Advertisement

- United States

- /

- Industrial REITs

- /

- NYSE:EGP

Should Cantor’s Overweight Rating and Dividend Hike Signal a Shift in EastGroup’s (EGP) Strategy?

Simply Wall St

Reviewed by Sasha Jovanovic

- Cantor Fitzgerald recently initiated coverage on EastGroup Properties with an Overweight rating, emphasizing the company's strong balance sheet and unique development strategy as advantages in the recovering industrial sector.

- EastGroup also announced a 10.7% increase in its quarterly dividend, highlighting management's confidence in the company's financial performance and investment direction.

- To understand the implications of this new analyst support, we'll examine how EastGroup's dividend increase could reinforce its investment outlook.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

EastGroup Properties Investment Narrative Recap

To see EastGroup Properties as a compelling holding, investors typically bet on continued demand for high-quality industrial space in major Sunbelt and Western US markets, underpinned by supply constraints and structural economic shifts favoring logistics. While Cantor Fitzgerald’s new Overweight rating may boost positive sentiment and shine a light on EastGroup’s balance sheet in the short term, it does not fundamentally remove the company’s biggest risk: prolonged tenant uncertainty in key regions, especially California, which could weigh on leasing activity and financial performance.

The recent decision by EastGroup to raise its quarterly dividend by 10.7% is especially relevant to this outlook, as it signals confidence in steady cash generation despite a period characterized by cautious capital allocation and selective new development starts. This increase aligns with consensus expectations for industrial REITs to leverage resilient fundamentals during sector recoveries, and could further support EastGroup’s investment appeal to income-focused shareholders.

However, investors should be mindful that, in contrast, concentrated geographic exposure in markets facing regulatory hurdles and climate risk could still pose challenges if...

Read the full narrative on EastGroup Properties (it's free!)

EastGroup Properties' narrative projects $921.3 million revenue and $339.7 million earnings by 2028. This requires 10.8% yearly revenue growth and a $103.2 million earnings increase from $236.5 million today.

Uncover how EastGroup Properties' forecasts yield a $188.28 fair value, a 11% upside to its current price.

Exploring Other Perspectives

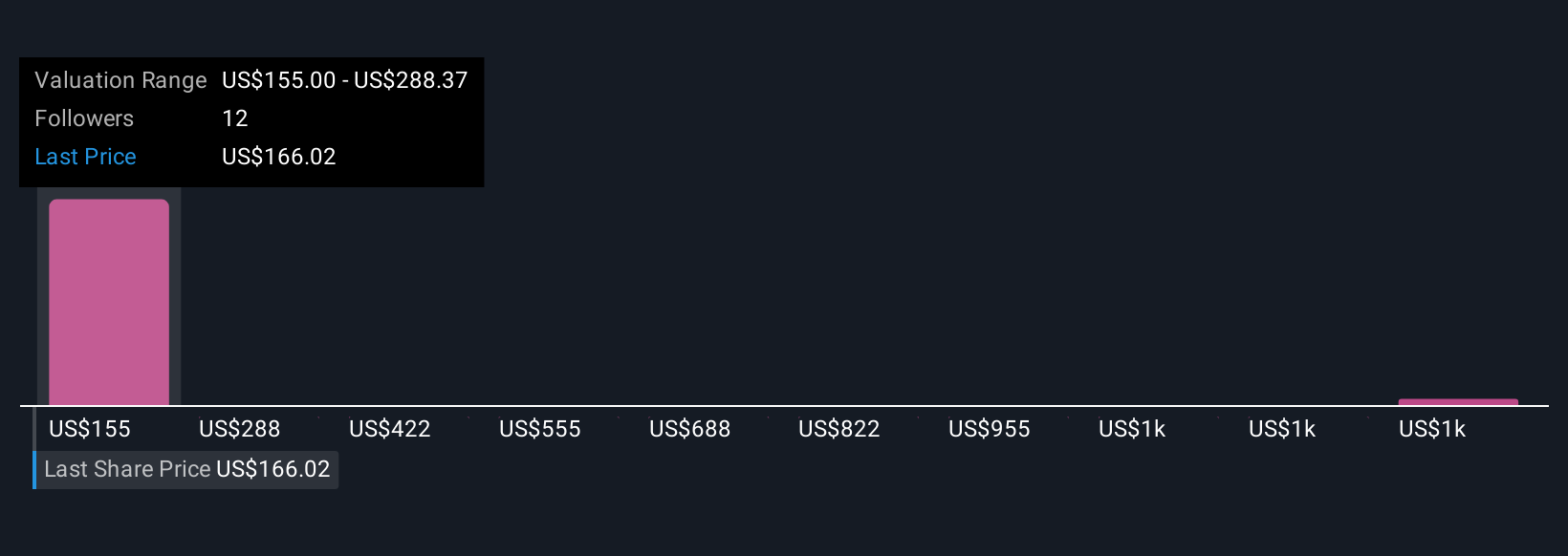

Five private investors in the Simply Wall St Community placed EastGroup’s fair value between US$155 and an outlier estimate of US$1,488, highlighting distinctive expectations for future growth. While the company’s ability to capitalize on migration to Sunbelt markets is supportive, these diverse viewpoints remind you to consider multiple angles before drawing your own conclusions.

Explore 5 other fair value estimates on EastGroup Properties - why the stock might be worth 9% less than the current price!

Build Your Own EastGroup Properties Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your EastGroup Properties research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free EastGroup Properties research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate EastGroup Properties' overall financial health at a glance.

Ready For A Different Approach?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Rare earth metals are the new gold rush. Find out which 33 stocks are leading the charge.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if EastGroup Properties might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EGP

EastGroup Properties

EastGroup Properties, Inc. (NYSE: EGP), a member of the S&P Mid-Cap 400 and Russell 2000 Indexes, is a self-administered equity real estate investment trust focused on the development, acquisition and operation of industrial properties in high-growth markets throughout the United States with an emphasis in the states of Texas, Florida, California, Arizona and North Carolina.

Established dividend payer with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.2% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|90.0% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.6% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.1% undervalued

AG

Community Contributor