Advertisement

- United States

- /

- Office REITs

- /

- NYSE:JBGS

JBG SMITH Properties (JBGS): Evaluating Valuation After Recent Share Price Moves

Simply Wall St

Reviewed by Simply Wall St

JBG SMITH Properties (JBGS) has seen its stock edge slightly higher today, gaining 0.5%. The move comes after a stretch in which the shares have dipped around 13% over the past month. This has drawn investor attention to its recent price action.

See our latest analysis for JBG SMITH Properties.

Despite a challenging month for shareholders, the momentum for JBG SMITH Properties has shifted over the longer run. While the 13.3% one-month share price decline stands out, the company's year-to-date share price return remains a robust 16.3%. In addition, the total shareholder return over the past year has reached 23.3%. This uptrend suggests investors are warming to its recovery potential and possibly reassessing risk.

If the recent rebound in JBG SMITH Properties’ performance has you rethinking your watchlist, now is a great time to broaden your scope with fast growing stocks with high insider ownership

With shares down from prior highs but still up substantially for the year, the key question is whether JBG SMITH Properties remains undervalued at current levels or if the market has already accounted for future gains.

Price-to-Sales of 2.1x: Is it justified?

JBG SMITH Properties is currently valued at a price-to-sales (P/S) ratio of 2.1x, closing at $17.96. This positions the stock almost exactly in line with the US Office REITs industry average for P/S, but slightly above the peer group average.

The price-to-sales ratio compares a company’s market price to its annual revenues. For property companies like JBG SMITH Properties, P/S is a useful metric because earnings can be volatile due to real estate cycles. Revenues, however, tend to be more stable. Investors look to this metric to assess whether they are paying a premium for each dollar of revenue generated by the business.

On its surface, a P/S of 2.1x suggests the market is valuing JBG SMITH Properties in line with the broader sector. However, compared to the peer average of 2x, the company appears fractionally more expensive. This premium could reflect investor optimism about its assets or future prospects. If JBG SMITH Properties underperforms or revenue expectations fall further, the market may re-rate the shares toward the fair P/S ratio of 1.9x.

Result: Price-to-Sales of 2.1x (ABOUT RIGHT)

Explore the SWS fair ratio for JBG SMITH Properties

However, if slowing annual revenue growth and continued net losses persist in upcoming quarters, these trends could undermine the recovery narrative.

Find out about the key risks to this JBG SMITH Properties narrative.

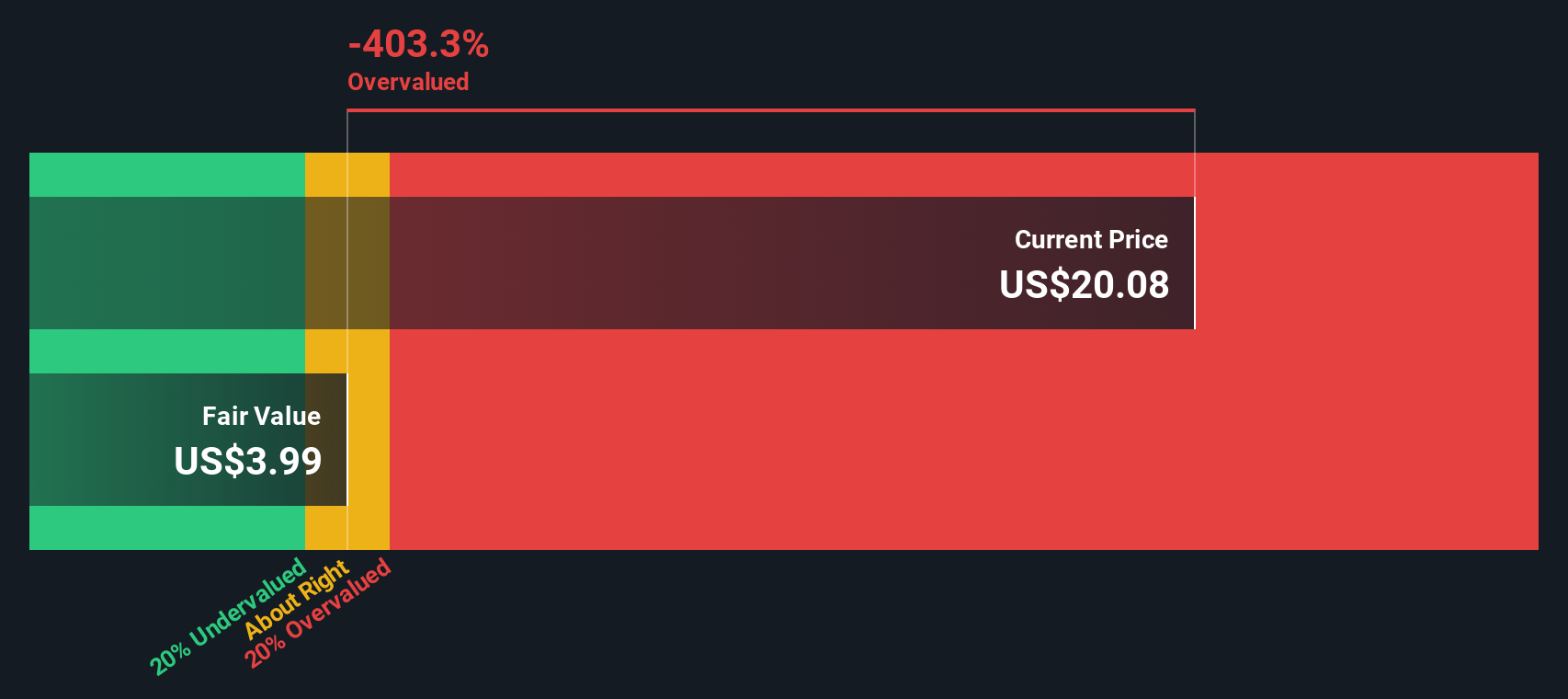

Another View: SWS DCF Model Paints a Cautious Picture

While the price-to-sales ratio suggests JBG SMITH Properties is fairly valued, our DCF model tells a different story. According to SWS DCF analysis, the current share price of $17.96 is well above the estimated fair value of $4.84. This implies the stock could be overvalued. Could this mean investors are too optimistic about the company's future?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out JBG SMITH Properties for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 879 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own JBG SMITH Properties Narrative

If you see things differently or want to test your own perspective, you can build a complete analysis yourself in just a few minutes, including your own insights and conclusions. Do it your way

A great starting point for your JBG SMITH Properties research is our analysis highlighting 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Unlock even more opportunities by using the Simply Wall Street Screener. Give yourself a winning edge by checking out new themes shaping markets before others even catch on.

- Boost your portfolio’s cash flow by targeting steady income with these 16 dividend stocks with yields > 3% offering yields above 3%.

- Invest ahead of the curve in the AI-powered revolution by selecting among these 25 AI penny stocks poised for rapid growth and disruption.

- Secure hidden gems trading below fair value through these 879 undervalued stocks based on cash flows and capitalize on overlooked potential before it gains wider recognition.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:JBGS

JBG SMITH Properties

JBG SMITH owns, operates, and develops mixed-use properties concentrated in amenity-rich, Metro-served submarkets in and around Washington, DC, most notably National Landing, that we believe have long-term growth potential and appeal to residential, office, and retail tenants.

Mediocre balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor