- United States

- /

- Biotech

- /

- NasdaqGS:VIGL

Here's Why We're Not Too Worried About Vigil Neuroscience's (NASDAQ:VIGL) Cash Burn Situation

There's no doubt that money can be made by owning shares of unprofitable businesses. By way of example, Vigil Neuroscience (NASDAQ:VIGL) has seen its share price rise 180% over the last year, delighting many shareholders. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

So notwithstanding the buoyant share price, we think it's well worth asking whether Vigil Neuroscience's cash burn is too risky. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

View our latest analysis for Vigil Neuroscience

Does Vigil Neuroscience Have A Long Cash Runway?

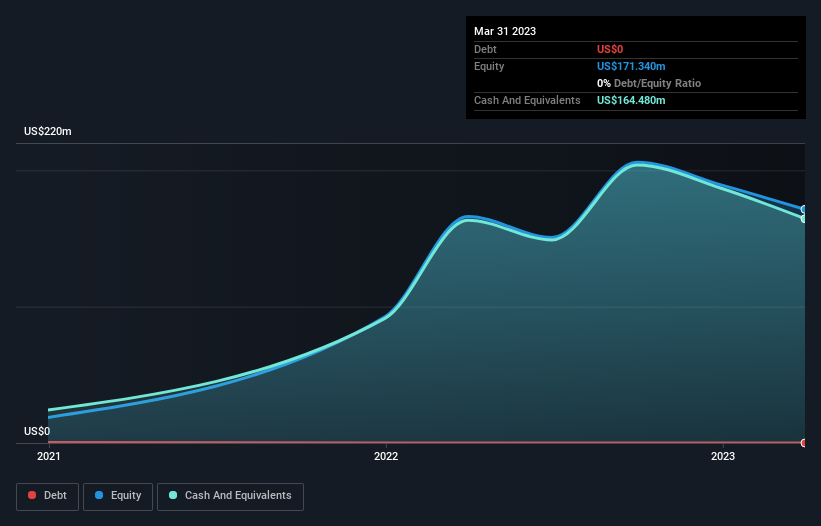

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. In March 2023, Vigil Neuroscience had US$164m in cash, and was debt-free. Looking at the last year, the company burnt through US$70m. That means it had a cash runway of about 2.3 years as of March 2023. That's decent, giving the company a couple years to develop its business. You can see how its cash balance has changed over time in the image below.

How Is Vigil Neuroscience's Cash Burn Changing Over Time?

Vigil Neuroscience didn't record any revenue over the last year, indicating that it's an early stage company still developing its business. Nonetheless, we can still examine its cash burn trajectory as part of our assessment of its cash burn situation. Over the last year its cash burn actually increased by 33%, which suggests that management are increasing investment in future growth, but not too quickly. However, the company's true cash runway will therefore be shorter than suggested above, if spending continues to increase. Clearly, however, the crucial factor is whether the company will grow its business going forward. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Hard Would It Be For Vigil Neuroscience To Raise More Cash For Growth?

While Vigil Neuroscience does have a solid cash runway, its cash burn trajectory may have some shareholders thinking ahead to when the company may need to raise more cash. Companies can raise capital through either debt or equity. Many companies end up issuing new shares to fund future growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Since it has a market capitalisation of US$313m, Vigil Neuroscience's US$70m in cash burn equates to about 23% of its market value. That's fairly notable cash burn, so if the company had to sell shares to cover the cost of another year's operations, shareholders would suffer some costly dilution.

Is Vigil Neuroscience's Cash Burn A Worry?

On this analysis of Vigil Neuroscience's cash burn, we think its cash runway was reassuring, while its increasing cash burn has us a bit worried. While we're the kind of investors who are always a bit concerned about the risks involved with cash burning companies, the metrics we have discussed in this article leave us relatively comfortable about Vigil Neuroscience's situation. Taking a deeper dive, we've spotted 4 warning signs for Vigil Neuroscience you should be aware of, and 1 of them is potentially serious.

Of course Vigil Neuroscience may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:VIGL

Vigil Neuroscience

A clinical-stage biotechnology company, focuses on developing treatments for rare and common neurodegenerative diseases by restoring the vigilance of microglia, the sentinel immune cells of the brain.

Flawless balance sheet low.

Market Insights

Community Narratives