Advertisement

- United States

- /

- Pharma

- /

- NYSE:TEVA

Teva (NYSE:TEVA) Valuation Check After Strong Q3, Margin Targets and Deleveraging Drive a Sharp Share Price Rebound

Simply Wall St

Reviewed by Simply Wall St

Teva Pharmaceutical Industries (NYSE:TEVA) is getting fresh attention after upbeat Q3 results, with revenue up 3% and debt ratios improving as management leans harder into higher margin innovative drugs like AUSTEDO and AJOVY.

See our latest analysis for Teva Pharmaceutical Industries.

The market has clearly noticed, with a roughly 36% 1 month share price return and 46.9% 3 month share price return propelling Teva to $27.83, while its 3 year total shareholder return above 230% signals that momentum is firmly building rather than fading.

If Teva’s turnaround story has your attention, it could be a good moment to scan other pharma names with improving fundamentals and income potential through pharma stocks with solid dividends.

With the shares now hugging Wall Street’s consensus price target and the turnaround clearly in motion, are investors still getting Teva at a discount, or is the market already baking in the next leg of growth?

Most Popular Narrative: 20% Undervalued

Against Teva Pharmaceutical Industries last close at $27.83, the most widely followed narrative points to a higher fair value anchored in improving earnings power.

The accelerating launch cadence of biosimilars (with 8 launches targeted through 2027 and a goal to double biosimilar revenue), backed by favorable regulatory trends increasing biosimilar adoption in major markets, should unlock incremental, higher margin revenue streams and offset headwinds from traditional generics, powering long term EBITDA growth.

Curious what kind of revenue runway, margin expansion, and future earnings multiple are baked into that upside view? The narrative leans on bold profitability and valuation assumptions that could reframe how this slow growing top line justifies a much richer share price.

Result: Fair Value of $27.90 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upside view could unravel if IRA pricing on AUSTEDO bites harder than expected or if execution on key biosimilar launches stumbles.

Find out about the key risks to this Teva Pharmaceutical Industries narrative.

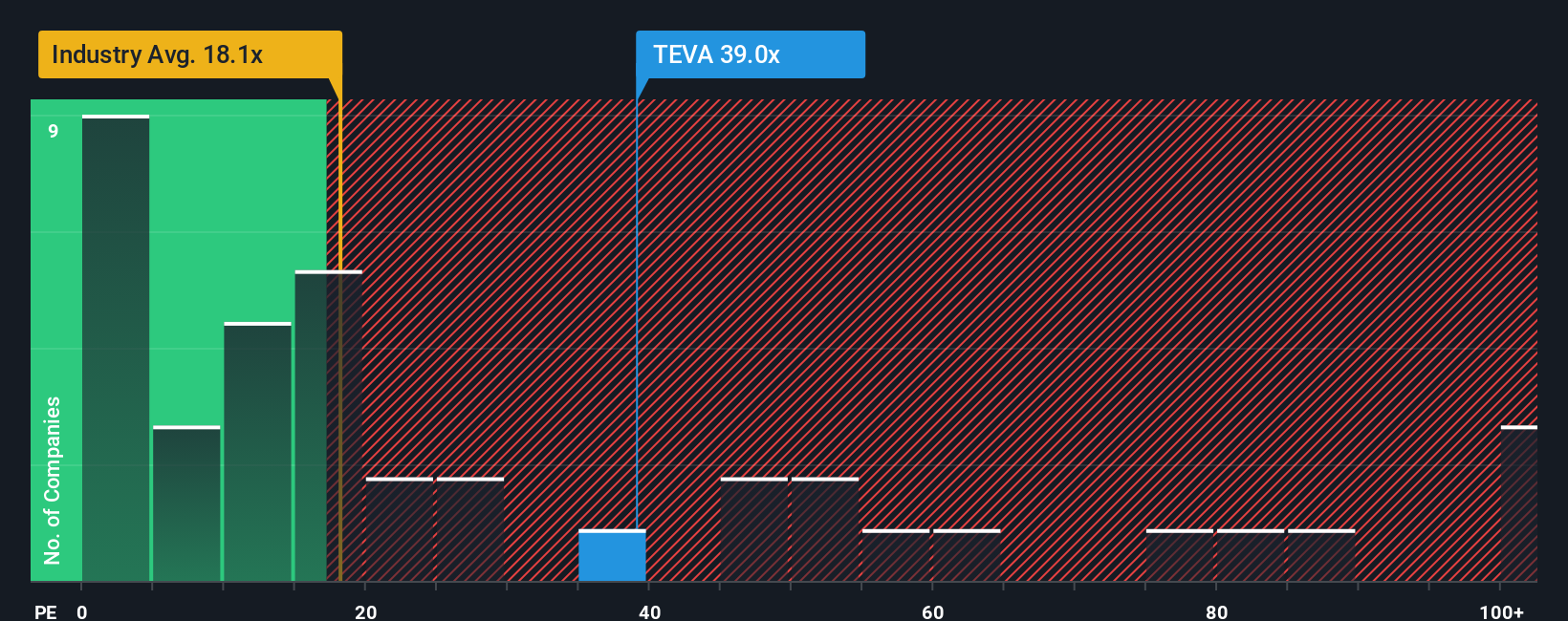

Another View: Multiples Flash a Caution Light

While narratives and fair value estimates point to upside, the current price tag looks stretched on earnings. Teva trades on a 44.8x price to earnings ratio, well above the US pharma average of 20x, peers at 35.9x, and even our fair ratio of 28.3x.

This gap suggests investors are already paying up for execution and IRA clarity, leaving less margin for error if growth or margins disappoint, or for upside if things go right. Is the market getting ahead of itself, or just pricing a durable turnaround early?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Teva Pharmaceutical Industries Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a personalized narrative in minutes: Do it your way.

A great starting point for your Teva Pharmaceutical Industries research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for your next smart investment move?

Before you close this tab, line up your watchlist with fresh opportunities using targeted screeners that surface quality, momentum, and income potential other investors may be overlooking.

- Boost potential total returns by focusing on reliable income through these 14 dividend stocks with yields > 3% that combine attractive yields with solid underlying businesses.

- Capitalize on structural growth by targeting innovation leaders across these 25 AI penny stocks positioned to benefit from ongoing advances in automation and machine learning.

- Sharpen your value edge by zeroing in on these 918 undervalued stocks based on cash flows that trade below what their cash flows and fundamentals might justify.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Teva Pharmaceutical Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TEVA

Teva Pharmaceutical Industries

Develops, manufactures, markets, and distributes generic and other medicines, and biopharmaceutical products in the United States, Europe, Israel, and internationally.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

40 followersusers have followed this narrative

6 commentsusers have commented on this narrative

11 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.1% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5190.0% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

115 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

953 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative