Advertisement

- United States

- /

- Pharma

- /

- NYSE:BMY

Bristol-Myers Squibb's (NYSE:BMY) Profits are Understated and the Company has Room for New Growth

The market for Bristol-Myers Squibb Company's ( NYSE:BMY ) shares didn't move much after it posted weak earnings recently, but seems to be currently entering a bear run. When faced with uncertainty, it is always good to return to the fundamentals and see the performance and future growth capabilities of the company.

We did some digging, and we believe the earnings are stronger than they seem, and that there is room for growth from new marketed products.

In this article, we will analyze both the growth prospects and the fundamental performance of the company.

Growth Drivers

Bristol-Myers Squibb has recently bolstered their product portfolio with new additions, and we are just starting to see the revenues from these products in an early phase.

These new products are the driver that is going to keep the revenue growth rate at a sustainable level. Analysts that follow the company estimate an annual revenue growth rate of 3%.

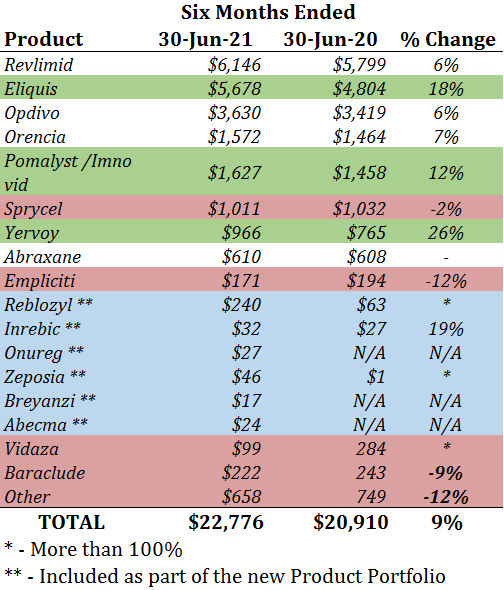

From the chart above, we can see that the company has 4 declining items, 3 items that gained 10%+ in the last six months, and perhaps most importantly - it has 6 new items with an uncertain future. In the latter group is where the possibility of value lies, because investors that make the most accurate estimate on the growth of the new products are those that are most likely to benefit.

Overall, it seems that the company is going to continue with low but steady growth, which is something investors might be looking forward to, especially considering the recent volatility.

Fundamental Performance

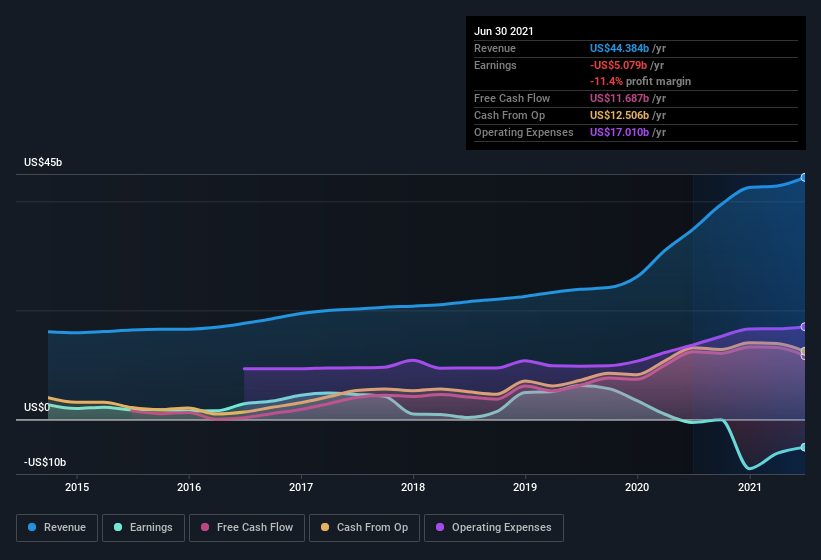

There are a few main aspects to the fundamental performance of the company. First is the successful revenue growth since 2020, which gives the company a lot more breathing room, especially because the revenues scale efficiently in relation to costs.

In the trailing twelve-month period - ending June 30th, we observe a 27% revenue growth and just a 17% growth in COGS (cost of goods sold) - This scaling will increase margins and lead to more cash inflows for Bristol-Myers Squibb.

Another aspect is the negative net income, which diverges from the free cash flows of the company. We will analyze both of these further below.

View our latest analysis for Bristol-Myers Squibb

Examining Cashflow Against Bristol-Myers Squibb's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio . In plain English, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period.

The ratio shows us how much a company's profit exceeds its FCF.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive.

For the year to June 2021, Bristol-Myers Squibb had an accrual ratio of -0.24.

That implies it has very good cash conversion, and that its earnings in the last year actually significantly understate its free cash flow.

The company produced free cash flow of US$12b during the period, dwarfing its reported profit of -US$5.08b.

However, that's not all there is to consider. We can see that unusual items have impacted its statutory profit, and therefore the accrual ratio.

How Do Unusual Items Influence Profit?

Bristol-Myers Squibb's profit was reduced by unusual items worth US$13b in the last twelve months, and this helped it produce high cash conversion, as reflected by its unusual items. This is what you'd expect to see where a company has a non-cash charge reducing paper profits.

In the twelve months to June 2021, Bristol-Myers Squibb had a big unusual items expense. All else being equal, this would likely have the effect of making the statutory profit look worse than its underlying earnings power.

Conclusion

The company is pushing a renewed product portfolio which has the potential to drive additional future growth. The new medicines are in a relatively new stage in the sales cycle, but that also means that they have a long patent life in-front of them.

The fundamental performance is stabilizing and revenues are scaling much better than costs. This opens the way to higher EBIT margins in the future.

Considering both Bristol-Myers Squibb's accrual ratio and its unusual items, we think its statutory earnings are unlikely to exaggerate the company's underlying earnings power. Based on these factors, we think Bristol-Myers Squibb's underlying earnings potential is as good as, or probably even better, than the statutory profit makes it seem!

So while earnings quality is important, it's equally important to consider the risks facing Bristol-Myers Squibb at this point in time. While conducting our analysis, we found that Bristol-Myers Squibb has 3 warning signs and it would be unwise to ignore them.

Valuation is complex, but we're here to simplify it.

Discover if Bristol-Myers Squibb might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NYSE:BMY

Bristol-Myers Squibb

Bristol-Myers Squibb Company discovers, develops, licenses, manufactures, markets, distributes, and sells biopharmaceutical products worldwide.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|82.7% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|36.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|61.4% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|37.1% undervalued

UN

Community Contributor