Advertisement

- United States

- /

- Specialized REITs

- /

- NYSE:FCPT

Assessing Four Corners Property Trust (FCPT): Is the Stock Undervalued or Already Fully Priced?

Simply Wall St

Reviewed by Simply Wall St

Four Corners Property Trust (FCPT) quietly continues executing its strategy of acquiring and leasing restaurant and retail properties. While recent headlines have been sparse, many investors are watching FCPT's valuation and operational growth closely these days.

See our latest analysis for Four Corners Property Trust.

With Four Corners Property Trust’s share price sitting at $24.01, momentum has been more sideways than surging lately. The bigger story lies in the longer-term results. After a rough patch that dragged its year-to-date share price return down 10.4%, the stock’s five-year total shareholder return of 9.3% shows FCPT has still managed to deliver positive results over the long run, even as recent sentiment has wavered.

If you’re searching for your next investment idea, this is a great time to expand your radar and discover fast growing stocks with high insider ownership

Given these results and the stock’s current trading price, should investors consider Four Corners Property Trust undervalued with potential for future upside, or is the company’s outlook already fully reflected in today’s valuation?

Most Popular Narrative: 16.5% Undervalued

Four Corners Property Trust last closed at $24.01, while the most closely followed narrative pegs its fair value far higher. This places the current market price well below the narrative’s assessment and signals an intriguing disconnect for investors tracking the story.

The company's focus on acquiring and expanding high-quality, e-commerce resistant retail and essential service properties (such as quick service restaurants, automotive services, and medical retail) positions FCPT's tenant base to benefit from long-term growth in physical service retail, supporting future rental income and revenue stability.

Want to know why this growth-focused portfolio has analysts considering future outperformance? There is one crucial assumption about FCPT’s expansion that fuels the narrative’s bold fair value. Explore the logic behind the numbers and see what is driving the valuation that eclipses today’s share price.

Result: Fair Value of $28.75 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, significant concentration in casual dining and intensifying competition for quality assets could challenge Four Corners Property Trust’s growth trajectory if industry headwinds persist.

Find out about the key risks to this Four Corners Property Trust narrative.

Another View: Is FCPT Actually Expensive?

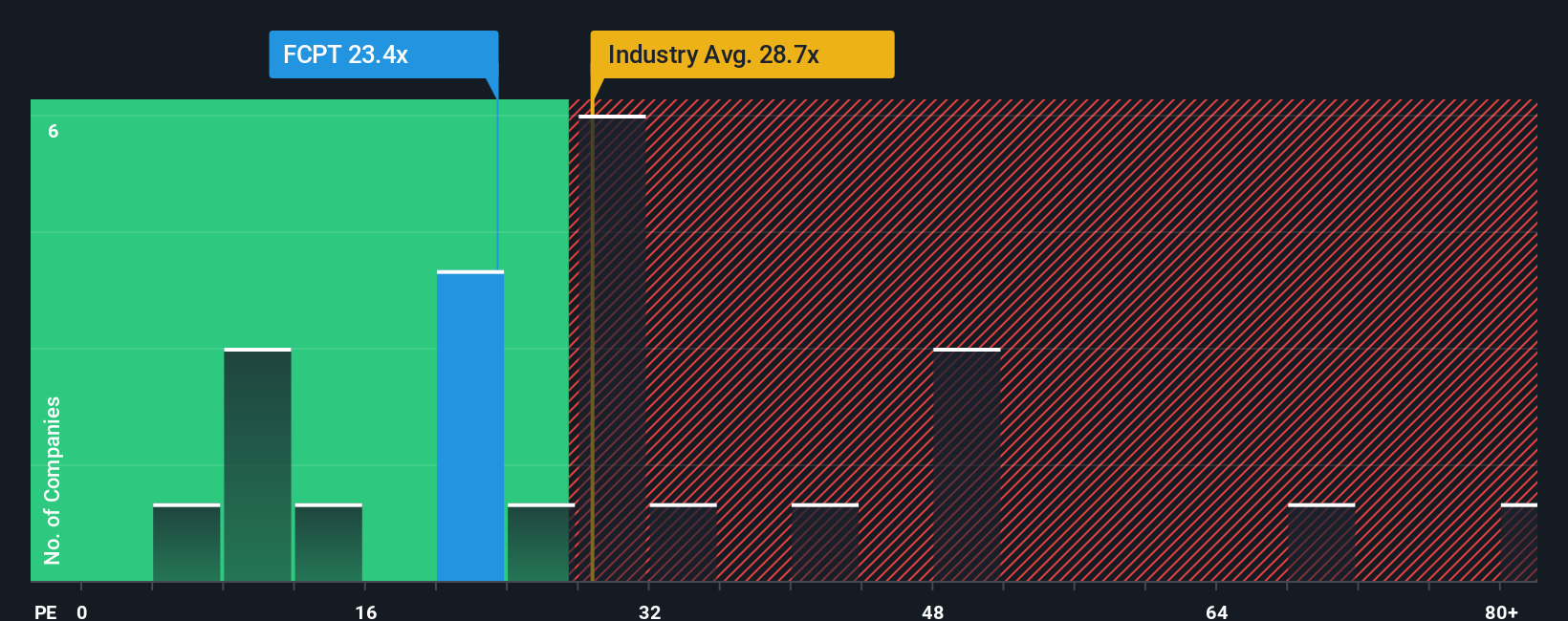

Looking at valuation through the lens of the price-to-earnings ratio provides a more cautious picture for Four Corners Property Trust. The stock trades at 23.3 times earnings, which is higher than the peer average of 20.2 but just below the broader industry’s 28.6. The fair ratio estimate sits at a lofty 34, indicating the market could eventually move much higher. However, the current gap warns that there are valuation risks if multiples shrink further. Is the upside truly as large as it appears, or is caution warranted as markets digest sector headwinds?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Four Corners Property Trust Narrative

If you see things differently or want a more hands-on approach, you can dive into the numbers and craft your own perspective in just a few minutes with Do it your way.

A great starting point for your Four Corners Property Trust research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

If you want to capitalize on unique market themes and position yourself ahead of the curve, don’t let these standout opportunities pass you by on Simply Wall Street.

- Uncover growth potential by checking out these 923 undervalued stocks based on cash flows which stand out based on strong cash flow fundamentals and attractive pricing in today’s market.

- Strengthen your income stream by tapping into these 15 dividend stocks with yields > 3% featuring yields above 3% and consistent dividend histories for steady long-term returns.

- Stay ahead of emerging technology trends with these 25 AI penny stocks ready to transform entire industries through innovations in artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FCPT

Four Corners Property Trust

FCPT is a real estate investment trust primarily engaged in the ownership, acquisition and leasing of restaurant and retail properties.

6 star dividend payer with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

96 followersusers have followed this narrative

10 commentsusers have commented on this narrative

19 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative