- United States

- /

- Pharma

- /

- NYSE:PRGO

If You Had Bought Perrigo (NYSE:PRGO) Stock Five Years Ago, You'd Be Sitting On A 67% Loss, Today

Statistically speaking, long term investing is a profitable endeavour. But that doesn't mean long term investors can avoid big losses. For example the Perrigo Company plc (NYSE:PRGO) share price dropped 67% over five years. That's not a lot of fun for true believers. On the other hand the share price has bounced 8.7% over the last week.

Check out our latest analysis for Perrigo

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

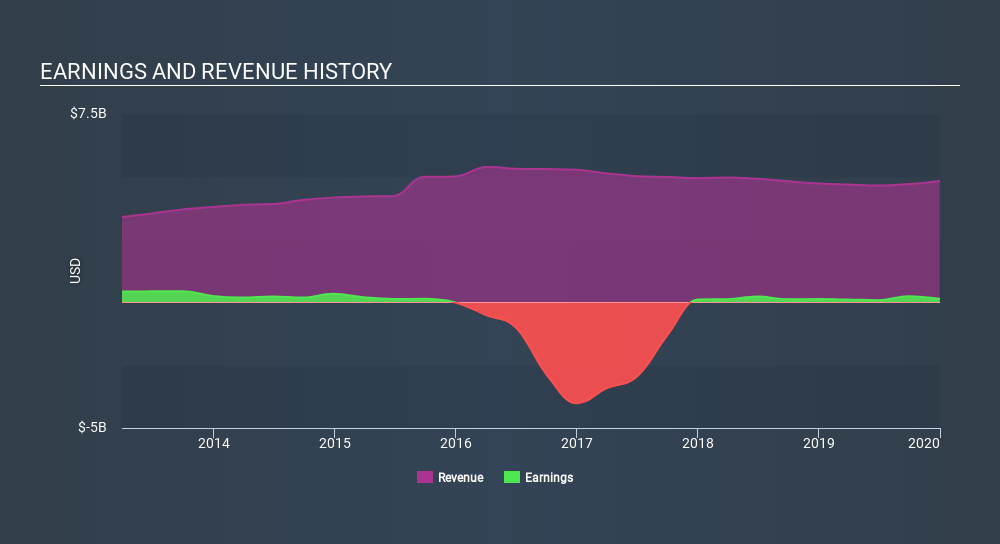

Perrigo became profitable within the last five years. Most would consider that to be a good thing, so it's counter-intuitive to see the share price declining. Other metrics may better explain the share price move.

The modest 1.6% dividend yield is unlikely to be guiding the market view of the stock. Revenue is actually up 0.5% over the time period. So it seems one might have to take closer look at the fundamentals to understand why the share price languishes. After all, there may be an opportunity.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

We like that insiders have been buying shares in the last twelve months. Having said that, most people consider earnings and revenue growth trends to be a more meaningful guide to the business. This free report showing analyst forecasts should help you form a view on Perrigo

What about the Total Shareholder Return (TSR)?

We've already covered Perrigo's share price action, but we should also mention its total shareholder return (TSR). Arguably the TSR is a more complete return calculation because it accounts for the value of dividends (as if they were reinvested), along with the hypothetical value of any discounted capital that have been offered to shareholders. Dividends have been really beneficial for Perrigo shareholders, and that cash payout explains why its total shareholder loss of 65%, over the last 5 years, isn't as bad as the share price return.

A Different Perspective

It's good to see that Perrigo has rewarded shareholders with a total shareholder return of 21% in the last twelve months. That's including the dividend. There's no doubt those recent returns are much better than the TSR loss of 19% per year over five years. We generally put more weight on the long term performance over the short term, but the recent improvement could hint at a (positive) inflection point within the business. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Like risks, for instance. Every company has them, and we've spotted 2 warning signs for Perrigo (of which 1 doesn't sit too well with us!) you should know about.

Perrigo is not the only stock that insiders are buying. For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:PRGO

Perrigo

Provides over-the-counter health and wellness solutions to enhance individual well-being in the United States, Europe, and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Community Narratives