- United States

- /

- Biotech

- /

- NasdaqGM:TRDA

Earnings Miss: Entrada Therapeutics, Inc. Missed EPS And Analysts Are Revising Their Forecasts

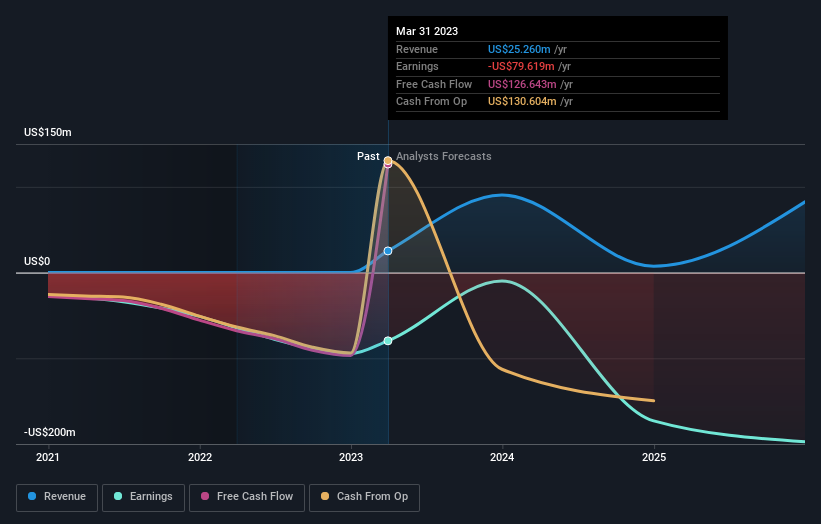

Investors in Entrada Therapeutics, Inc. (NASDAQ:TRDA) had a good week, as its shares rose 3.1% to close at US$12.50 following the release of its quarterly results. It was a pretty bad result overall, with revenues coming in 68% lower than the analysts predicted. Statutory earnings correspondingly nosedived, with Entrada Therapeutics reporting a loss of US$0.21 per share, where the analysts were expecting a profit. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

Check out our latest analysis for Entrada Therapeutics

Following the latest results, Entrada Therapeutics' three analysts are now forecasting revenues of US$90.5m in 2023. This would be a substantial 258% improvement in sales compared to the last 12 months. Losses are predicted to fall substantially, shrinking 87% to US$0.30. Before this latest report, the consensus had been expecting revenues of US$101.7m and US$3.58 per share in losses. We can see there's definitely been a change in sentiment in this update, with the analysts administering a meaningful downgrade to next year's revenue estimates, while at the same time reducing their loss estimates.

The consensus price target was broadly unchanged at US$21.50, implying that the business is performing roughly in line with expectations, despite adjustments to both revenue and earnings estimates. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic Entrada Therapeutics analyst has a price target of US$25.00 per share, while the most pessimistic values it at US$18.00. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

The Bottom Line

The most obvious conclusion is that the analysts made no changes to their forecasts for a loss next year. They also downgraded their revenue estimates, although industry data suggests that Entrada Therapeutics' revenues are expected to grow faster than the wider industry. Yet - earnings are more important to the intrinsic value of the business. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have forecasts for Entrada Therapeutics going out to 2025, and you can see them free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 4 warning signs for Entrada Therapeutics (1 is a bit concerning) you should be aware of.

Valuation is complex, but we're here to simplify it.

Discover if Entrada Therapeutics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:TRDA

Entrada Therapeutics

A clinical-stage biotechnology company, develops endosomal escape vehicle (EEV) therapeutics for the treatment of multiple neuromuscular diseases.

Flawless balance sheet and fair value.

Market Insights

Community Narratives