Advertisement

- United States

- /

- Specialized REITs

- /

- NYSE:EPR

We Think EPR Properties' (NYSE:EPR) CEO Compensation Package Needs To Be Put Under A Microscope

EPR Properties (NYSE:EPR) has not performed well recently and CEO Greg Silvers will probably need to up their game. Shareholders will be interested in what the board will have to say about turning performance around at the next AGM on 28 May 2021. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. The data we present below explains why we think CEO compensation is not consistent with recent performance.

See our latest analysis for EPR Properties

Comparing EPR Properties' CEO Compensation With the industry

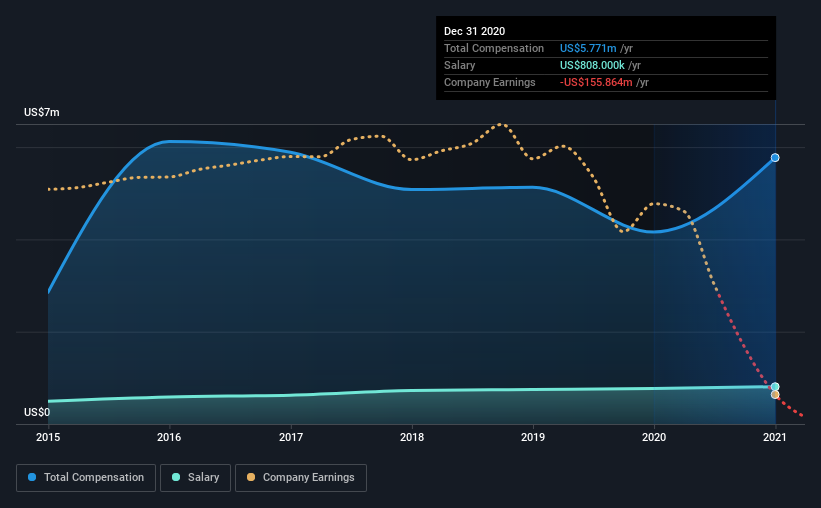

According to our data, EPR Properties has a market capitalization of US$3.5b, and paid its CEO total annual compensation worth US$5.8m over the year to December 2020. We note that's an increase of 39% above last year. While we always look at total compensation first, our analysis shows that the salary component is less, at US$808k.

On comparing similar companies from the same industry with market caps ranging from US$2.0b to US$6.4b, we found that the median CEO total compensation was US$5.4m. From this we gather that Greg Silvers is paid around the median for CEOs in the industry. Moreover, Greg Silvers also holds US$26m worth of EPR Properties stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | US$808k | US$770k | 14% |

| Other | US$5.0m | US$3.4m | 86% |

| Total Compensation | US$5.8m | US$4.2m | 100% |

Speaking on an industry level, nearly 15% of total compensation represents salary, while the remainder of 85% is other remuneration. Although there is a difference in how total compensation is set, EPR Properties more or less reflects the market in terms of setting the salary. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

EPR Properties' Growth

Over the last three years, EPR Properties has shrunk its funds from operations (FFO) by 83% per year. It saw its revenue drop 43% over the last year.

The decline in FFO is a bit concerning. This is compounded by the fact revenue is actually down on last year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has EPR Properties Been A Good Investment?

With a three year total loss of 10% for the shareholders, EPR Properties would certainly have some dissatisfied shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, management will get a chance to explain how they plan to get the business back on track and address the concerns from investors.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. In our study, we found 2 warning signs for EPR Properties you should be aware of, and 1 of them is concerning.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you decide to trade EPR Properties, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if EPR Properties might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSE:EPR

EPR Properties

EPR Properties (NYSE: EPR) is the leading diversified experiential net lease real estate investment trust (REIT), specializing in select enduring experiential properties in the real estate industry.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|23.7% undervalued

MA

Community Contributor

A formidable player in AI and enterprise computing.

Fair Value US$210.00|0.7% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|14.9% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor