quality undervalued stocks based on quality and fundamentals.

- Strengthen your income stream by reviewing stocks in the 10 dividend fortresses that may suit investors who care about sizable, ongoing payouts.

- Limit unpleasant surprises by checking out companies in the 74 resilient stocks with low risk scores that emphasise resilience and more measured risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:AMZN

Amazon.com

Engages in the retail sale of consumer products, advertising, and subscriptions service through online and physical stores in North America and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.559.3% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$4811.0% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8212.9% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

AN

andre_santos on NIKE ·

Nike - A Fundamental and Historical Valuation

Fair Value:US$36.8311.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

TripleS on AnaptysBio ·

ANAB has a scaling and rising royalty stream, one up and coming new royalty, a loan that dies in 2027 which will result in a doubling

Fair Value:US$9025.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GE

Germaine on MM Computer Systems Berhad ·

MM Computer Systems' Latest Contract Wins Reinforce Growth Momentum After Listing

Fair Value:RM 0.3313.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75031.5% undervalued

79 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.9% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.2% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative