- United States

- /

- Pharma

- /

- NasdaqGS:TLRY

Tilray Brands (NasdaqGS:TLRY) Reports Third-Quarter Losses

Reviewed by Simply Wall St

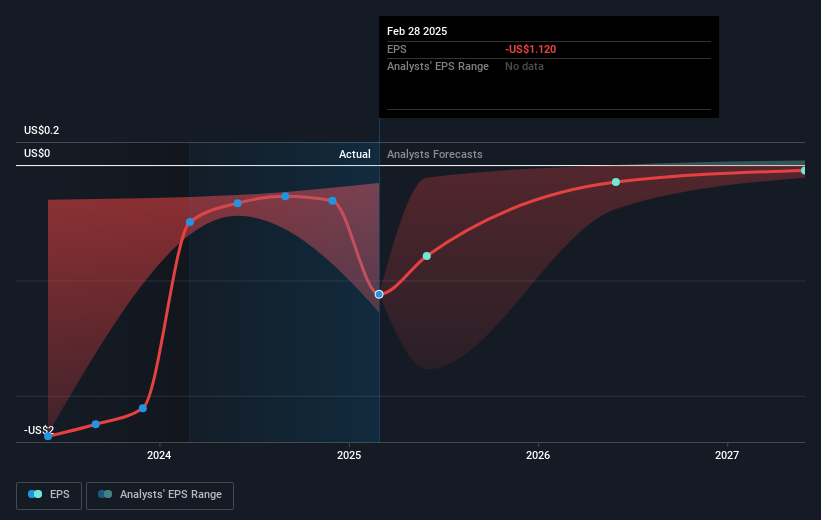

Tilray Brands (NasdaqGS:TLRY) reported significant losses in its third-quarter results, with sales declining slightly and net loss widening considerably compared to the previous year. The company also received a Nasdaq compliance notice regarding its share price, which must stay above $1 to maintain its listing. These events may have contributed to the 18% decline in its stock price over the last week, countering the broader market's 5% rise. Despite revised revenue guidance suggesting potential future improvements, the immediate financial challenges seemed to weigh more heavily on investor sentiment during this period.

We've identified 2 risks for Tilray Brands that you should be aware of.

Over the past year, Tilray Brands' (NasdaqGS:TLRY) total shareholder return has decreased by 73.22%, significantly underperforming the broader US market, which saw a 3.6% rise, and the US Pharmaceuticals industry, which fell by 8.6%. This decline reflects the underlying challenges highlighted in their recent earnings report, including a substantial widening of net losses and a slight dip in sales. The company's revenue forecast of US$850 million to US$950 million for FY 2025 suggests a cautious optimism, yet the widening net losses remain a considerable concern.

The share price adjustment also responds to Tilray receiving a Nasdaq compliance notice due to its current trading price below the US$1 minimum bid requirement, with a deadline of September 21, 2025, for compliance. With the stock trading at 61.5% below the consensus analyst fair value estimate, and a target price significantly higher than the present share price, there remains distinct market skepticism regarding near-term prospects. Despite these challenges, the company's strategic initiatives, like product innovations and expanded distribution, may potentially improve future performance metrics if successfully executed.

Our valuation report here indicates Tilray Brands may be undervalued.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Tilray Brands, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Tilray Brands might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TLRY

Tilray Brands

A lifestyle consumer products company, engages in the research, cultivation, processing, and distribution of medical cannabis products in Canada, the United States, Europe, Australia, New Zealand, Latin America, and internationally.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives